|

|

|

|

|

|

Clients, friends, and colleagues,

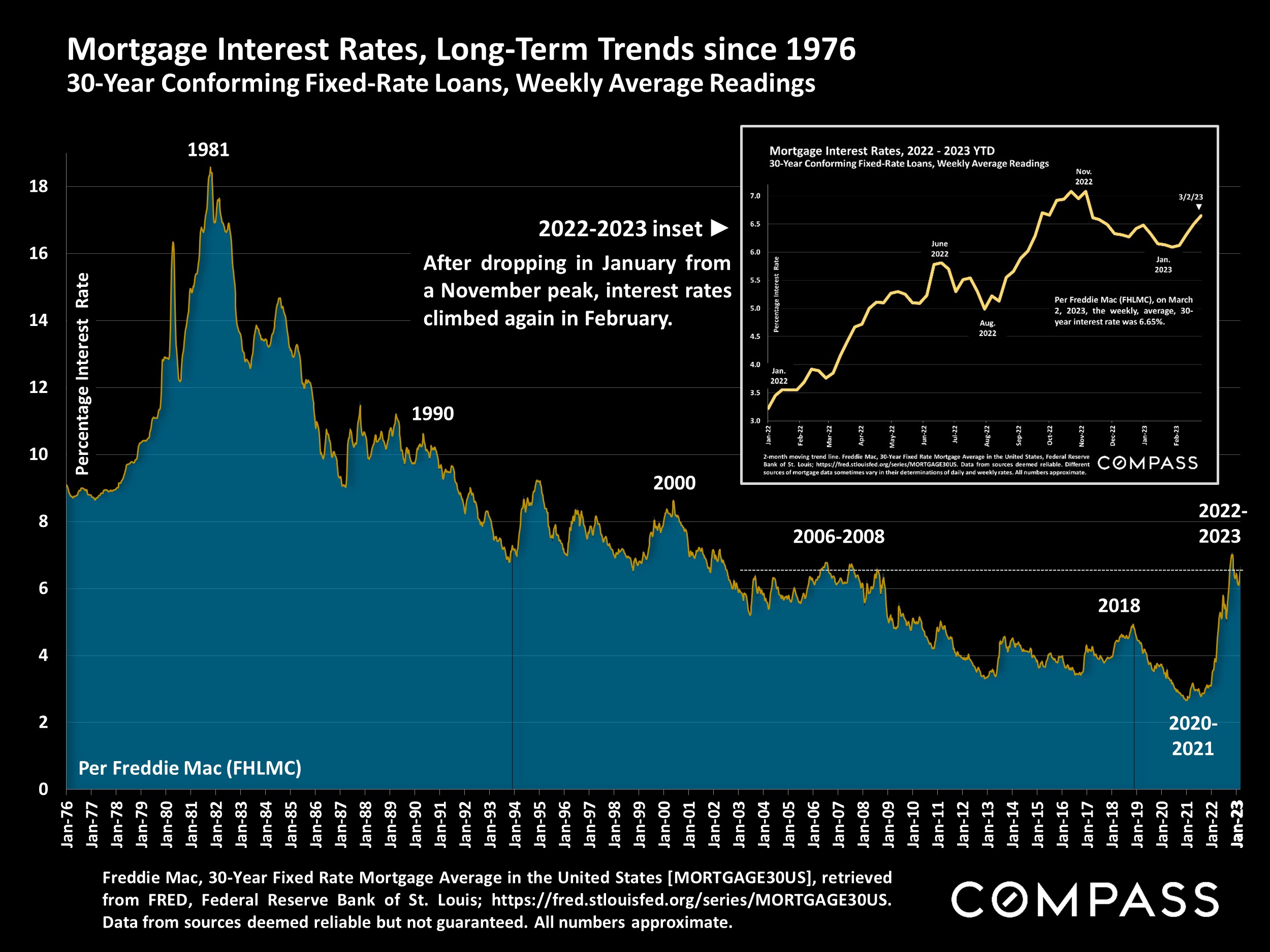

It's been quite the weekend: Silicon Valley Bank fell on Friday, Signature Bank (NY) fell on Sunday, and interest rates are continuing their rise since February (national average sits over 7% for 30-yr fixed).

The good news is that the Fed ensured that all depositors of SVB, including those above the $250K FDIC limit, would be paid back in full. The same was announced for Signature Bank.

Now I'm not a qualified financial executive, but when looking at the reported fundamentals that caused the failure of SVB, it's reassuring that it doesn't look to involve faulty lending standards or fraud (and we all know from '08 how loose lending standards can create catastrophic, systemic failure across Wall Street). SVB had exceptionally high exposure to rising interest rates due to their investment strategy of long-term mortgage bonds and treasuries. Combined with the less plentiful times in the tech/VC world, if customers reached back for their deposits before their investments matured, the bank simply wasn't liquid enough to cover. SVB tried to raise capital after taking a loss on some of their investments, and customers panicked, resulting in a run on the bank.

