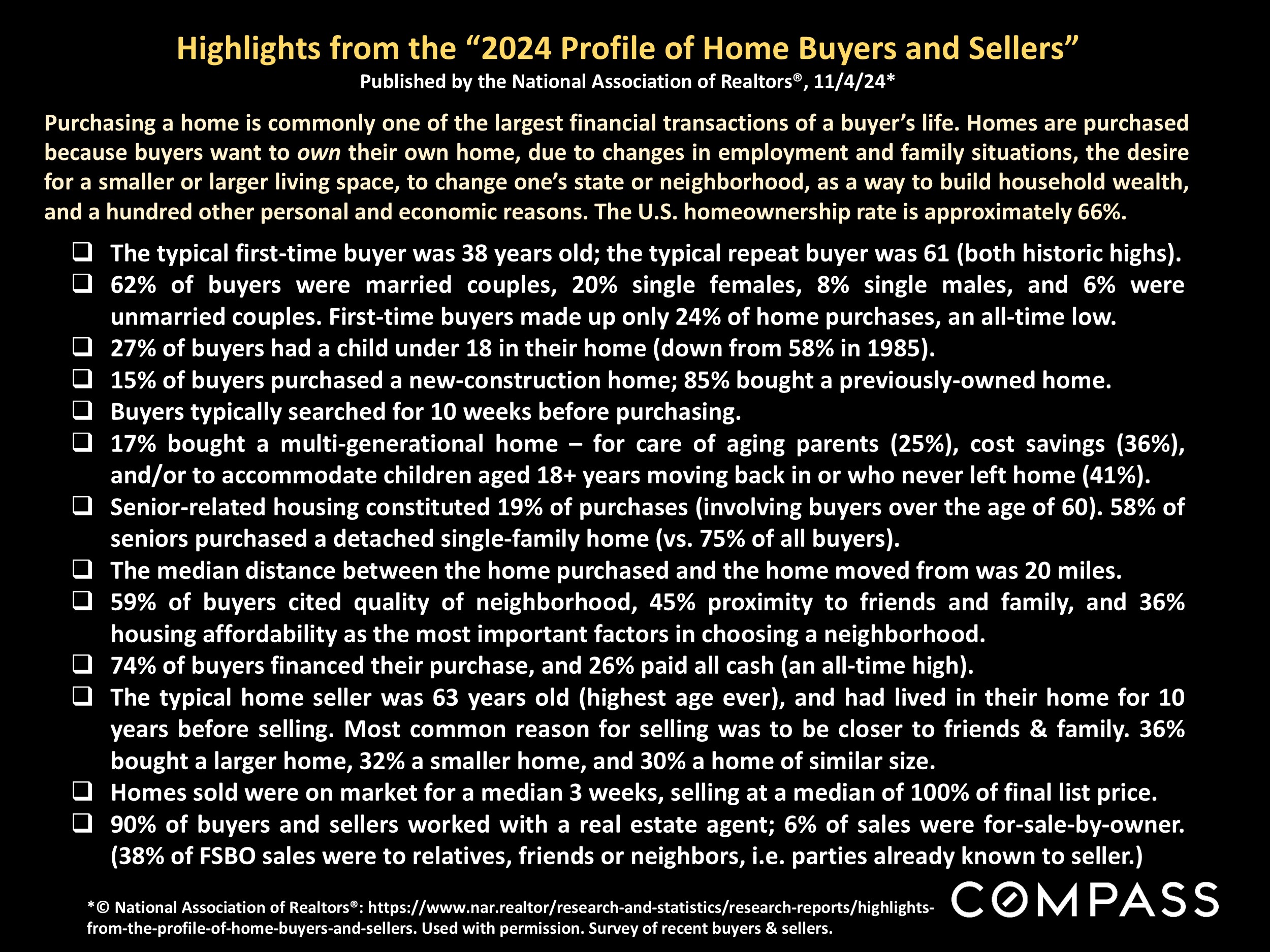

Clients, friends, and colleagues:

Near the end of November, markets around the Bay Area began moving into the mid-winter holiday slowdown (December typically results in the lowest counts of the year for new listings and homes going into contract). Homes are still listed and deals continue to be made, just at a much slower pace. And as I always tell my clients, this is usually the period where buyers can negotiate most aggressively on unsold properties with longer days on market.

