| |

|

|

|

|

San Francisco Market Update

|

|

Clients, friends, and colleagues:

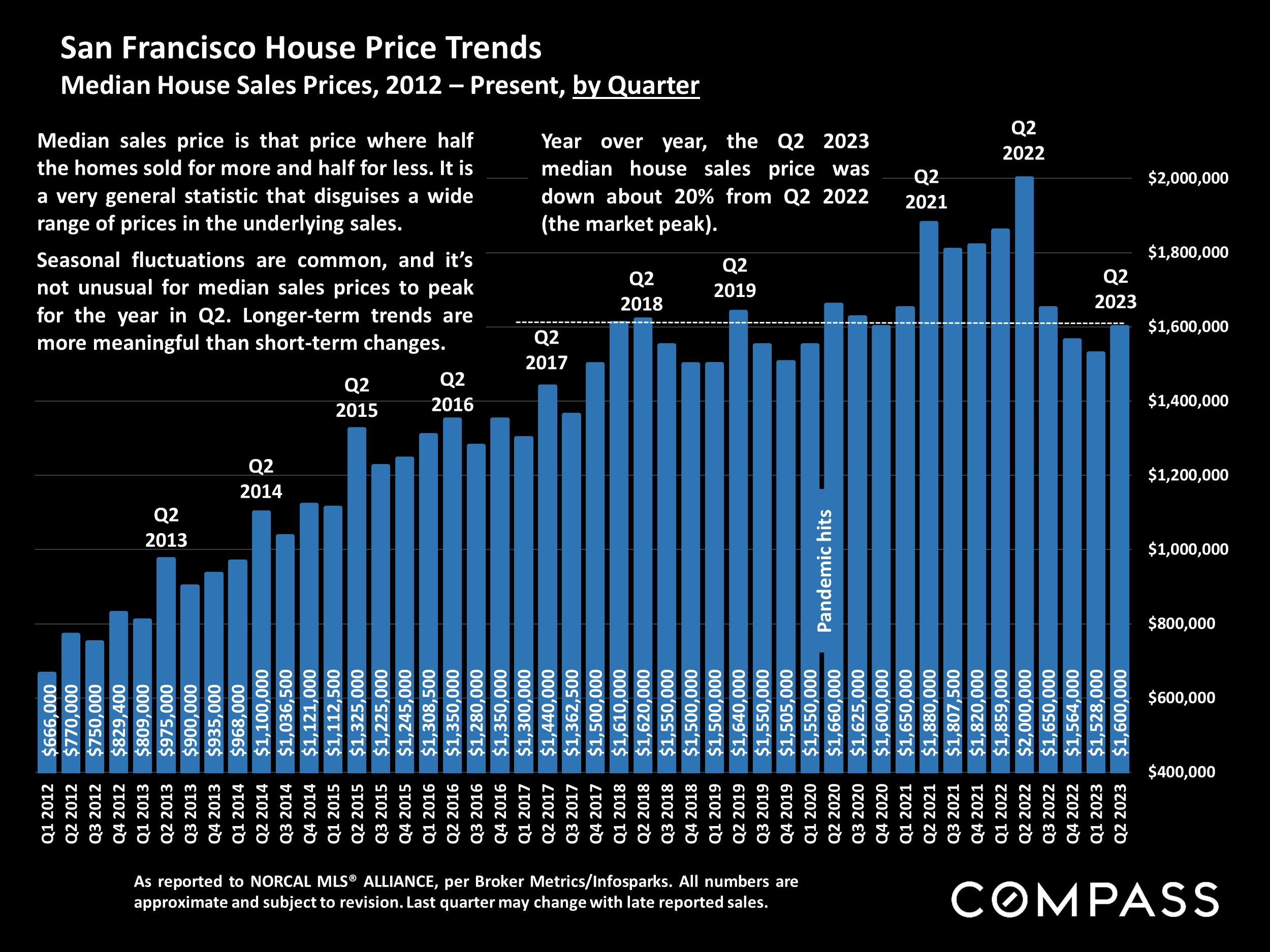

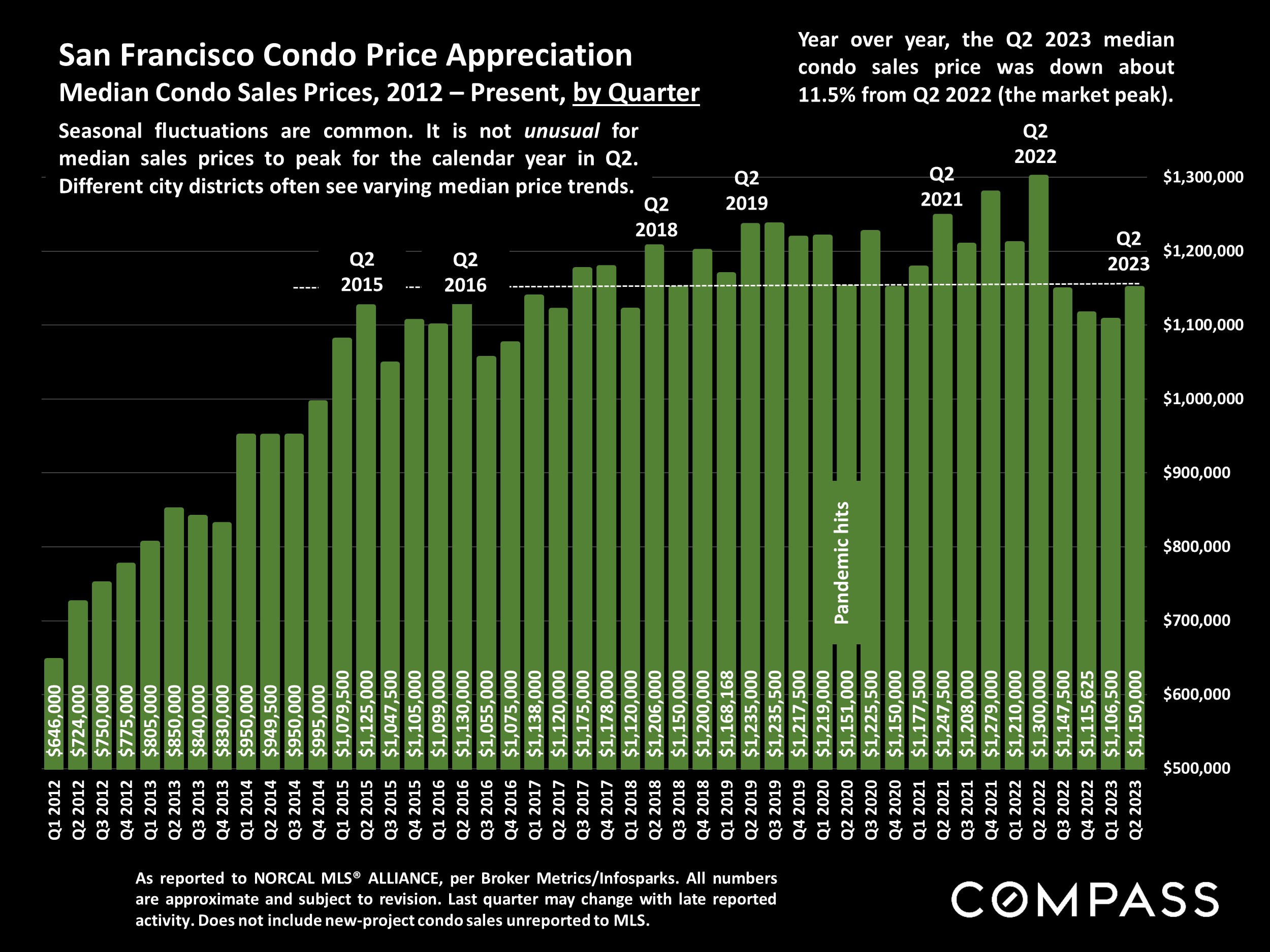

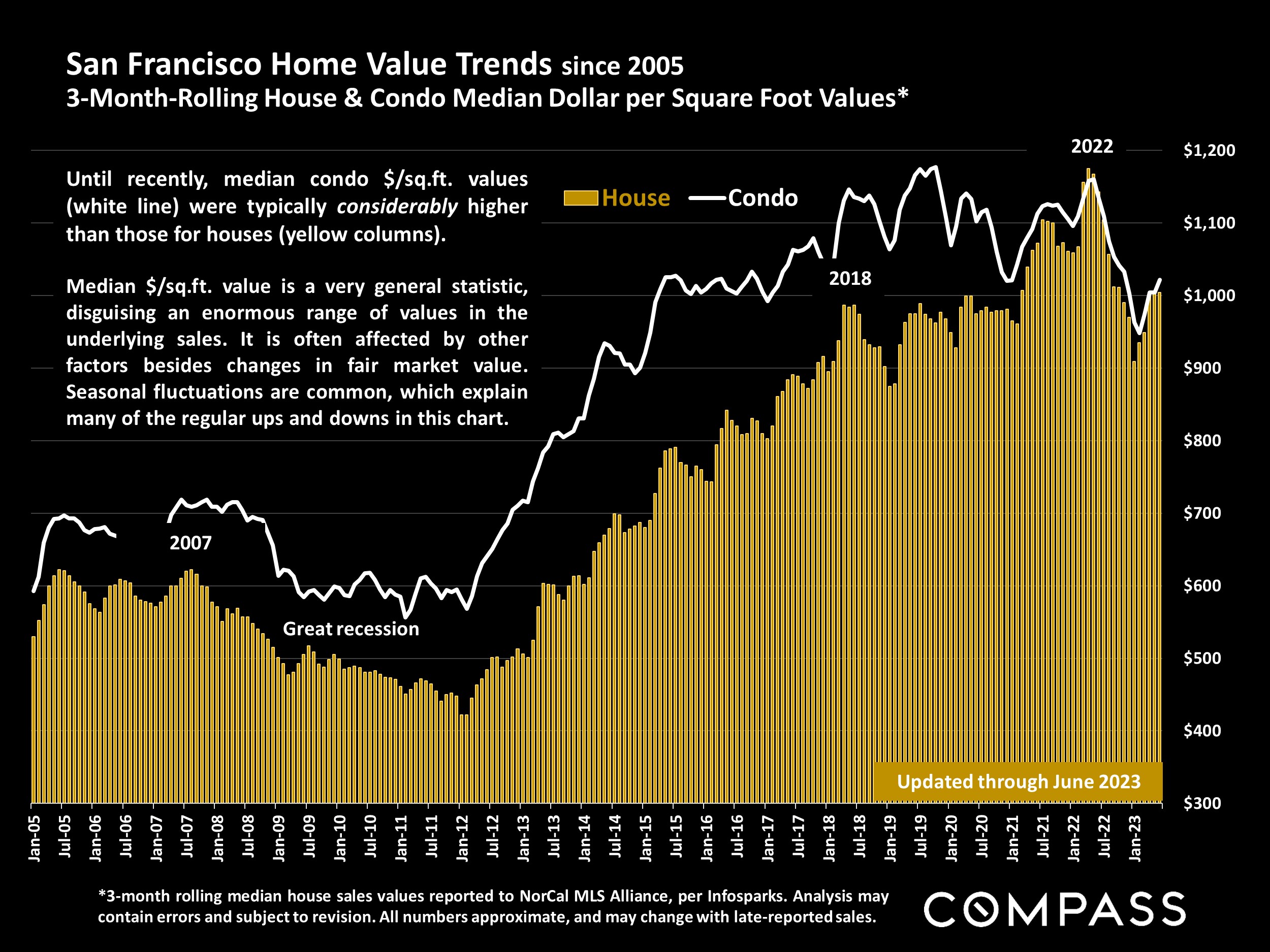

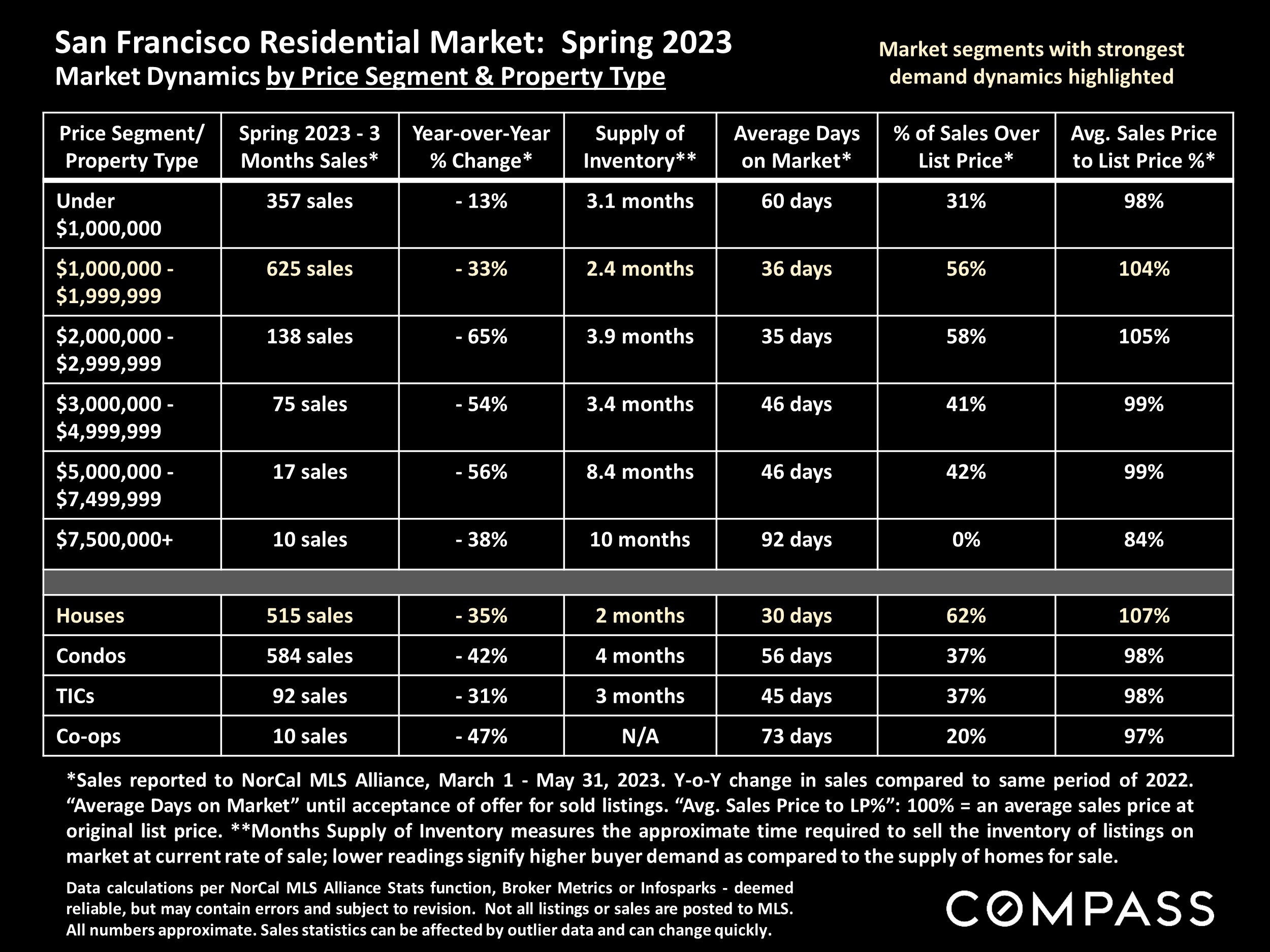

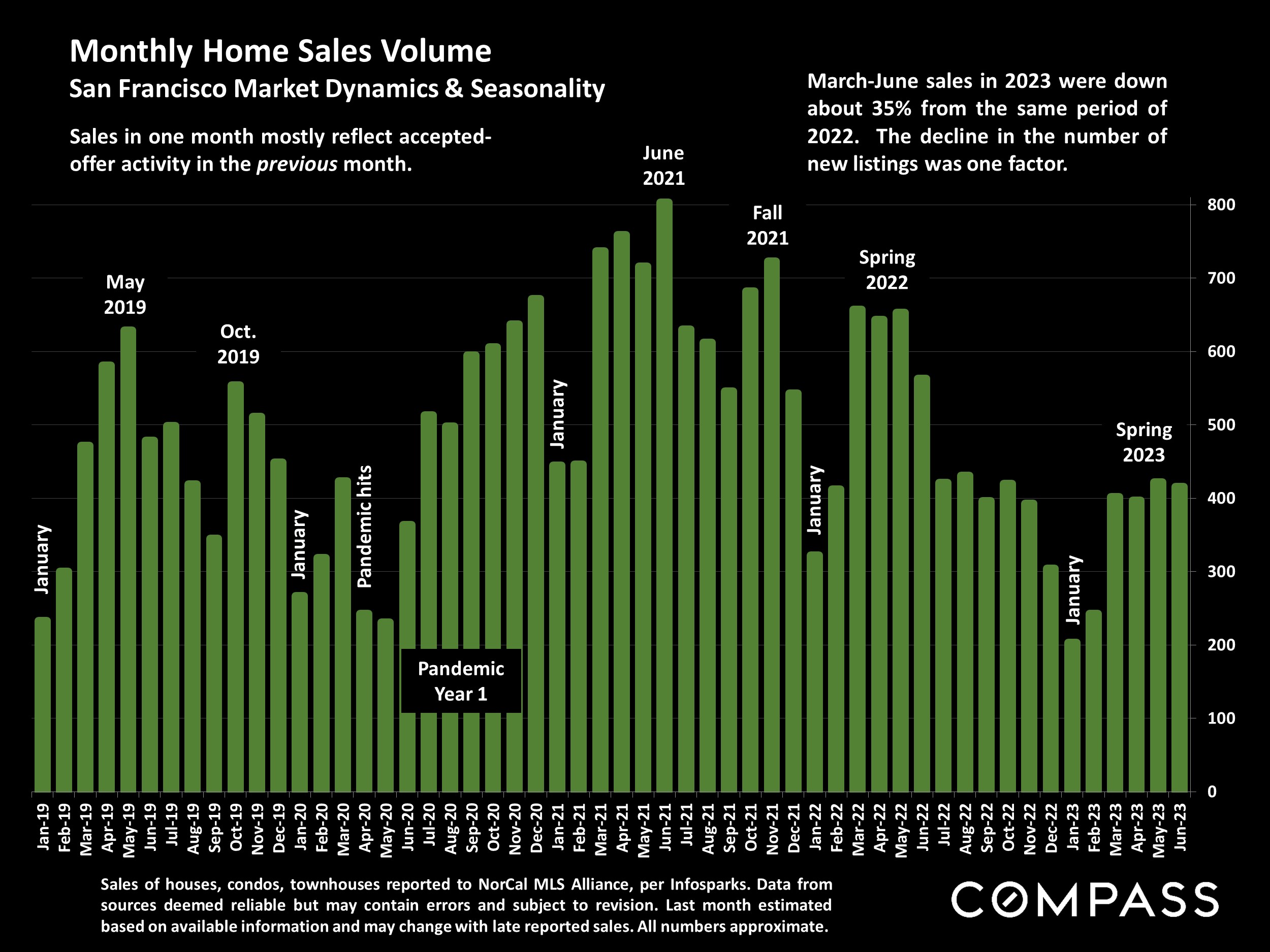

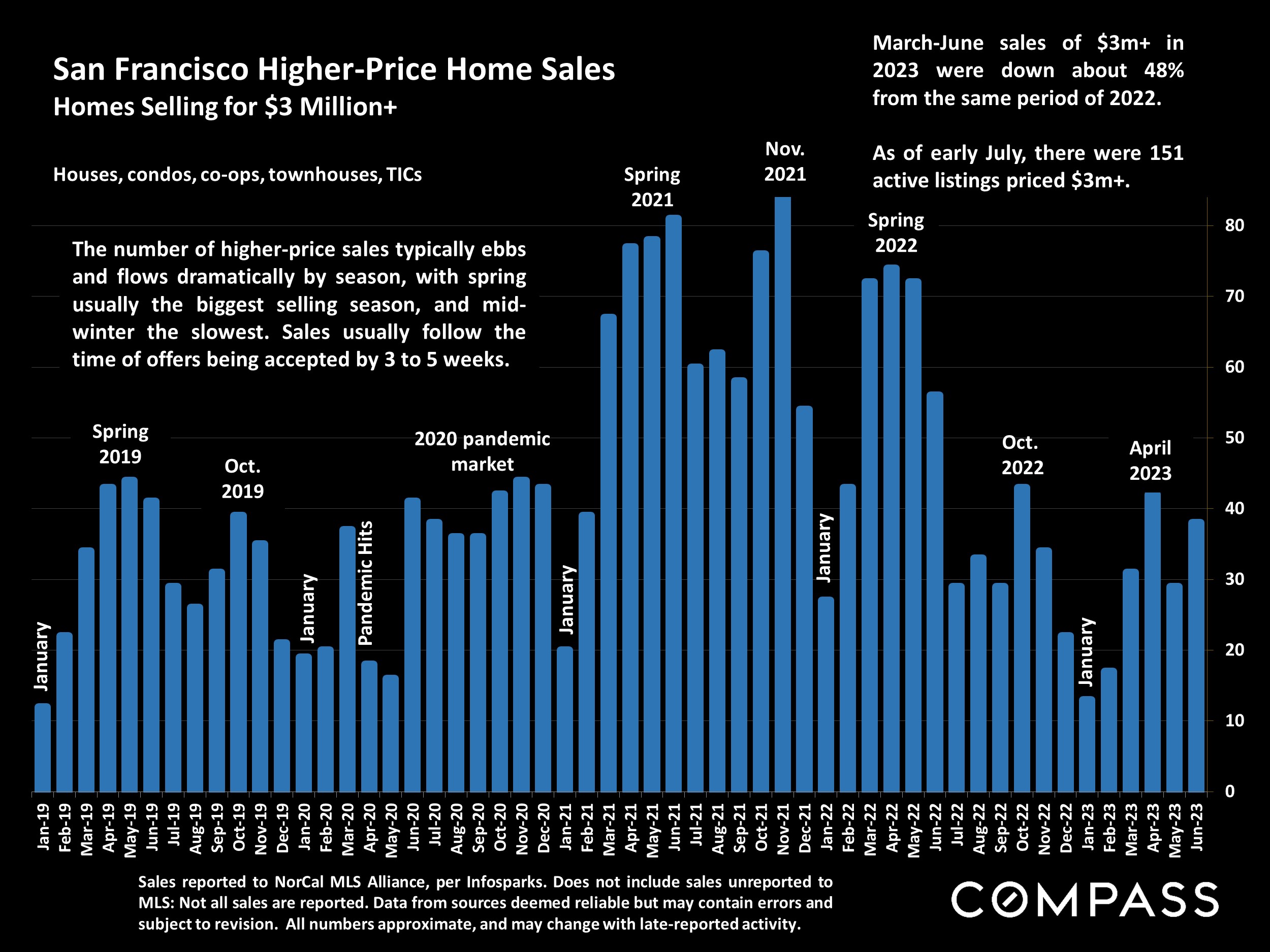

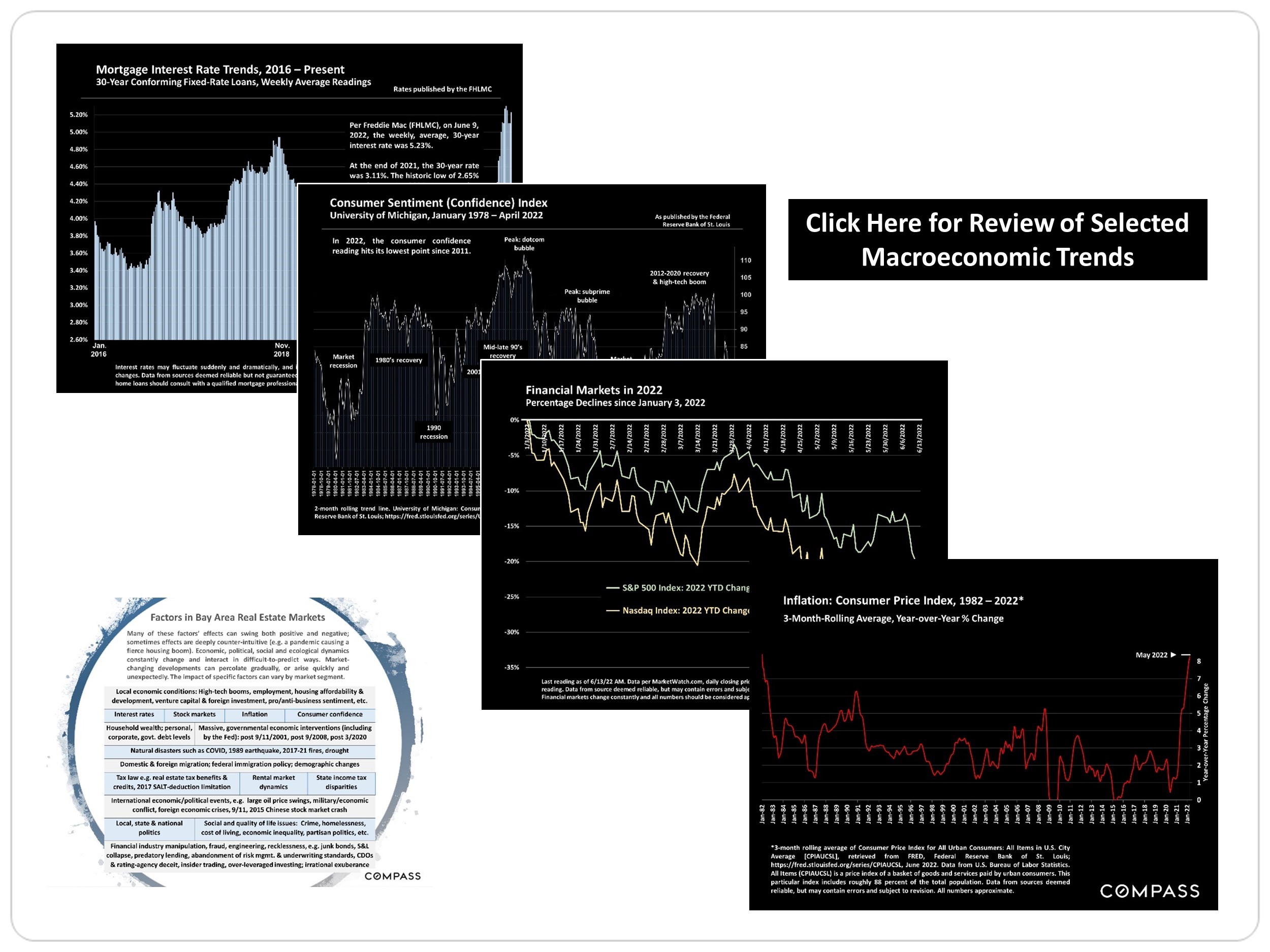