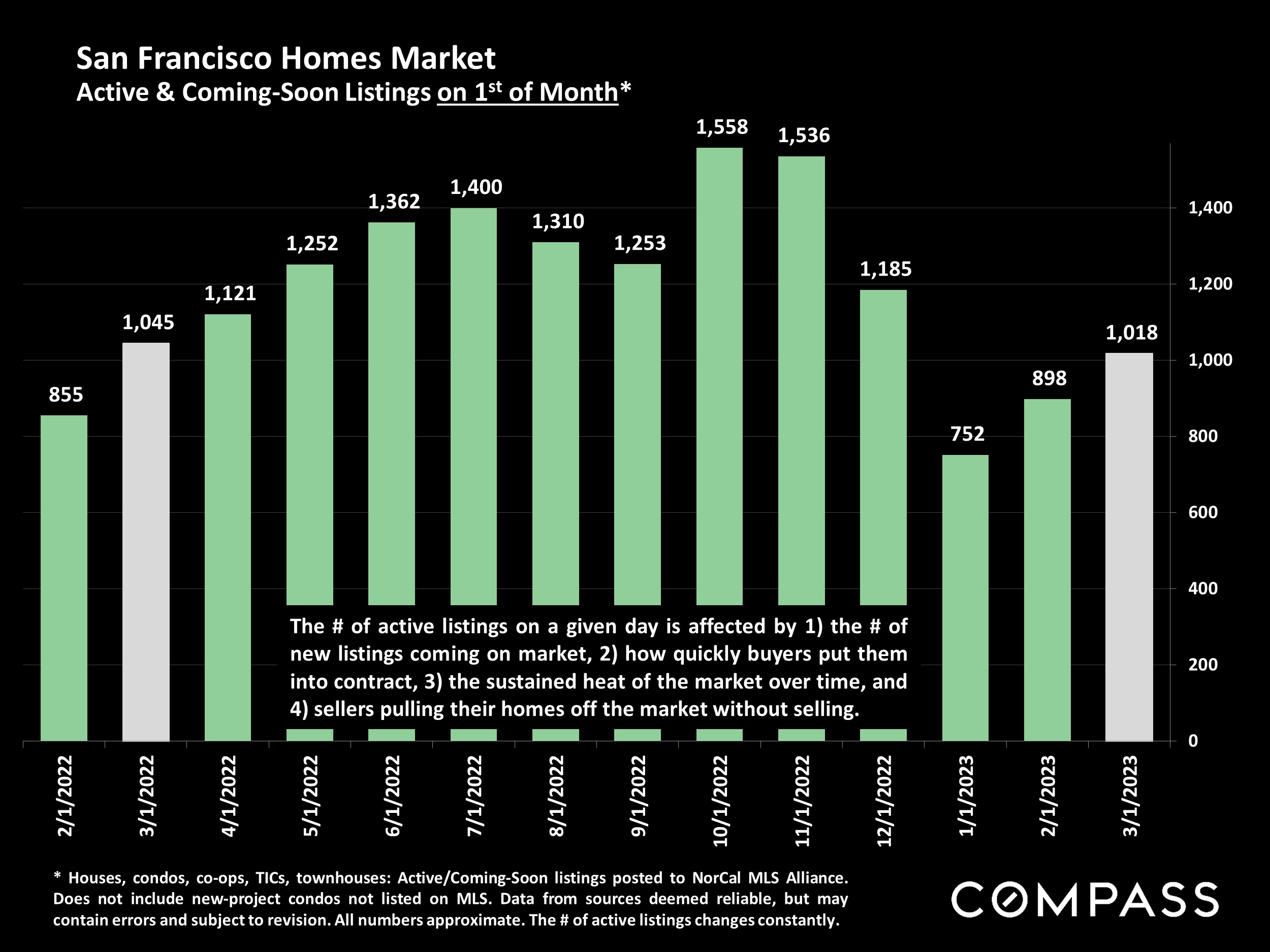

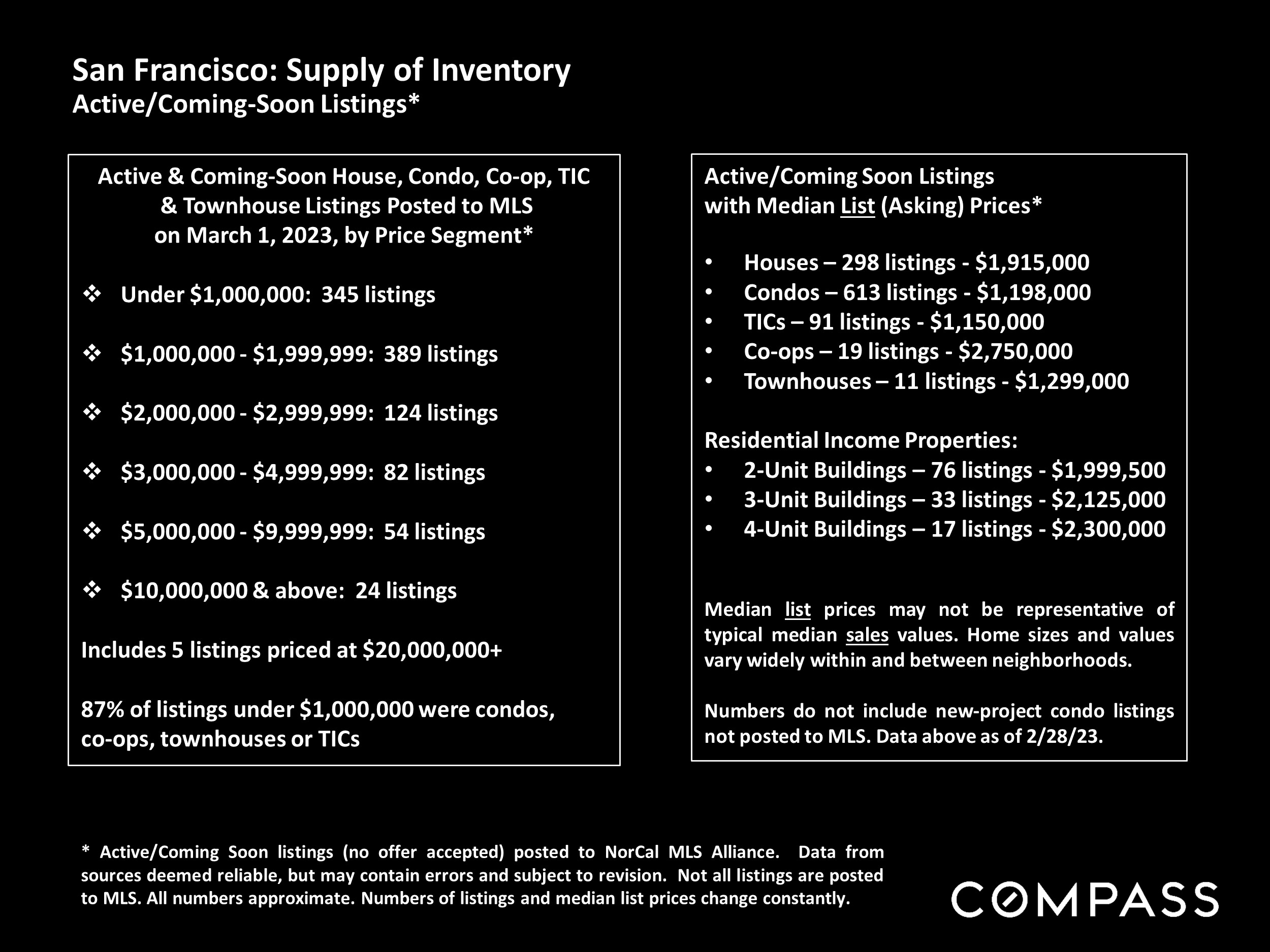

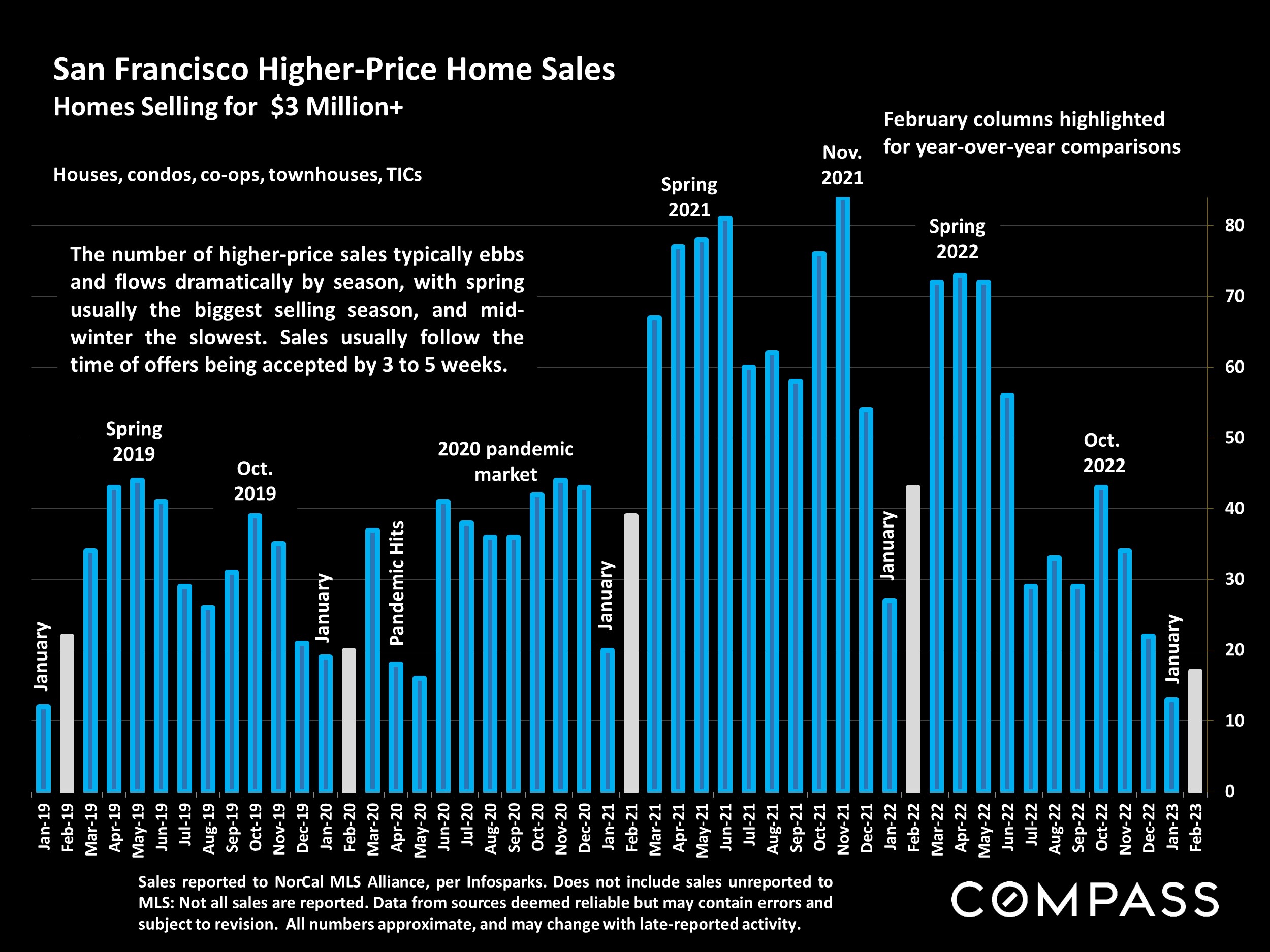

So, how does this impact real estate? More specifically, how does this impact real estate in the Bay Area & San Francisco? The obvious answer is we are way too early to tell and that this is a fluid situation: news is coming out by the minute. What I can offer is some insight into the state of our market right up until the news of SVB on Friday - and the market has certainly rebounded from Q4 2022.

