San Francisco Market Update

|

"Do you think prices will go down further? Into 2023?"

Clients, friends, and colleagues,

I get asked this question almost daily, and I'm sure you do too.

While we all have opinions and no one has a crystal ball, I'd like to offer some quick, valuable context to help you reach your own answer.

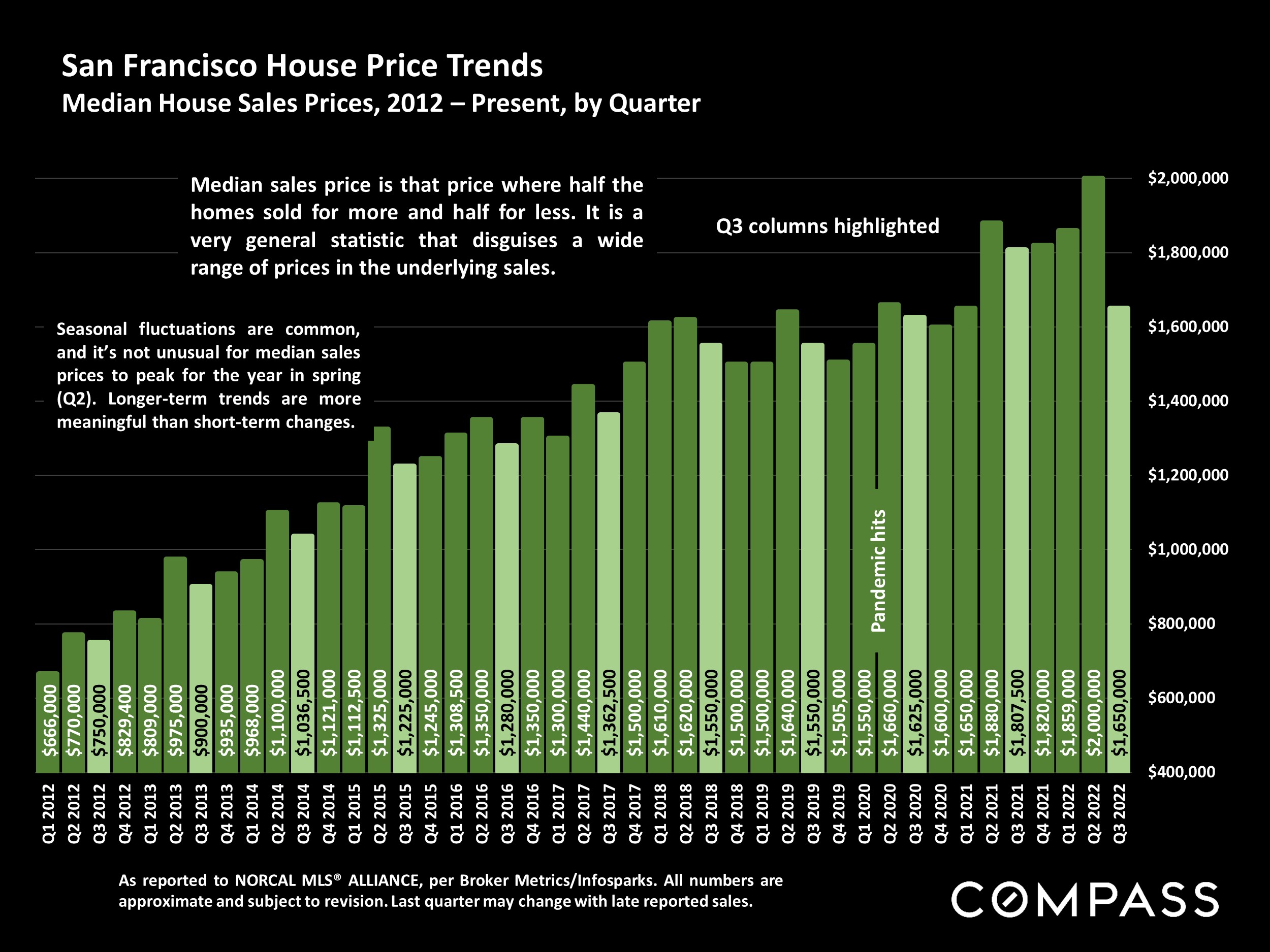

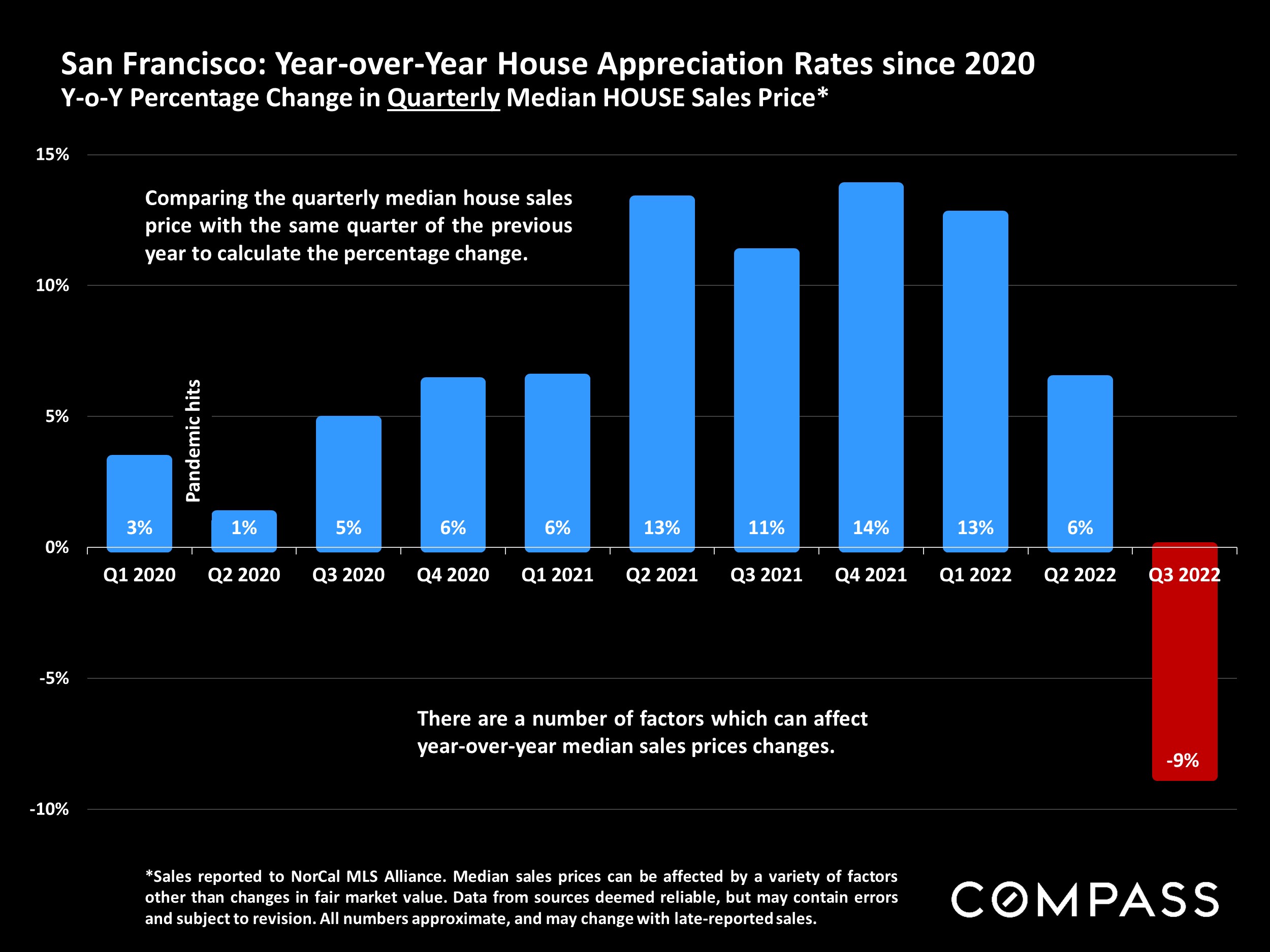

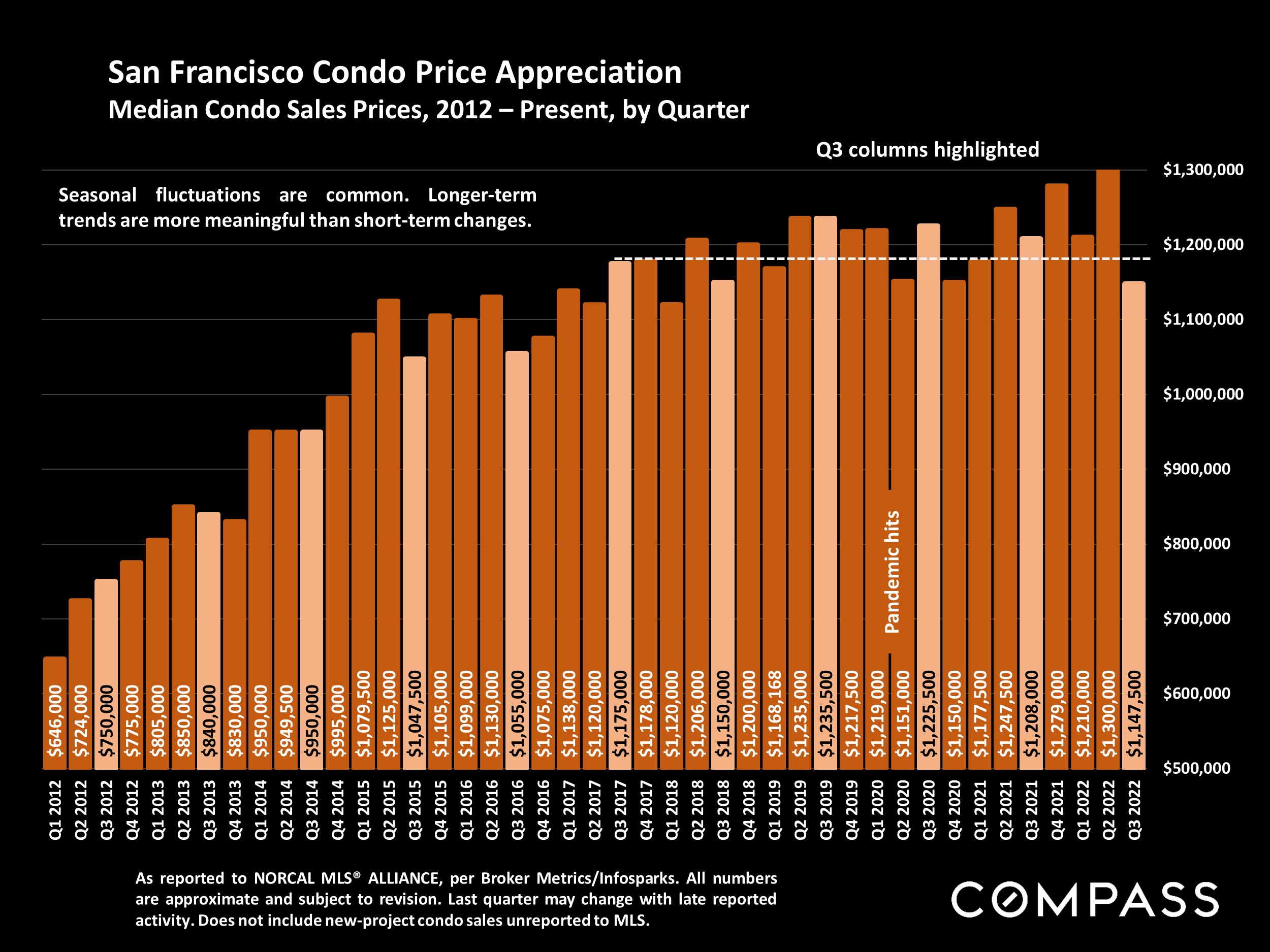

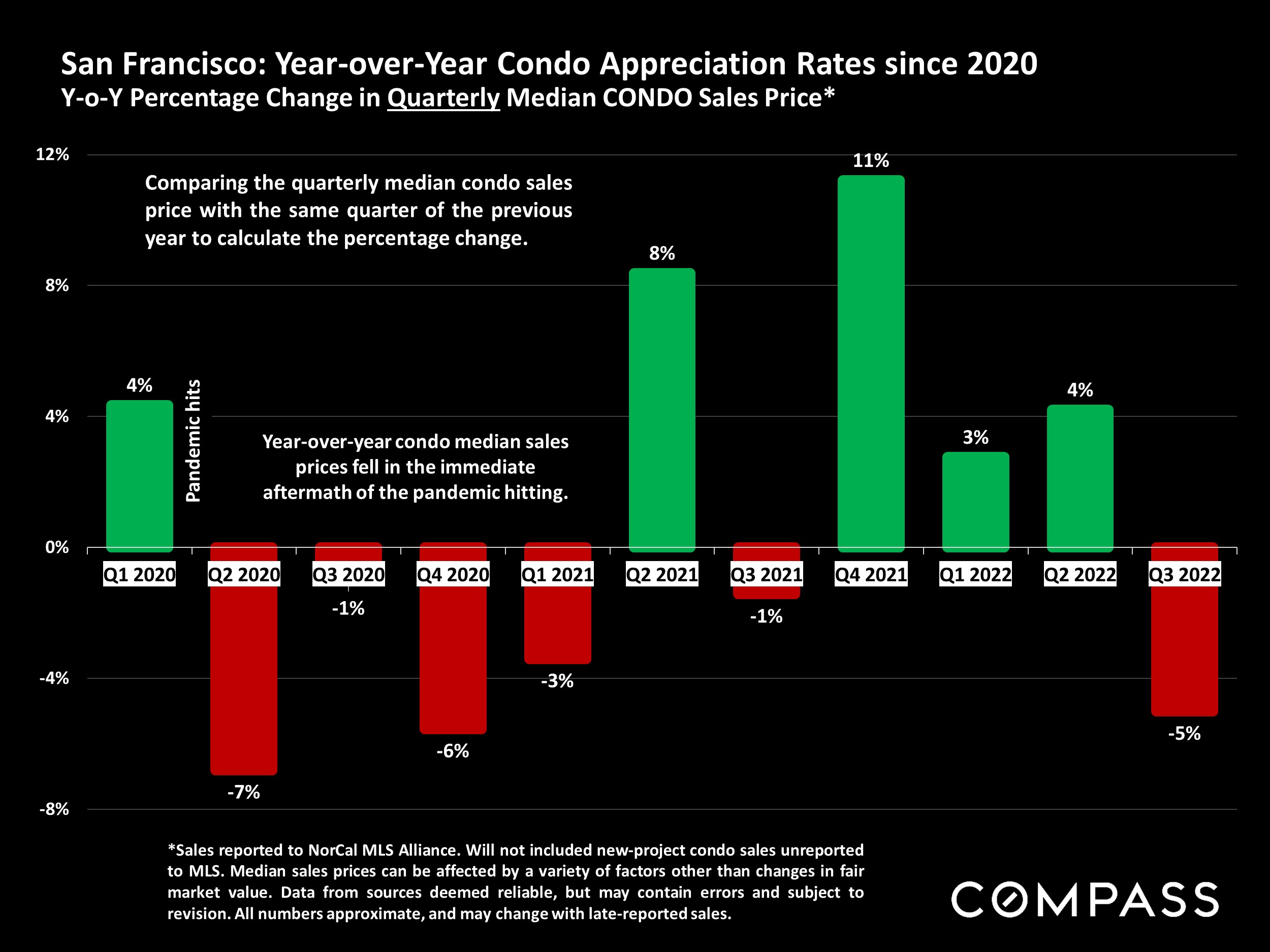

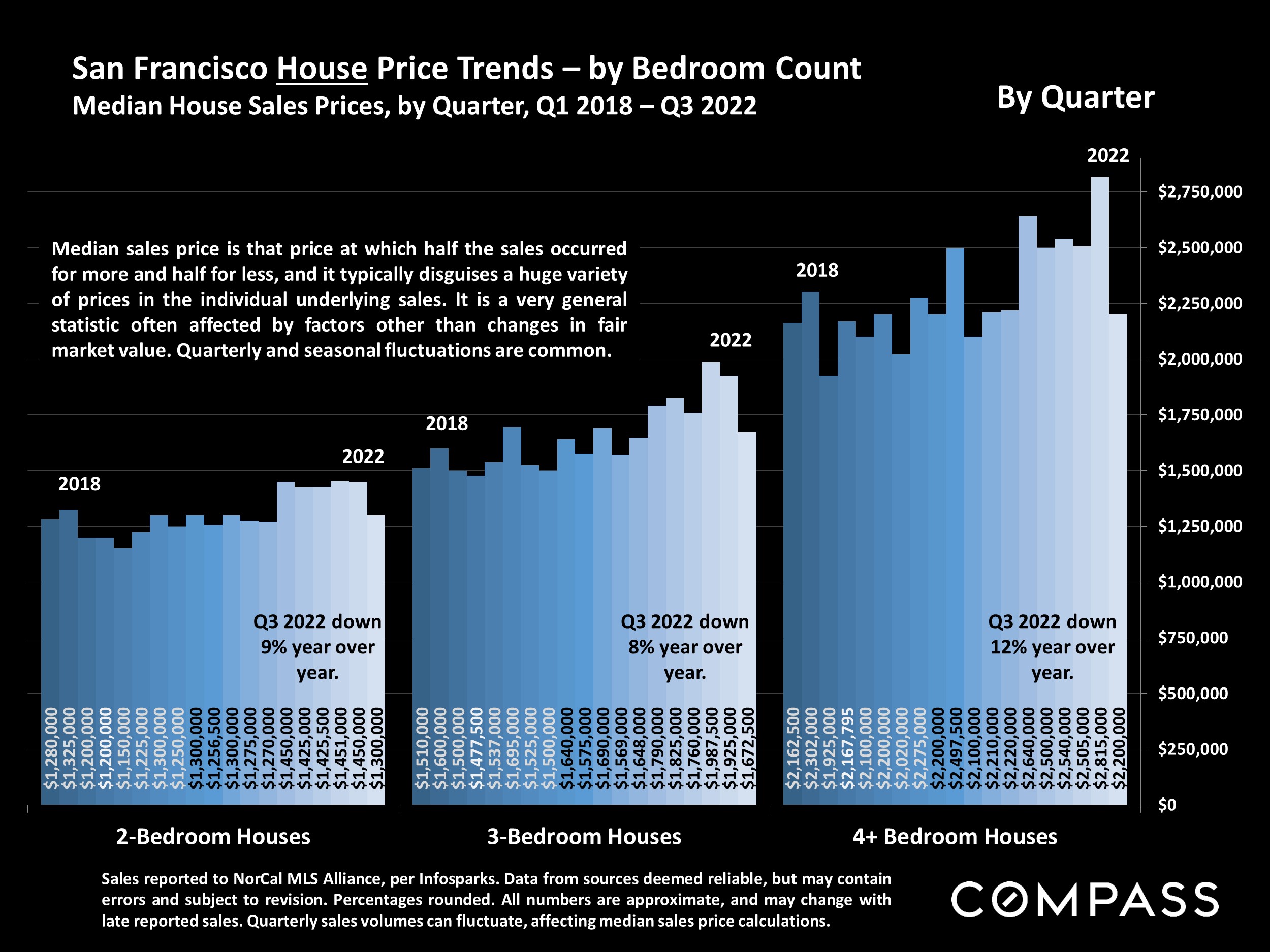

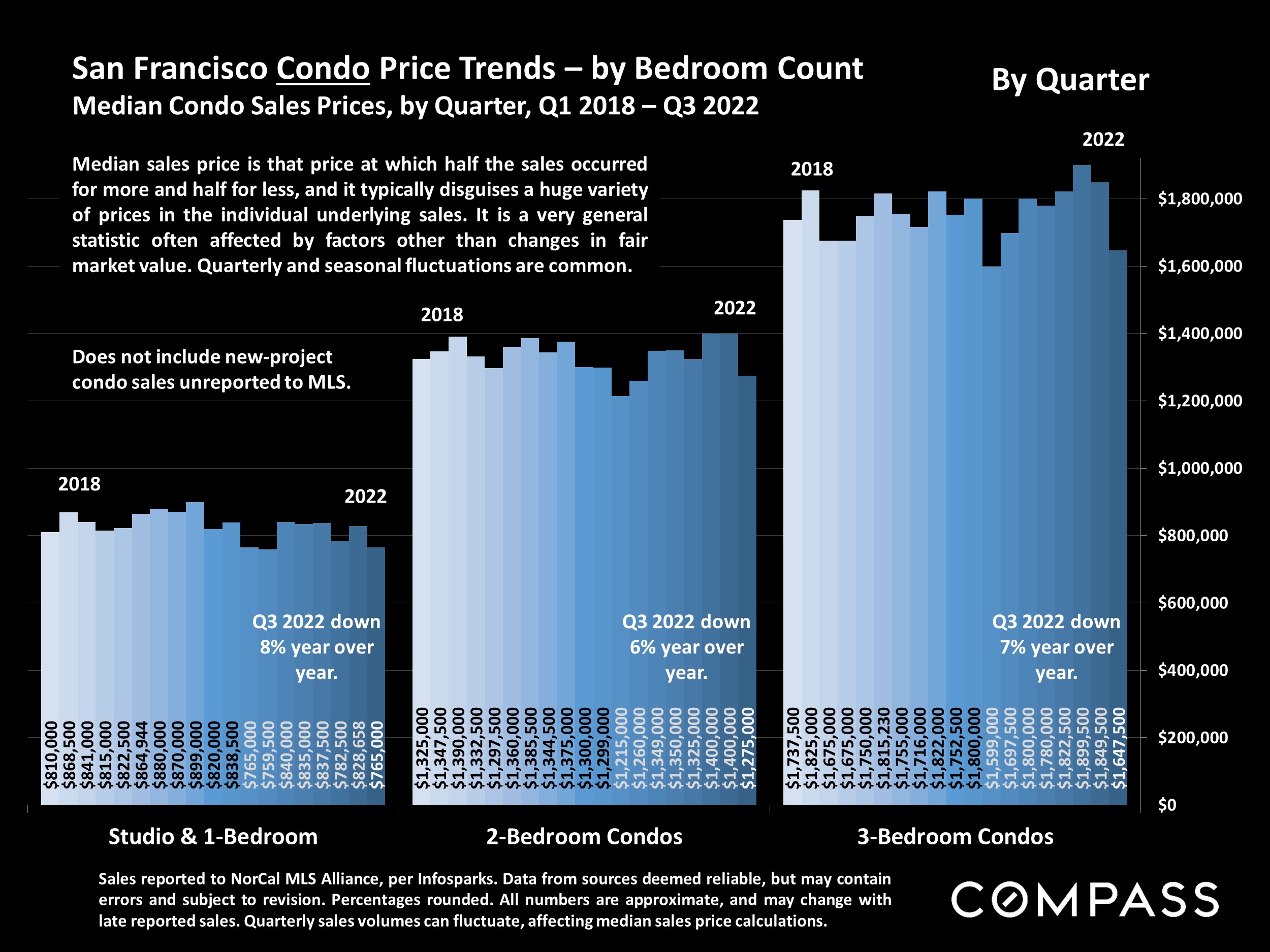