Underlying market and economic dynamics in 2023 have been a mixed bag of often contrary and volatile factors - including downward-trending inflation; interest rates still bouncing between 6% and 7%; general uncertainy regarding what the Fed will do next (next meeting this Wednesday); substantial rebounds in stock markets; banks, commercial real estate, and debt-default crises; international political, economic, and military conflicts; high-tech left amid generally very strong employment statistics; and a recovery in buyer demand, sales activity and home prices, but all 3 remaining significantly lower than the peak of the market in spring 2022. And within the city, market conditions of course vary by property type (houses generally seeing higher demand), neighborhood (the downtown market remains relatively weak), and/or price segment within types and locations.

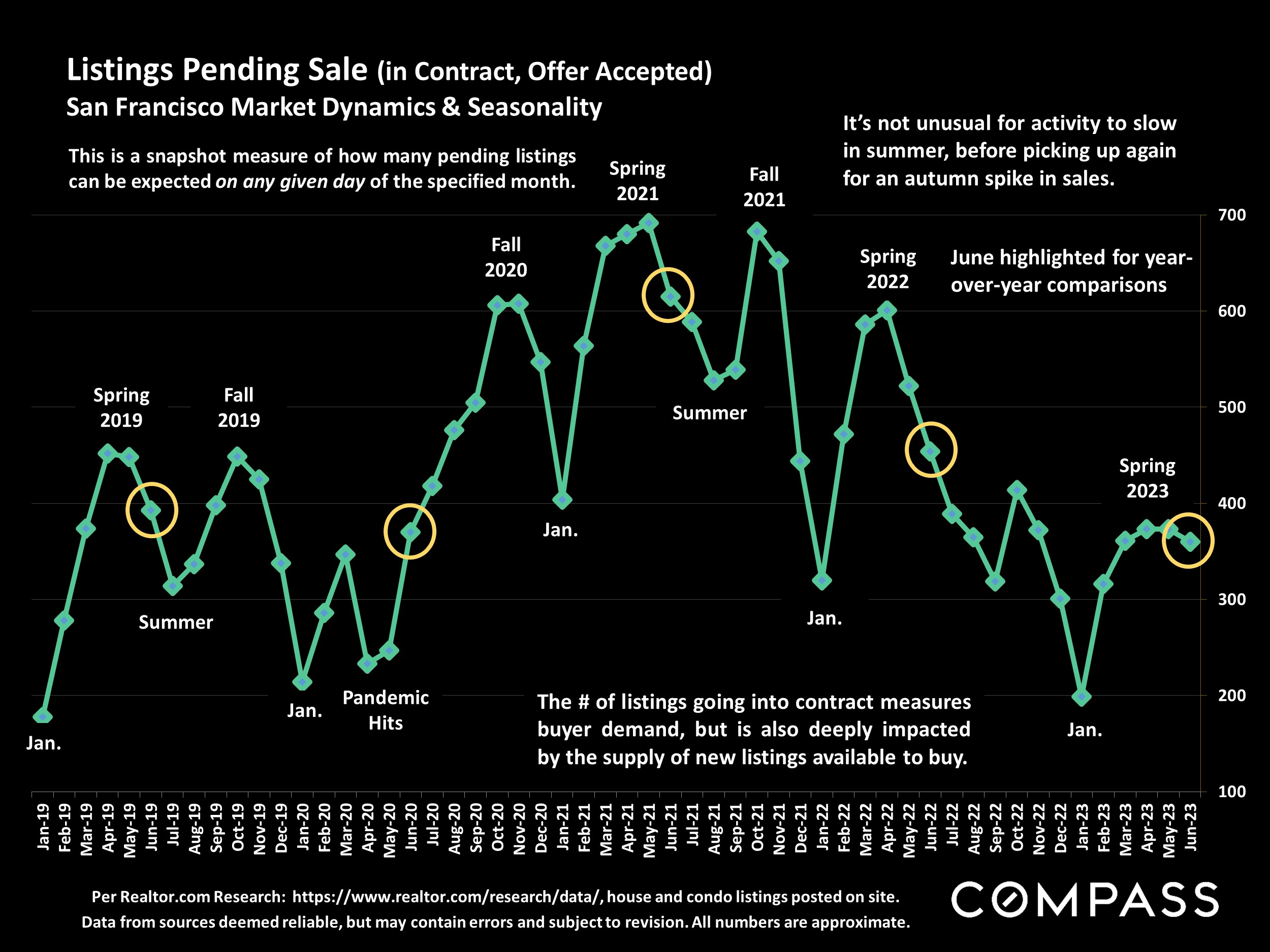

Ultimately, the market is defined by neither just demand nor supply, but by the balance between the two. As we've moved deeper into 2023, that balance has generally titled to sellers' advantage, with homes selling faster, with more offers, for higher prices. Part of this is due to seasonal dynamics: Spring is commonly the highest-demand, most active selling season of the year. But the contrast with the 2nd half of 2022, when demand and sales plunged, is more than seasonal. It also reflects a rebound in psychology, with many buyers deciding to move forward with their life plans.