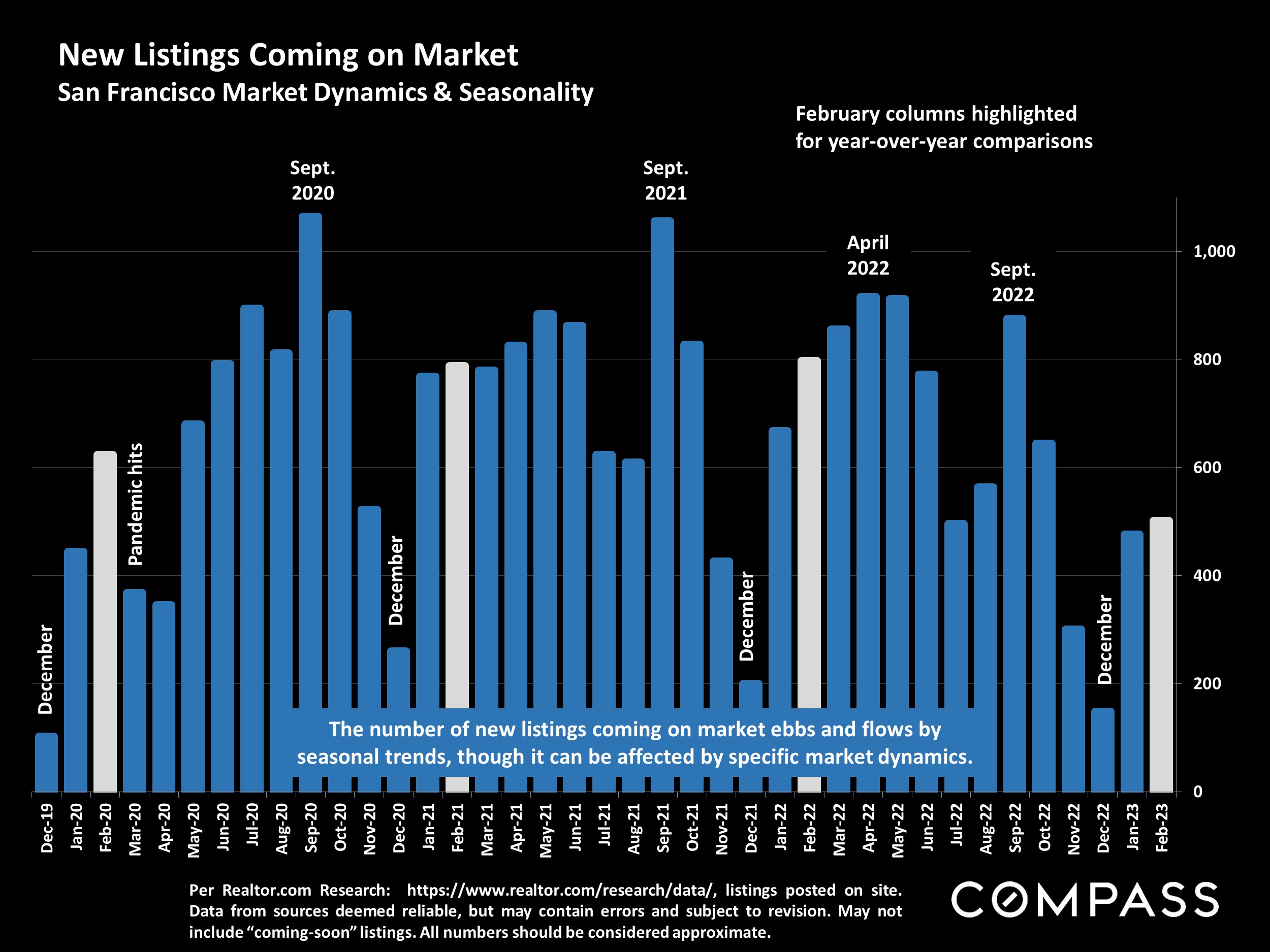

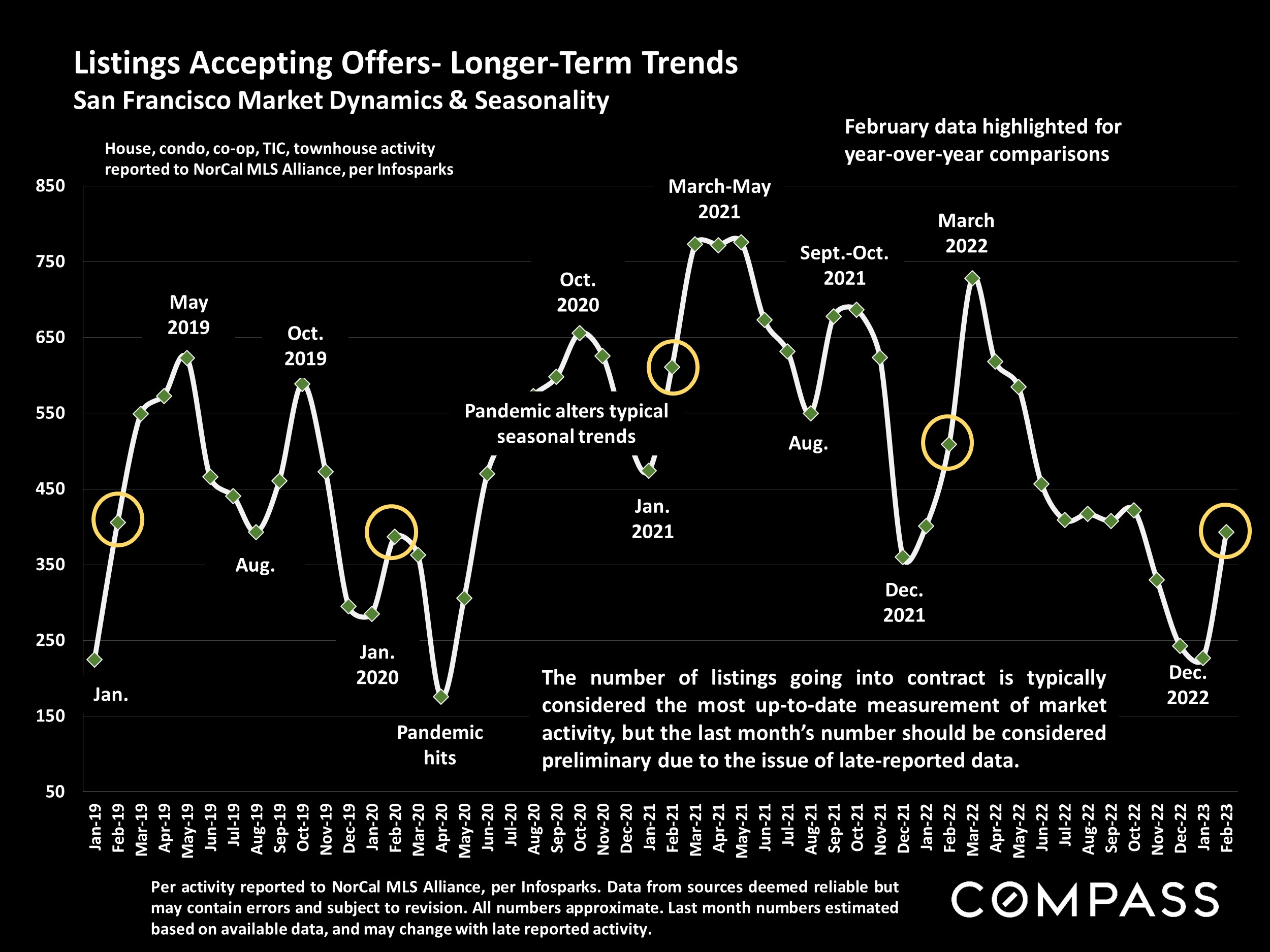

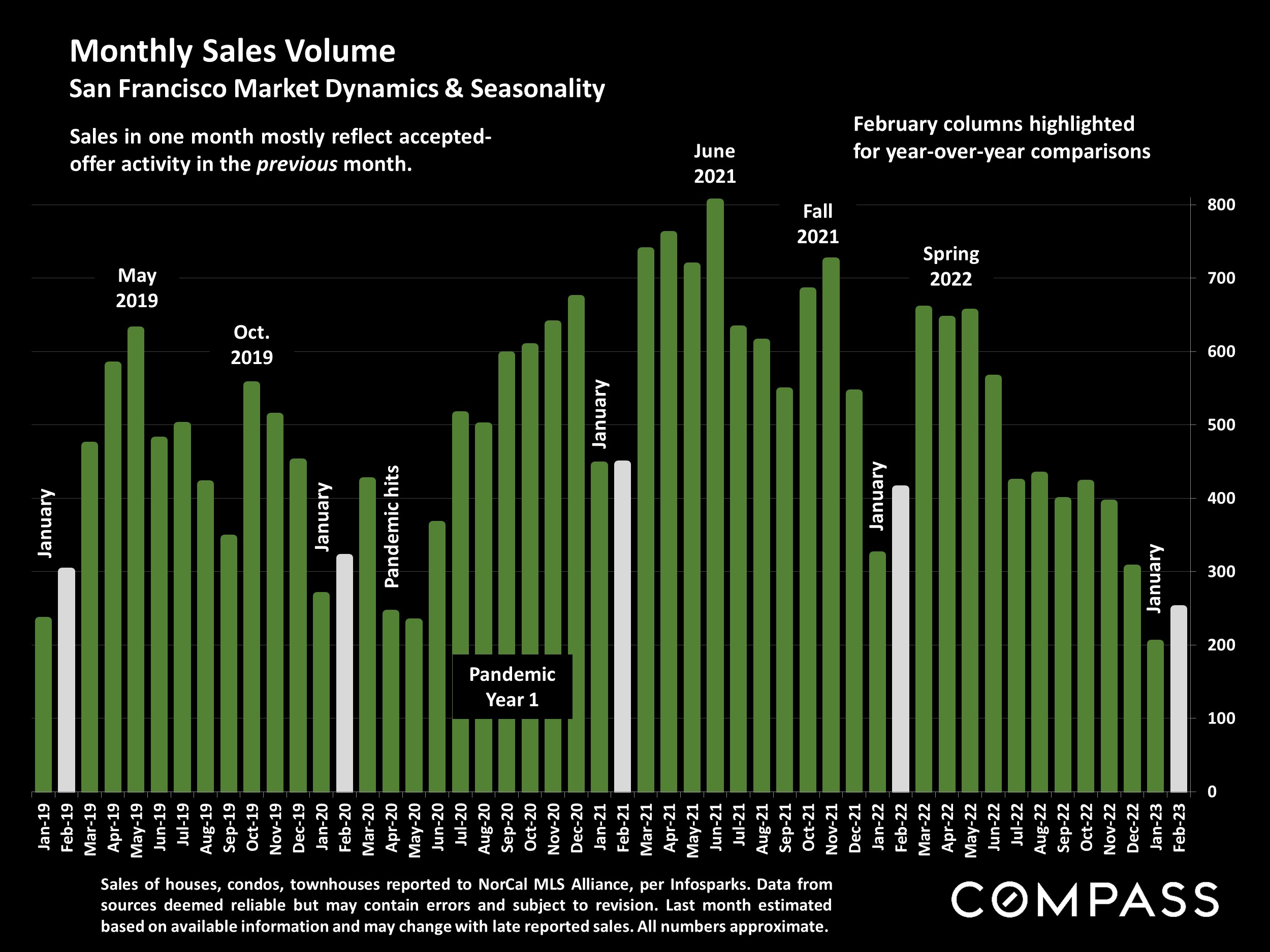

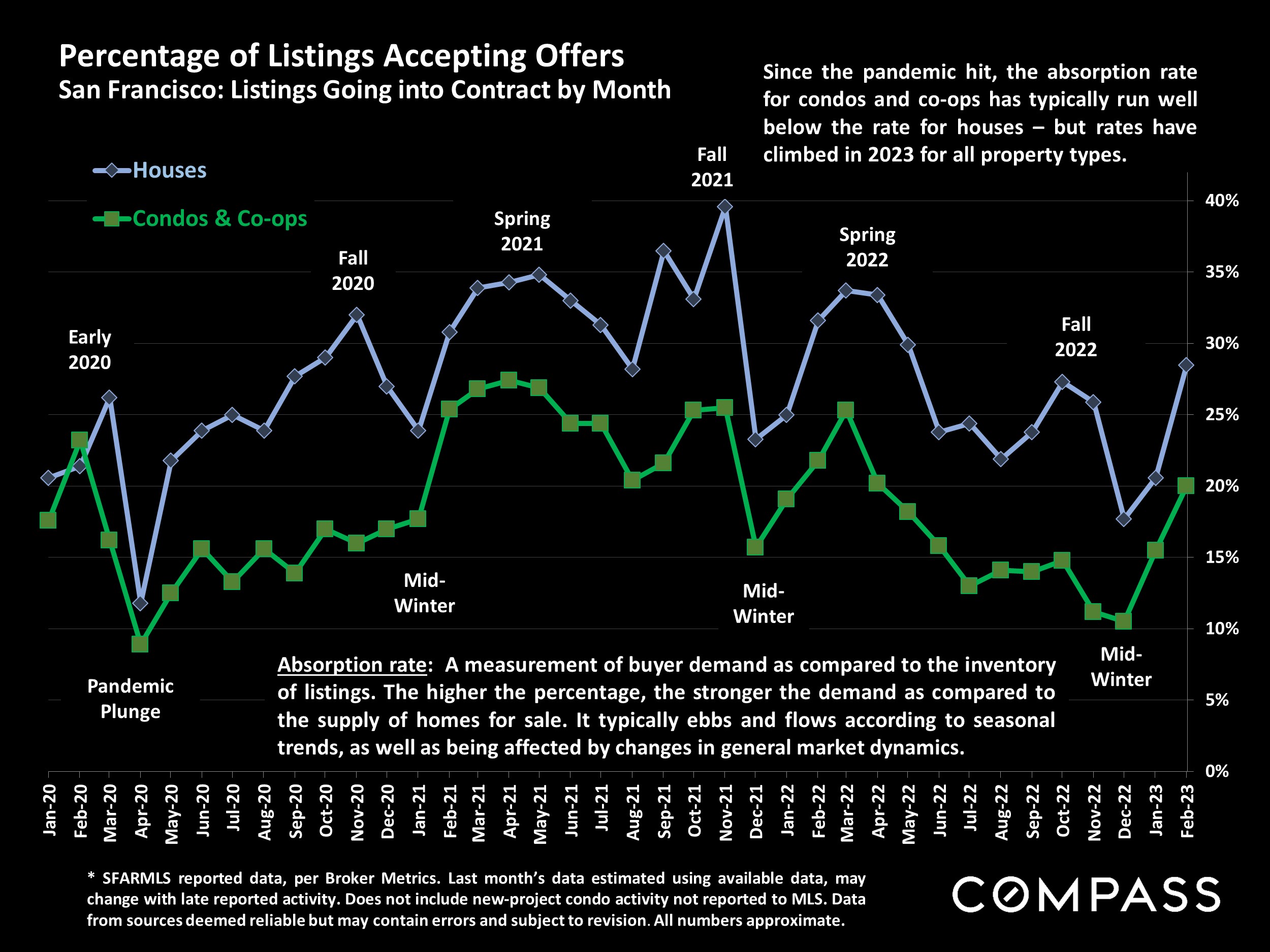