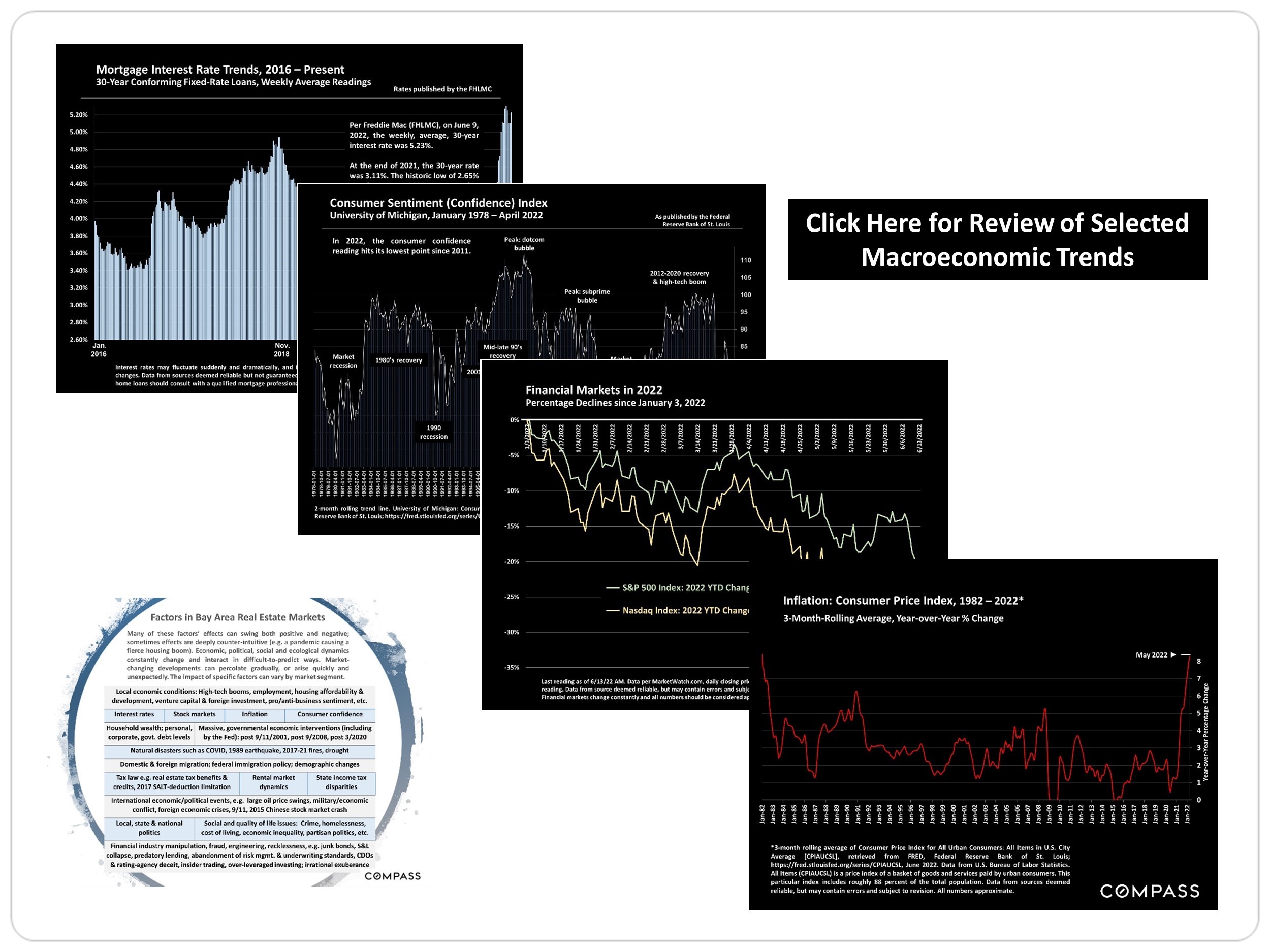

Quick recap of the main reasons for the current market softening: part of the decline is due to seasonal trends - median sales prices often peak for the calendar year in Q2, then drop in summer - but the bigger part is clearly due to changing market conditions prompted by shifts in interest rates (other factors include inflation, stock market volatility, and consumer confidence).

Since interest rates are the main factor here, let's dig in:

1) Quick math on the difference in monthly mortgage payments between a 3% and 6% interest rate (assuming 20% down and 30-yr fixed):

$2M purchase price @ 3% = $6,746/mo

$2M purchase price @ 6% = $9,593/mo

= 42% increase in a buyer's monthly payment.

2) Yes, a current 6% interest rate is not high by any historical standard. But what is historically significant is how quickly they increased. Interest rates have increased nearly 100% in less than a year (from 3.11% to start the year, to over 6% today). This is a shock to buyers' affordability, creating an immediate gap between buyer and seller expectations.

So, is now a good time to buy?