For most Bay Area markets, summer has historically been a slower period after spring - with some regions such as San Francisco, seeing a relatively short (6-8 week) spike up in activity in autumn before the big midwinter slowdown - but typical seasonal trends have been upended a few times in recent years. Certainly, a substantial amount of buying and selling will continue to occur in coming months, as well as variations in underlying economic conditions, which we will cover in detail in future reports.

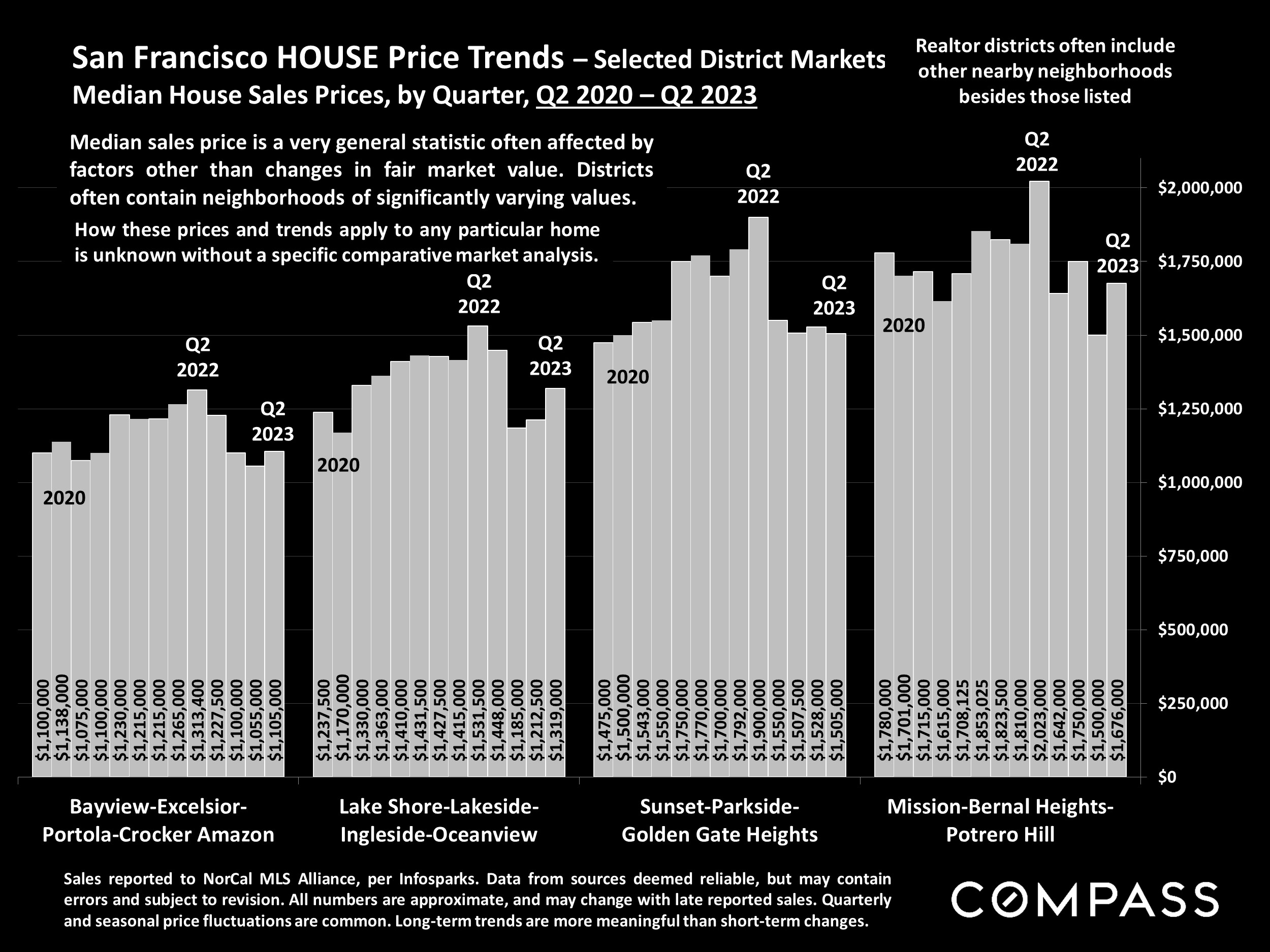

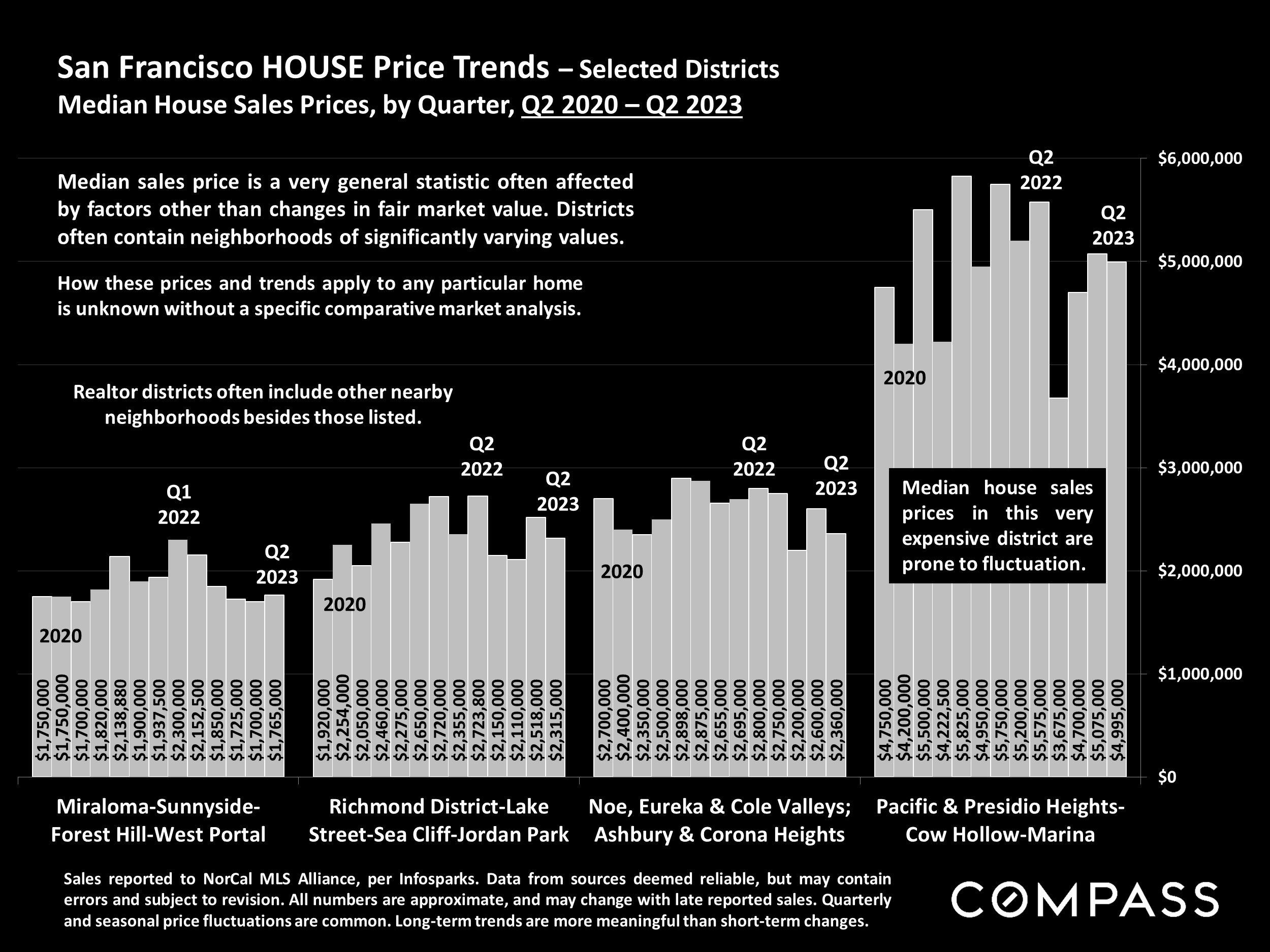

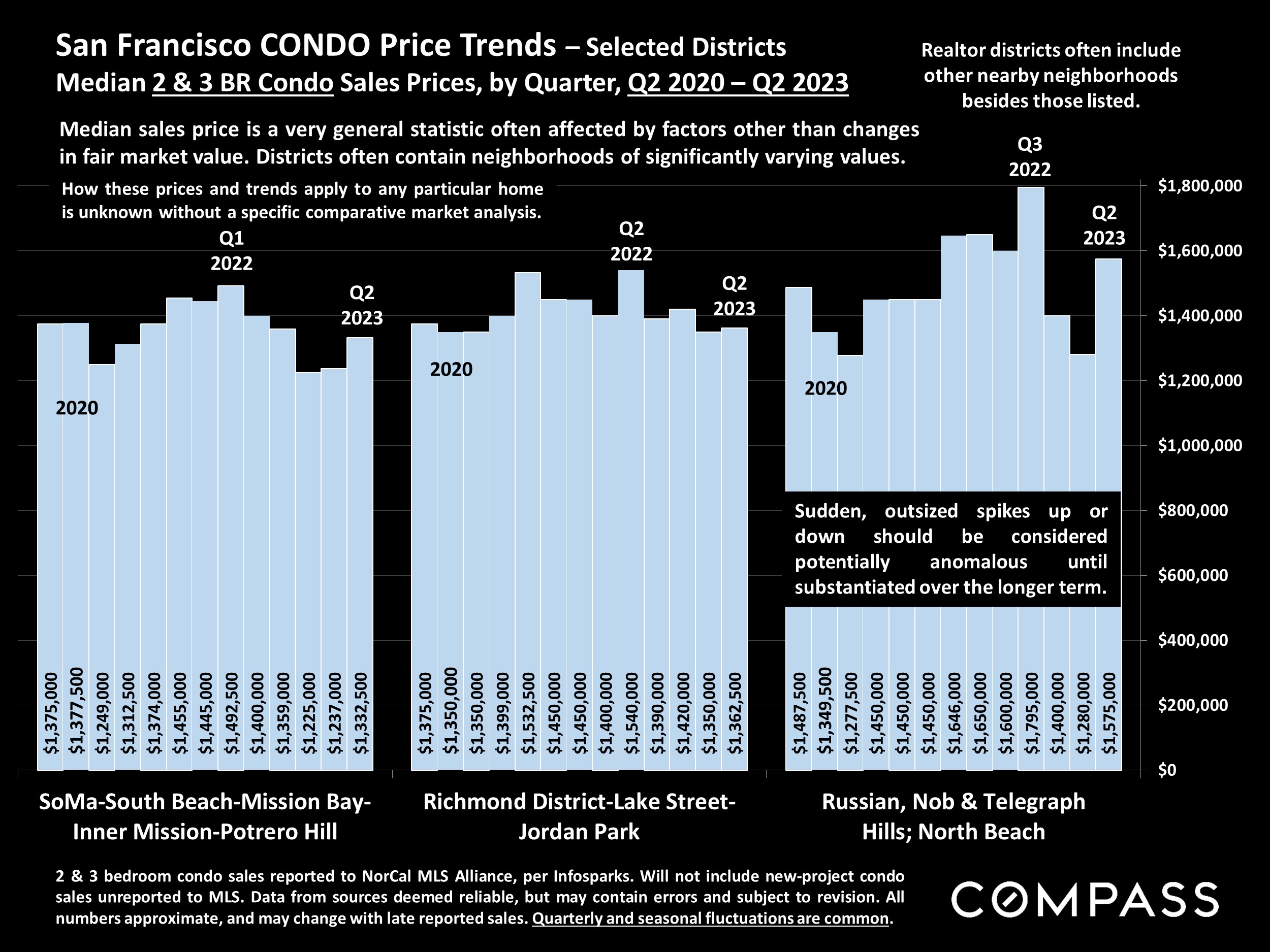

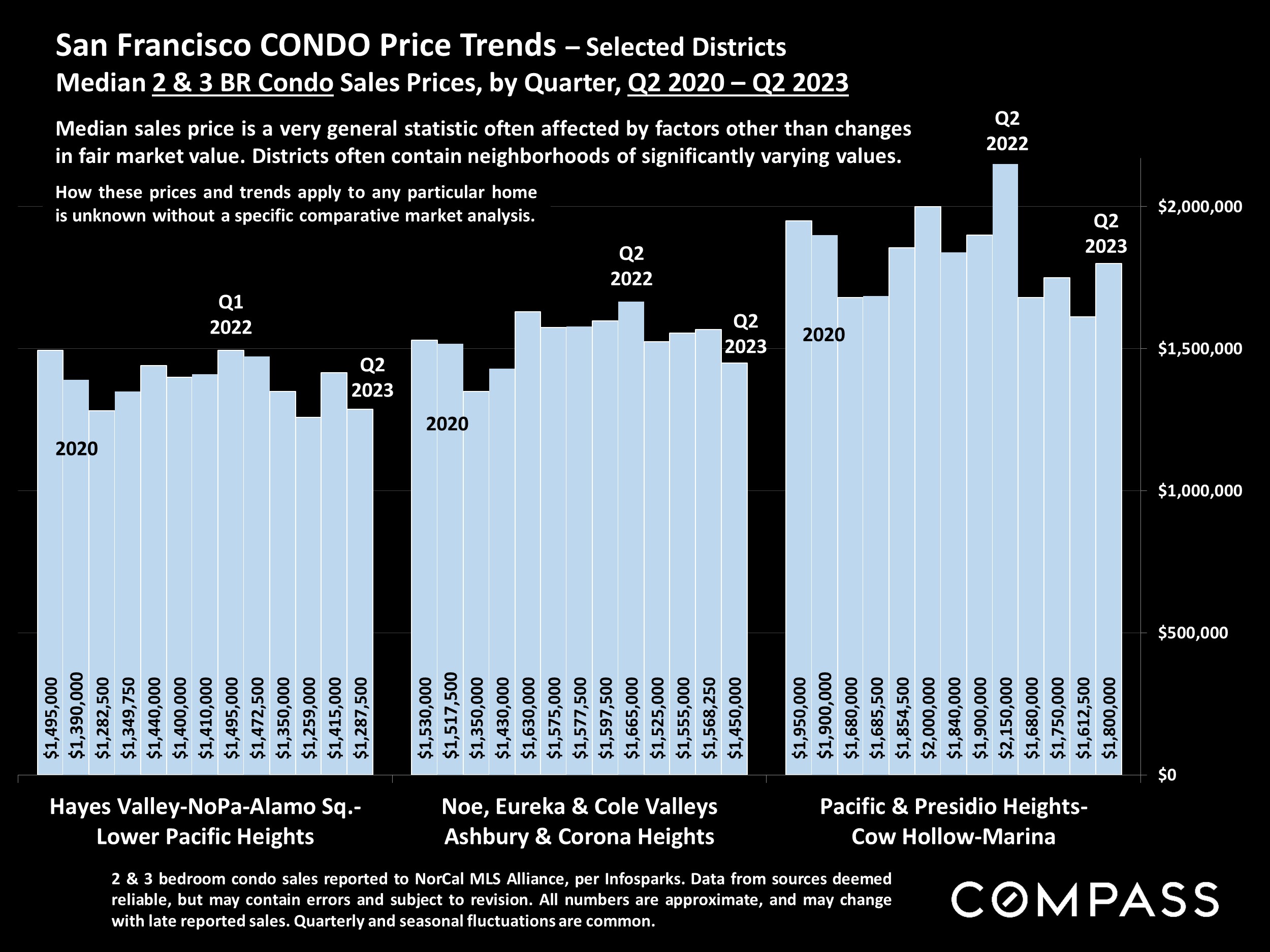

Summary of some Key Metrics recorded for June 2023 in San Francisco

Single-Family: $1,600,000 (-20% from June 2022 | +7% from January 2023)

Condos: $1,150,000 (-11.5% from June 2022 | +9.5% from January 2023)

Single-Family: 14 (12 DOM in June 2022 | 24 DOM in January 2023)

Condos: 31 (18 DOM in June 2022 | 54 DOM in January 2023)