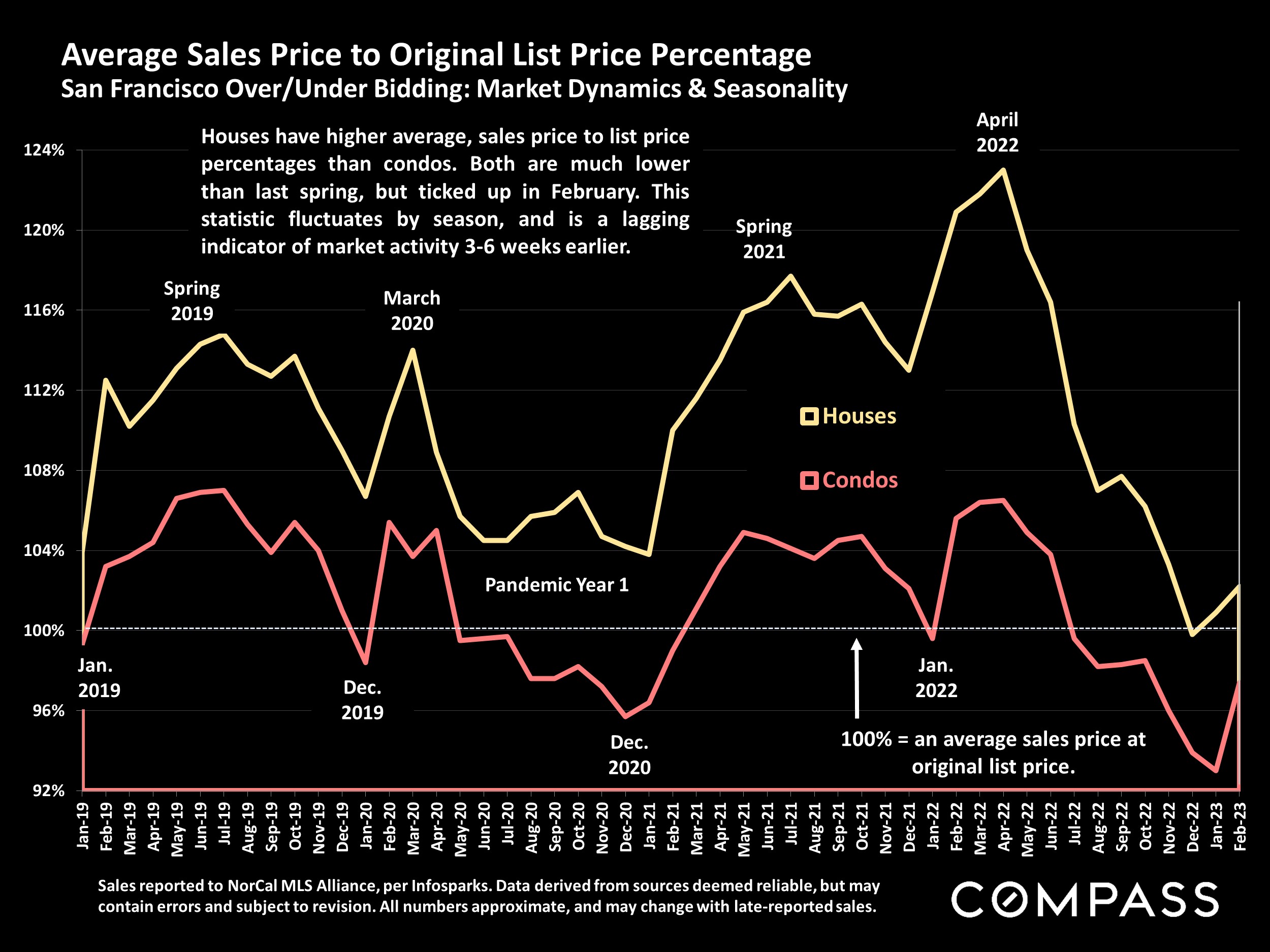

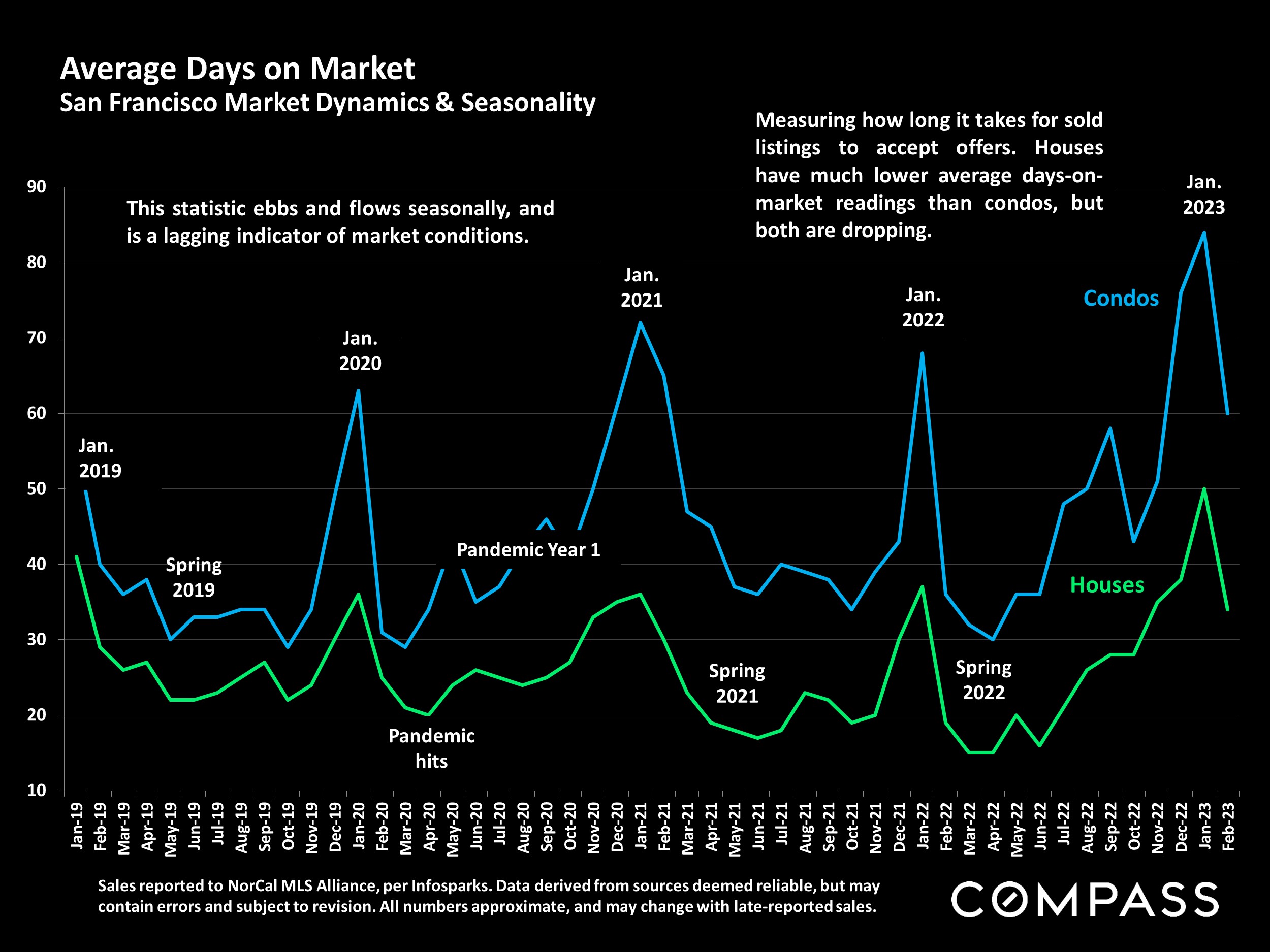

After the acute decline in market activity in the 2nd half of 2022, buyer demand rose dramatically and most market indicators turned positive in 2023: Open house traffic, number of offers, and overbidding & absorption rates all saw improvement.