This is always, always a subjective question. If you can comfortably afford to purchase right now, meaning you can forecast a 5+ year horizon, it's a great time to buy. Here's why:

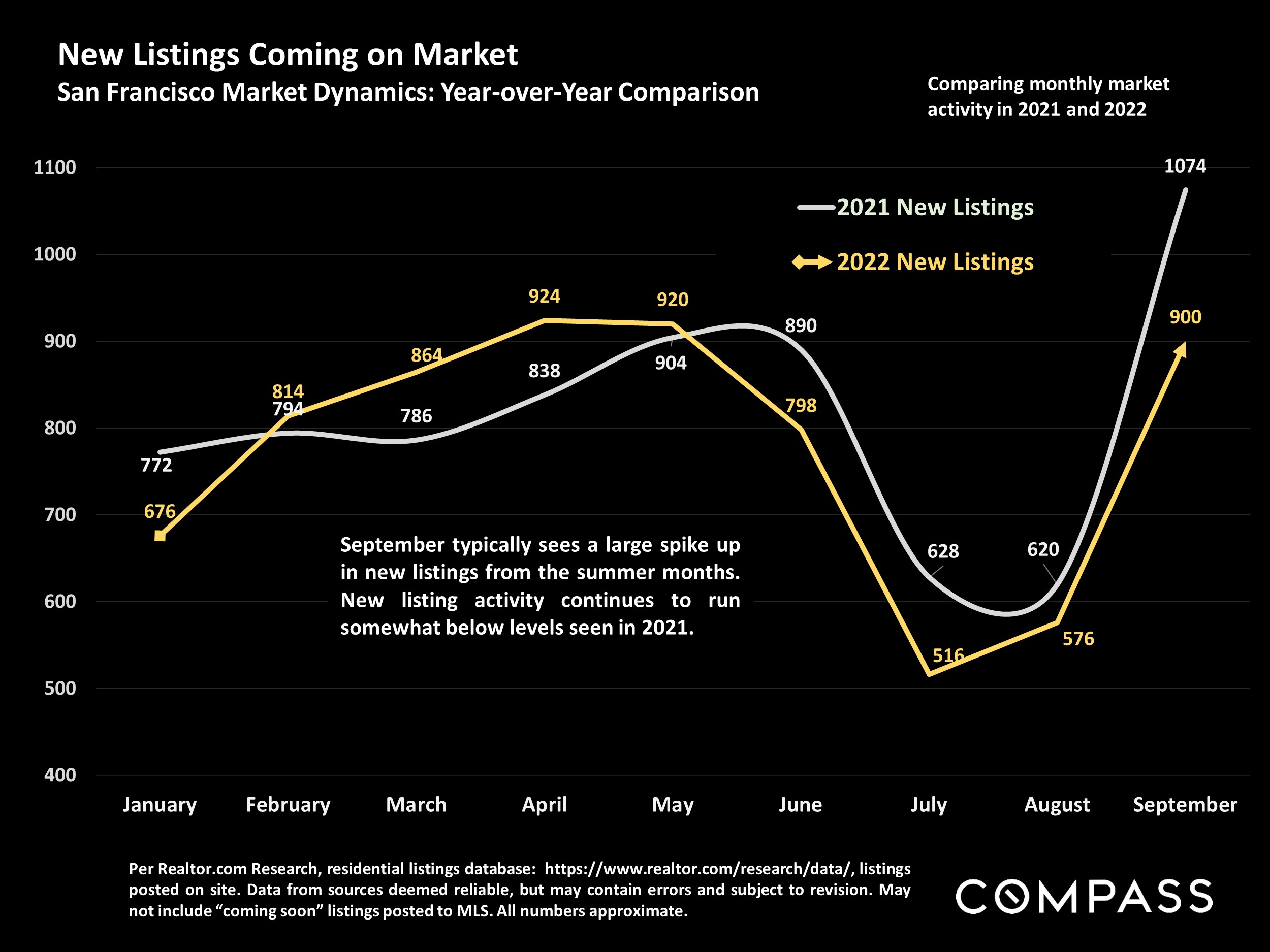

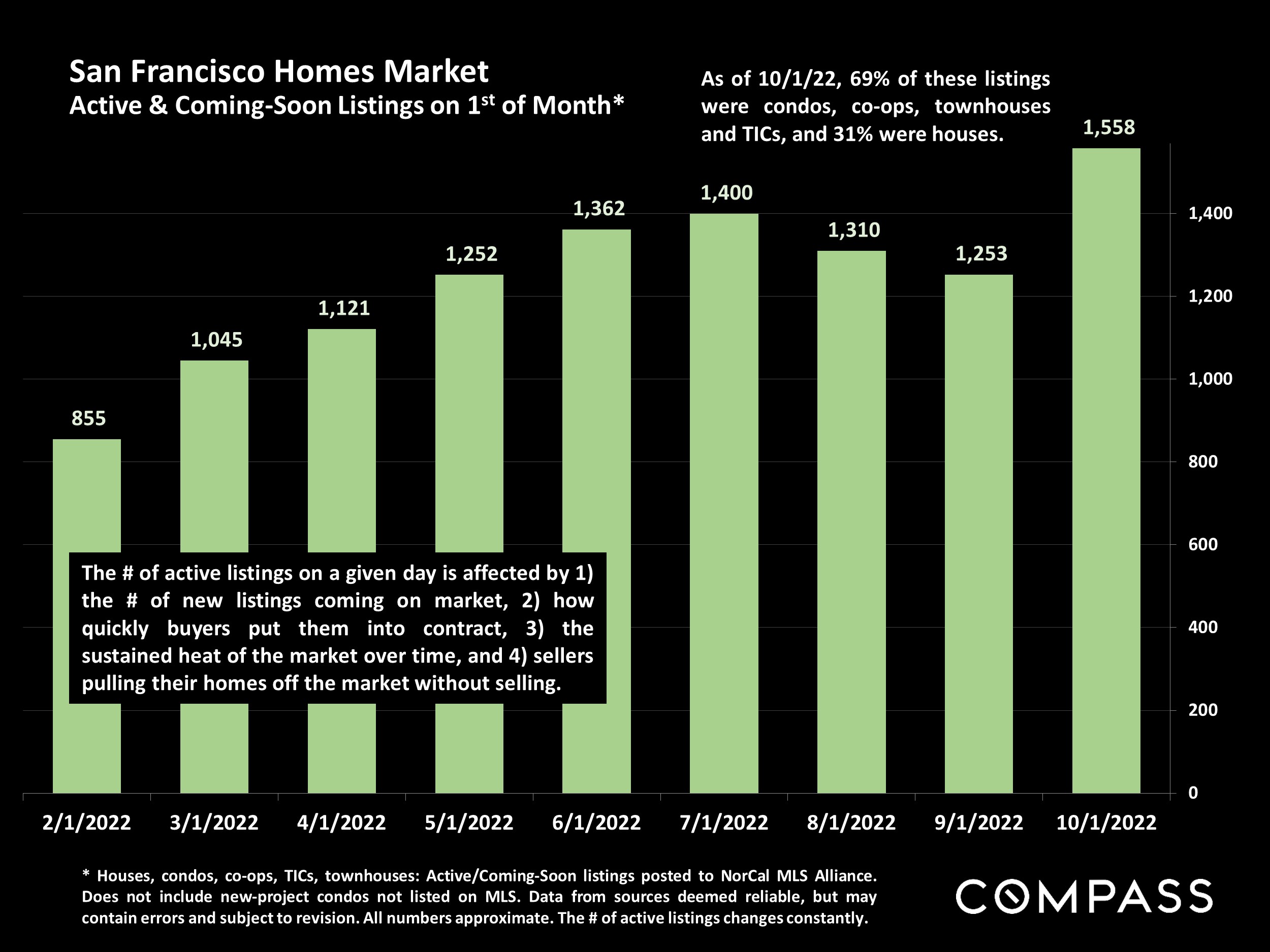

(A) While we haven't seen a wild surge of desperate sellers (new listing numbers are actually down from last year), I have been able to spot some very motivated sellers and help my buyers secure sizeable price discounts. I'm talking paying the same price as sellers did 5, 6, even 7 years ago.

(B) You can still get a low interest rate. I have lenders who have helped my recent buyers secure 30-yr fixed interest rates right around 4%! Ask me for details.

(C) Perhaps most pertinent to the posed question: the fundamentals of the current housing market are strong. Comparisons with the crash of 2008 continue to be made, but the precipitating factors in the 2008 crash - tens of millions of households talked into home loans they could never afford, forcing a tsunami of frantic sales (foreclosures, short-sales, etc) during the great recession - simply does not apply today. Mortgage payments as a percentage of income, and loan delinquency rates are both close to all-time lows, and most homeowners' mortgages are held at historically low rates. Stock market declines, though substantial, cannot compare with those seen in 2008-2009, and employment remains very strong.