It is difficult to make definitive determinations about where the market is heading in 2025 from Q4 statistics, but in the last several years, demand rebounded substantially early in the new year and then accelerated into spring. And many of us agents have reported a significant increase in clients wanting to list their homes next year. As always, much depends on political and macroeconomic factors that are challenging to predict.

As of last week - inflation ticked up slightly to 2.7% while the core CPI remained unchanged at 3.3%.

Interest rates have ticked down a bit, mostly in the mid 6s, though there are great incentives with certain institutions that can help get your rate down (contact me for more information).

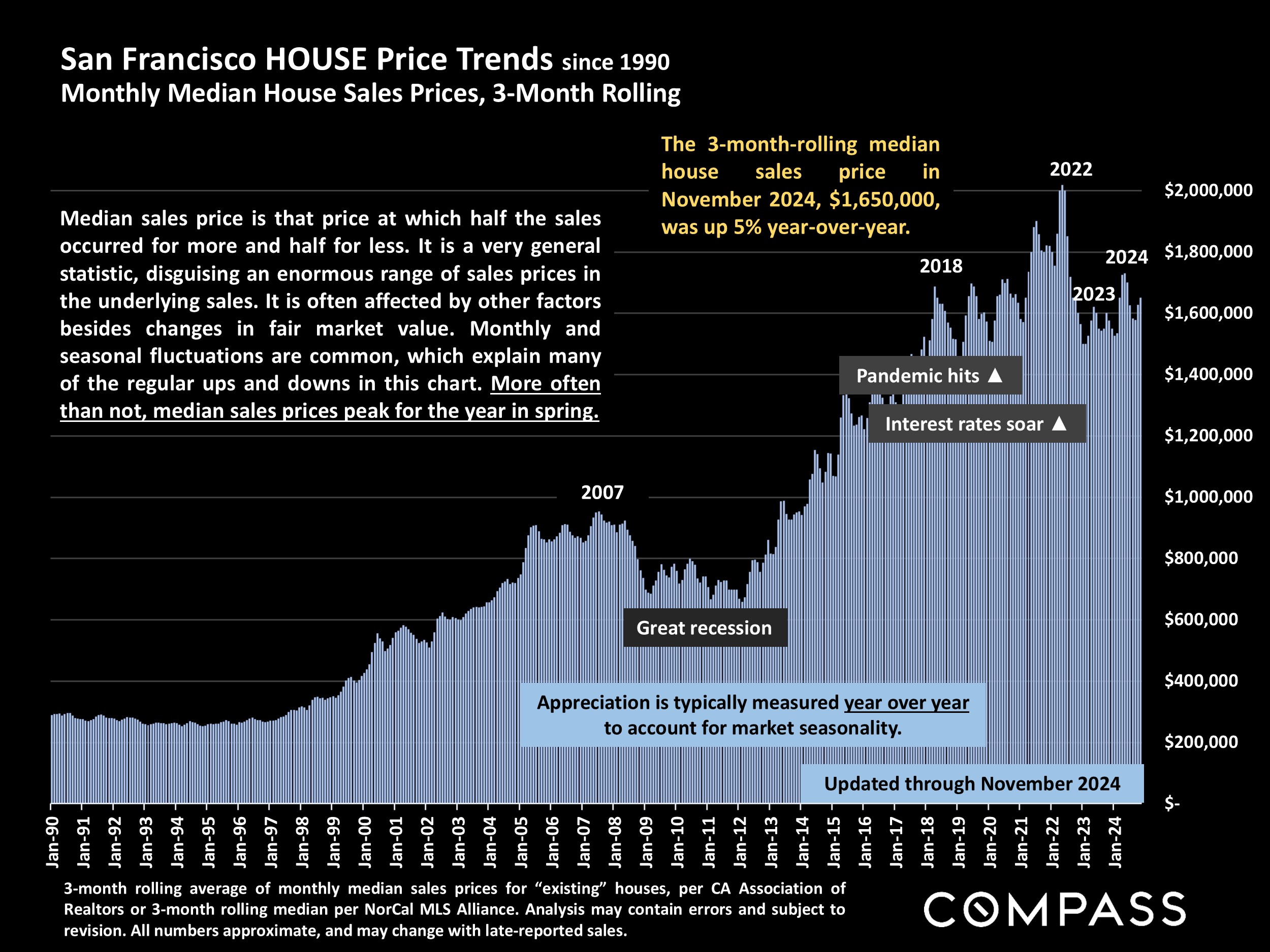