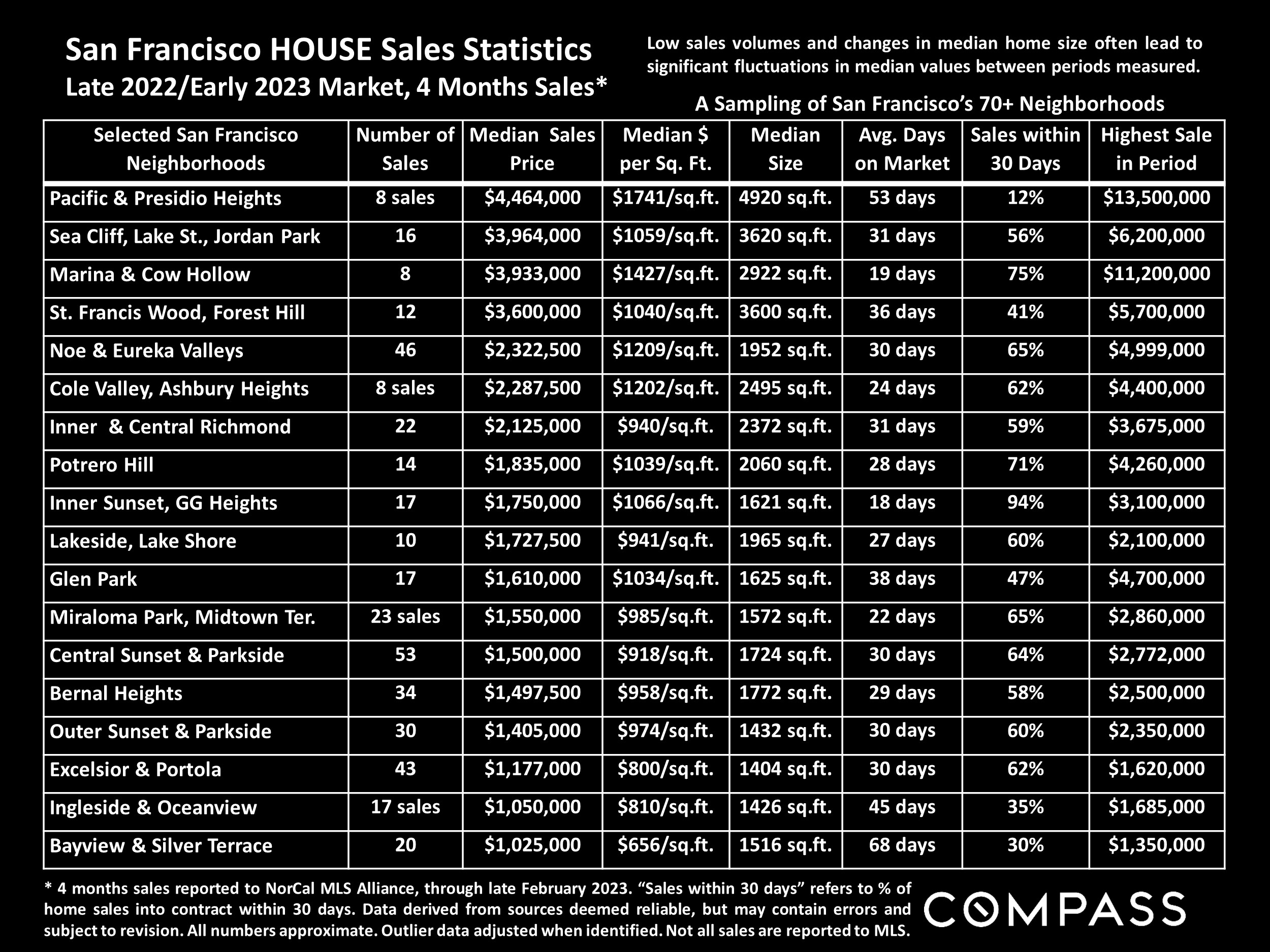

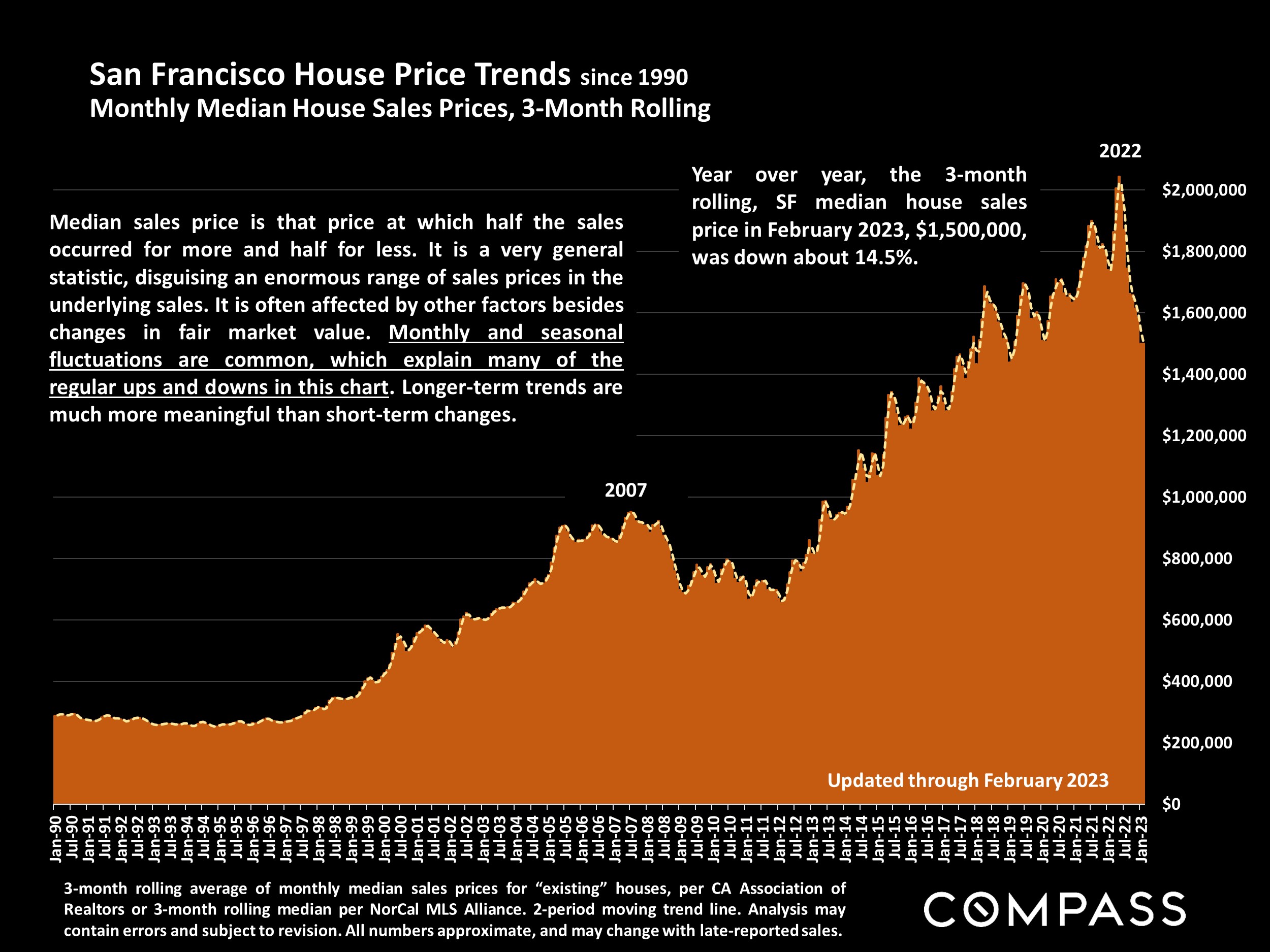

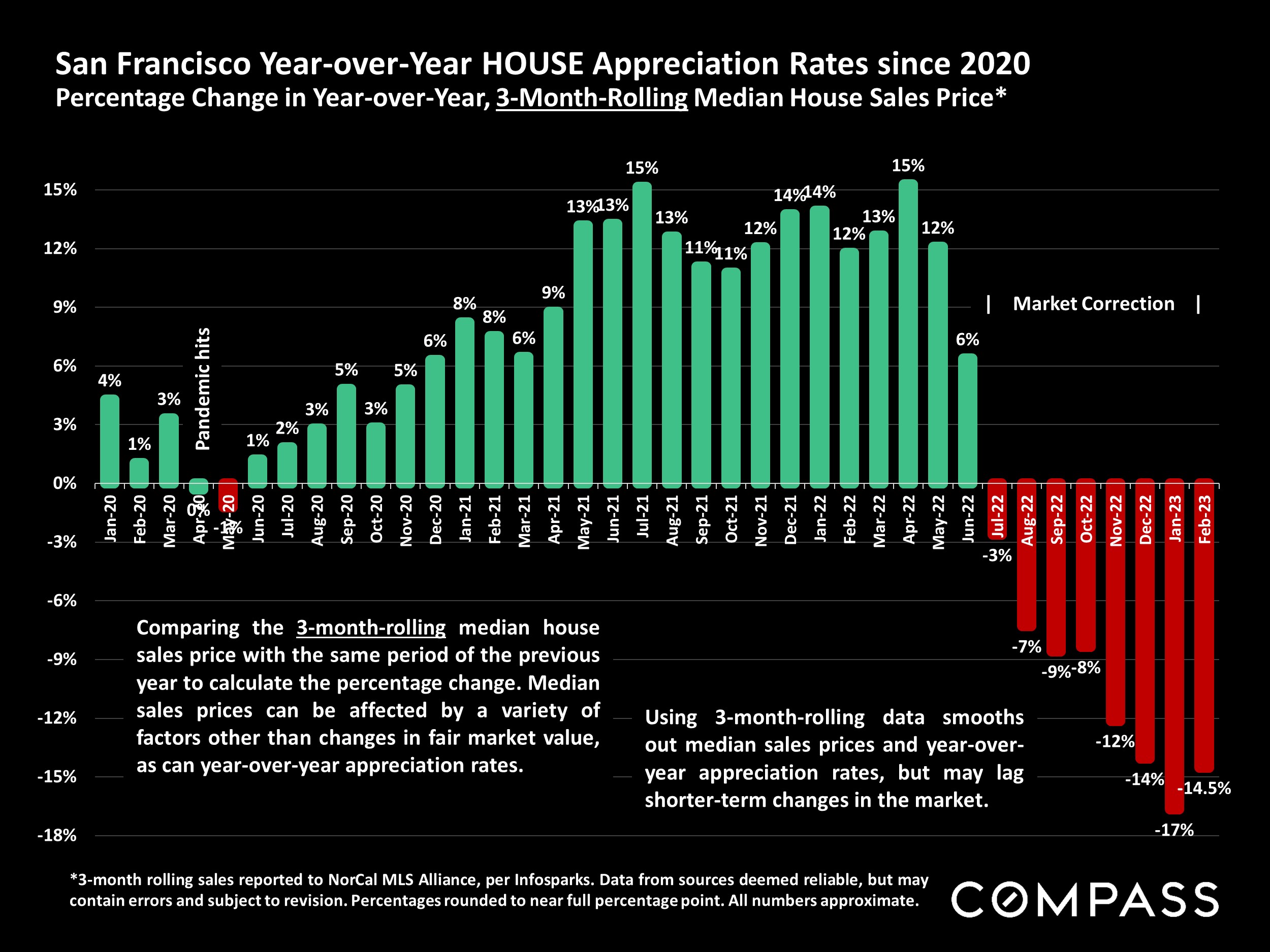

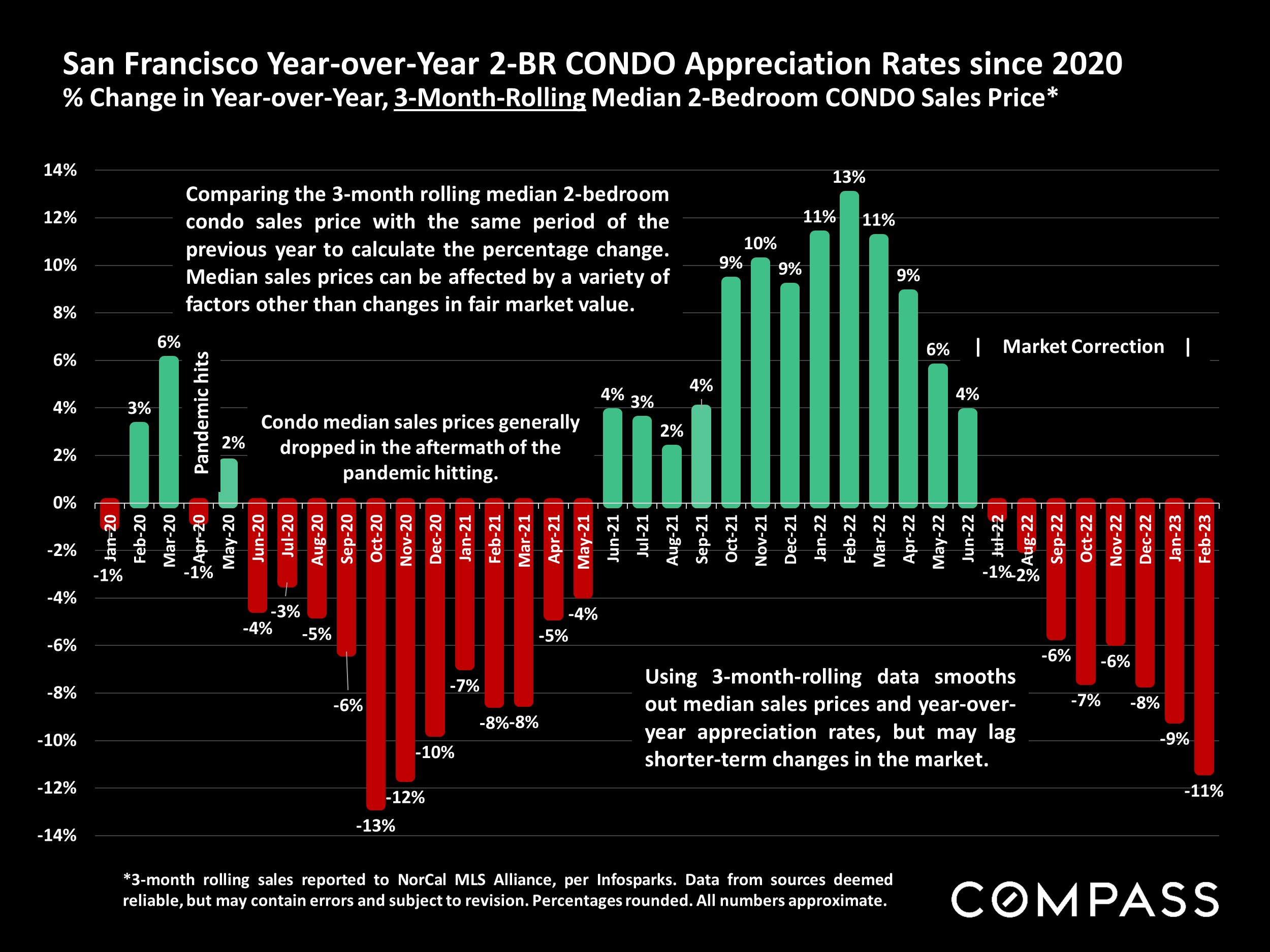

It is too early for significant effects to show up in home