(D) In summary, getting a better than average interest rate + a great deal on equity, in a perpetually low inventory, global market like San Francisco = an absolute homerun in the long term. Even if you don't get an interest rate below 6%, now can still be a great time to buy because of the available discounts on equity. The advantages of securing a low purchase price can't be understated (don't forget you lock in a lower property tax payment too!), and you can always refinance in the future.

It's a great time to be pre-approved, in-sync with your agent about your specific needs and goals, and keeping your eyes peeled for the right opportunity to pounce on. There's many I know of right now, and I'll be happy to share them with you.

Sincerely,

Recent reviews, sales, and active listings @ the bottom

|

Recent Sales / In-Contract

|

208 North Lake Merced Hills, Unit 4D

|

3 Bed | 3 Bath | SOLD $1,910,000

|

2 Bed | 2 Bath | SOLD $1,025,000

|

355 1st Street, Unit S1107

2 Bed | 2 Bath | SOLD $1,225,000

|

3 Bed | 2.5 Bath | SOLD $1,850,000

|

3136 Fulton Street, Unit 1

4 Bed | 3.5 Bath SOLD $1,715,000

|

|

2920 Buchanan Street, Unit 3

|

|

101 Lombard Street, Unit 402W

|

3136 Fulton Street, Unit 2

|

|

marketingcenter-sfbayarea-sfcityproper |