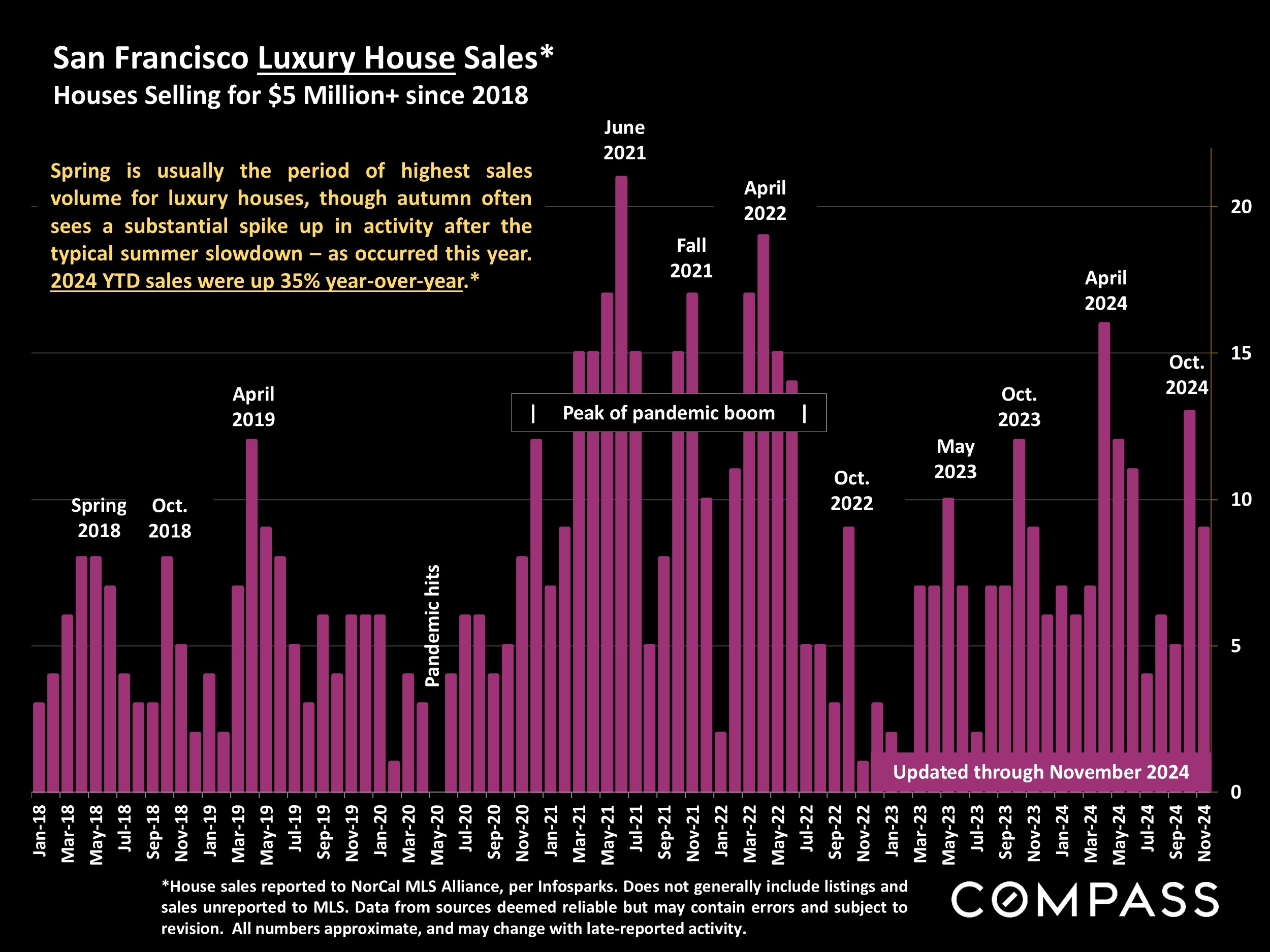

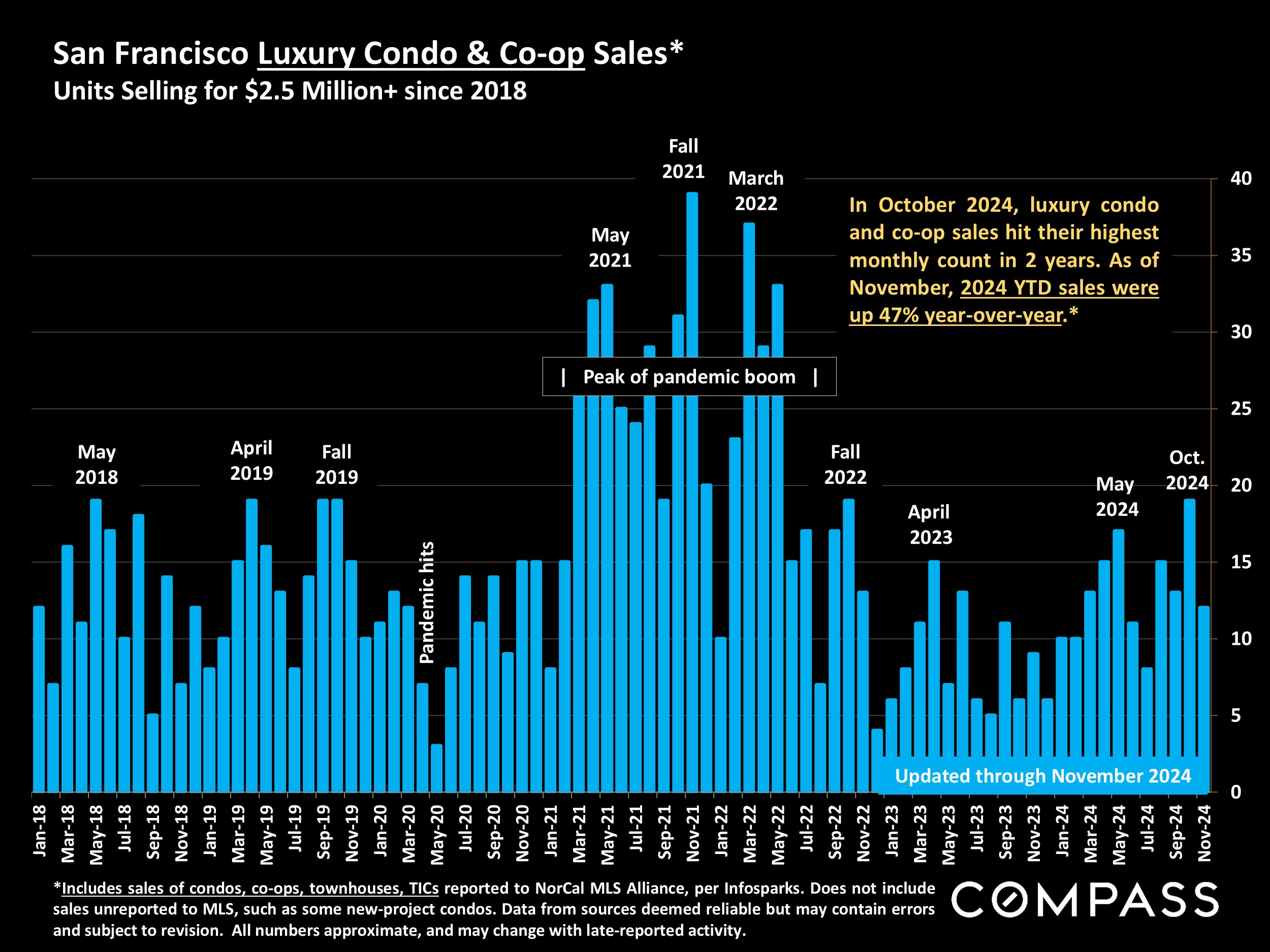

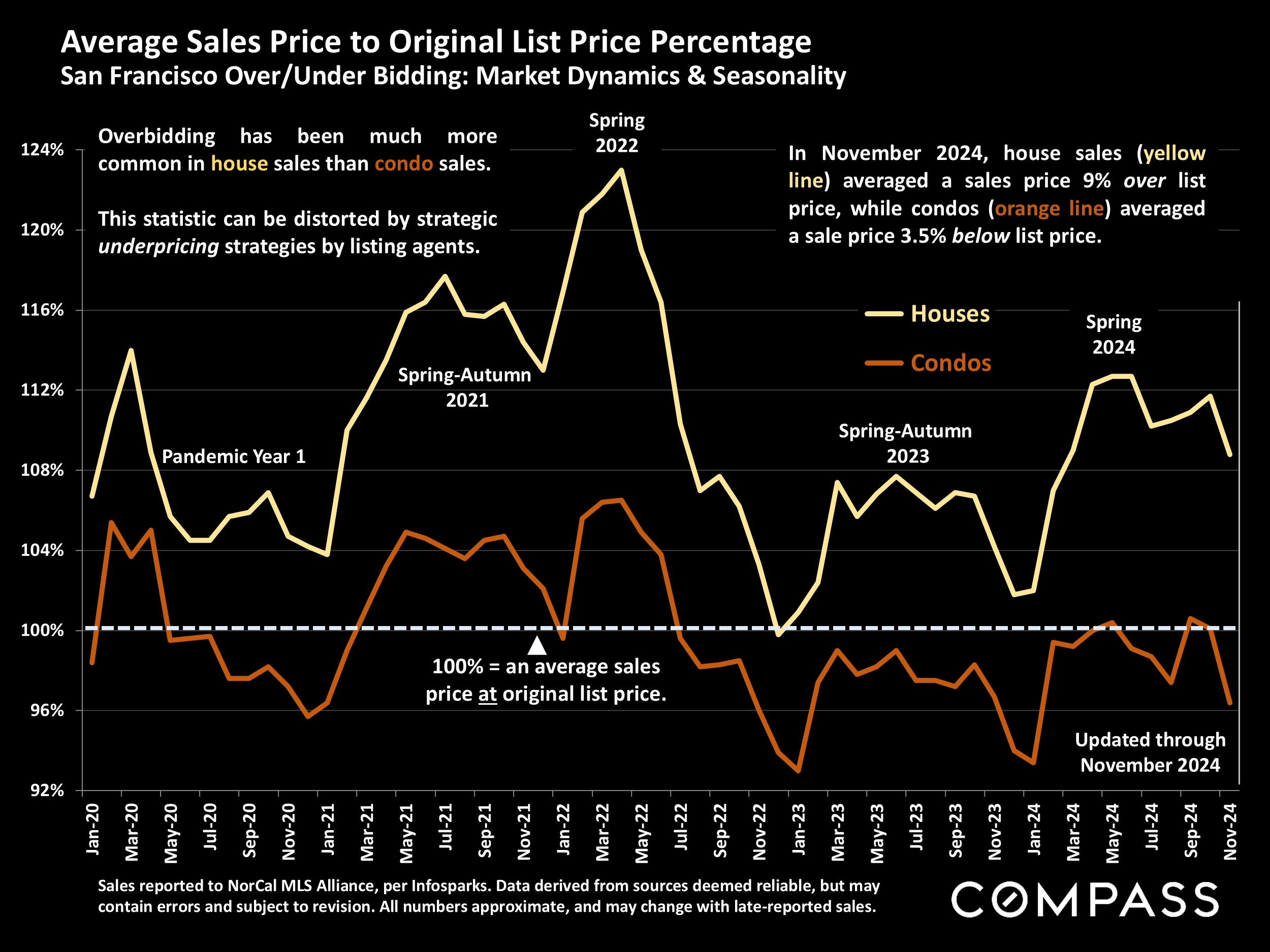

This report will look at supply and demand dynamics recorded in November - but always note that these are lagging indicators: November data primarily reflects listings that went into contract in October.

A couple quick tidbits before we jump into the data:

In totality, stock markets have continued to their rise (Dow is +16% YTD; Nasdaq is +36% YTD; S&P is +28% YTD).

The Fed dropped their benchmark rate another 0.25% (11/7/2024).

Consumer confidence hit its highest reading in 7 months on 12/6/2024.

If you have any questions about the general market or specific property, I am always here and happy to assist.

Wishing you all a wonderfuly holiday season!

Warmly,

Ron