Single-Family: 336 (-4.5% from June 2022 | +17% from January 2023)

Condos: 650 (-34% from June 2022 | +11.5% from January 2023)

If you have any questions about a specific property or the general market here in the Bay Area, I'm always here and happy to help!

Recent Contracts, Sales, and Active Listings @ the bottom

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In-Contract / Recent Sales

|

|

|

|

|

|

|

|

|

in contract / South Beach

|

|

280 Spear Street, Unit 29B

|

|

1 BD 1 BA 797 SF $1,165,000

|

|

|

|

|

|

|

|

|

|

|

|

5 BD 4 BA 2327 SF $2,195,000

|

|

|

|

|

|

|

|

|

|

|

2821 Buchanan Street, Unit 34

|

|

3 BD 2 BA 2375 SF $2,700,000

|

|

|

|

|

|

|

|

|

|

2200 Pacific Avenue, Unit 3A

|

|

2 BD 2 BA 1856 SF $1,400,000

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 BD 6 BA 5757 SF $5,995,000

|

|

|

|

|

|

|

|

|

|

260 King Street, Unit 429

|

|

1 BD 1 BA 600 SF $599,000

|

|

|

|

|

|

|

|

|

|

|

1370 Valencia Street, Unit 5

|

|

2 BD 2 BA 1380 SF $1,395,000

|

|

|

|

|

|

|

|

|

|

1 Burnett Avenue North, Unit 9

|

|

3 BD 3 BA 2157 SF $1,750,000

|

|

|

|

|

|

|

|

|

|

|

|

|

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics - such as "active listings," "days on market," and "months supply of inventory" - differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won't be reflected in the data. "Homes" signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, or their MLS areas, unless otherwise delineated. Multicounty metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, "bonus" rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis.

|

|

Compass is a real estate broker licensed by the State of California operating under multiple entities. License Numbers 01991628, 1527235, 1527365, 1356742, 1443761, 1997075, 1935359, 1961027, 1842987, 1869607, 1866771, 1527205, 1079009, 1272467. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions.

|

|

|

|

|

|

|

|

|