prices: Through February, 3-month-rolling median house sale prices saw year-over-year declines across all Bay Area counties (these percentage declines should be regarded cautiously until substantiated over the longer term):

San Francisco Median Sale Price

February 2023: $1,500,000 (down 14.5% Y.O.Y.)

February 2022: $1,755,000

February 2021: $1,570,000

February 2020: $1,460,000

February 2019: $1,445,000

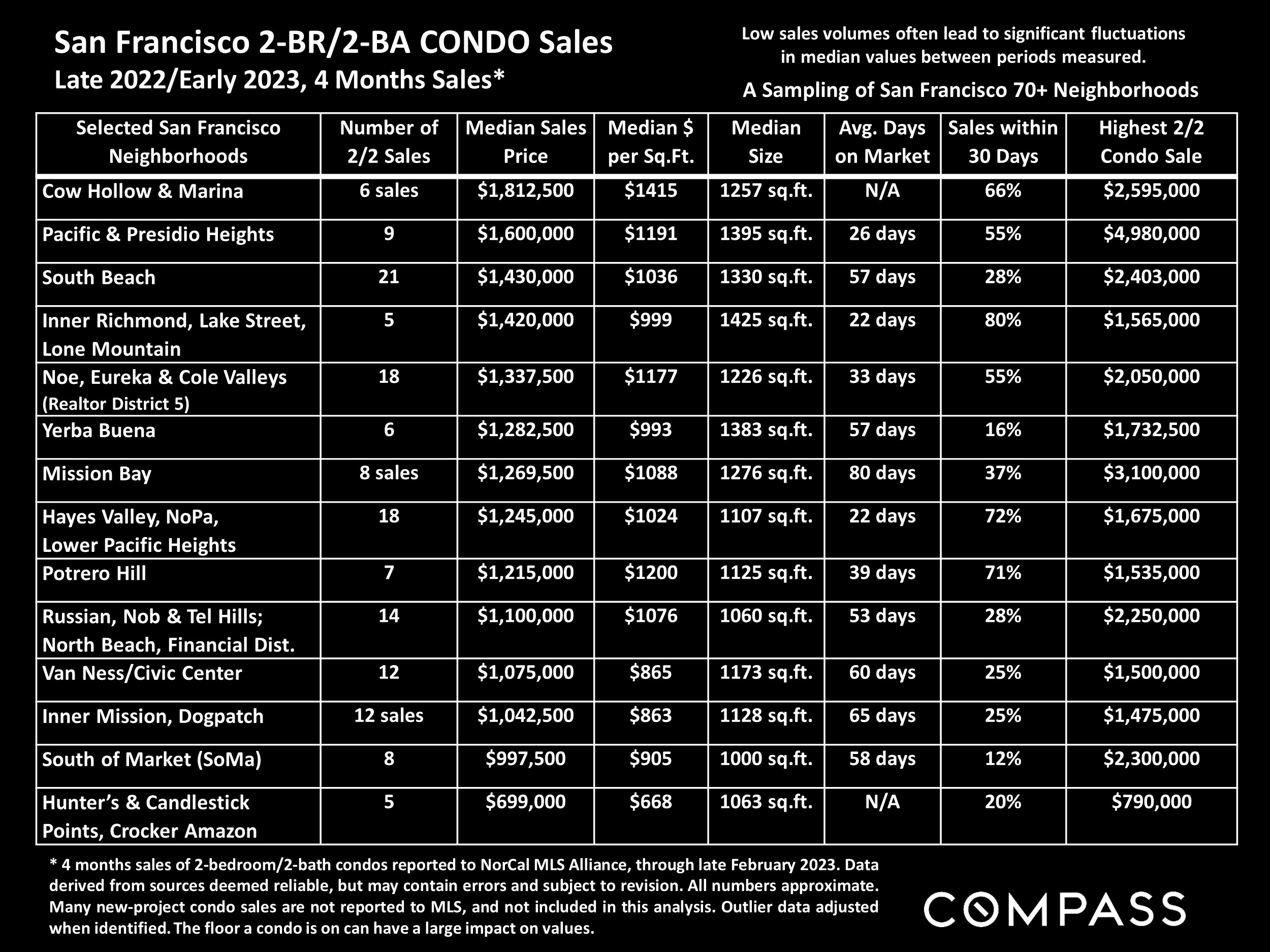

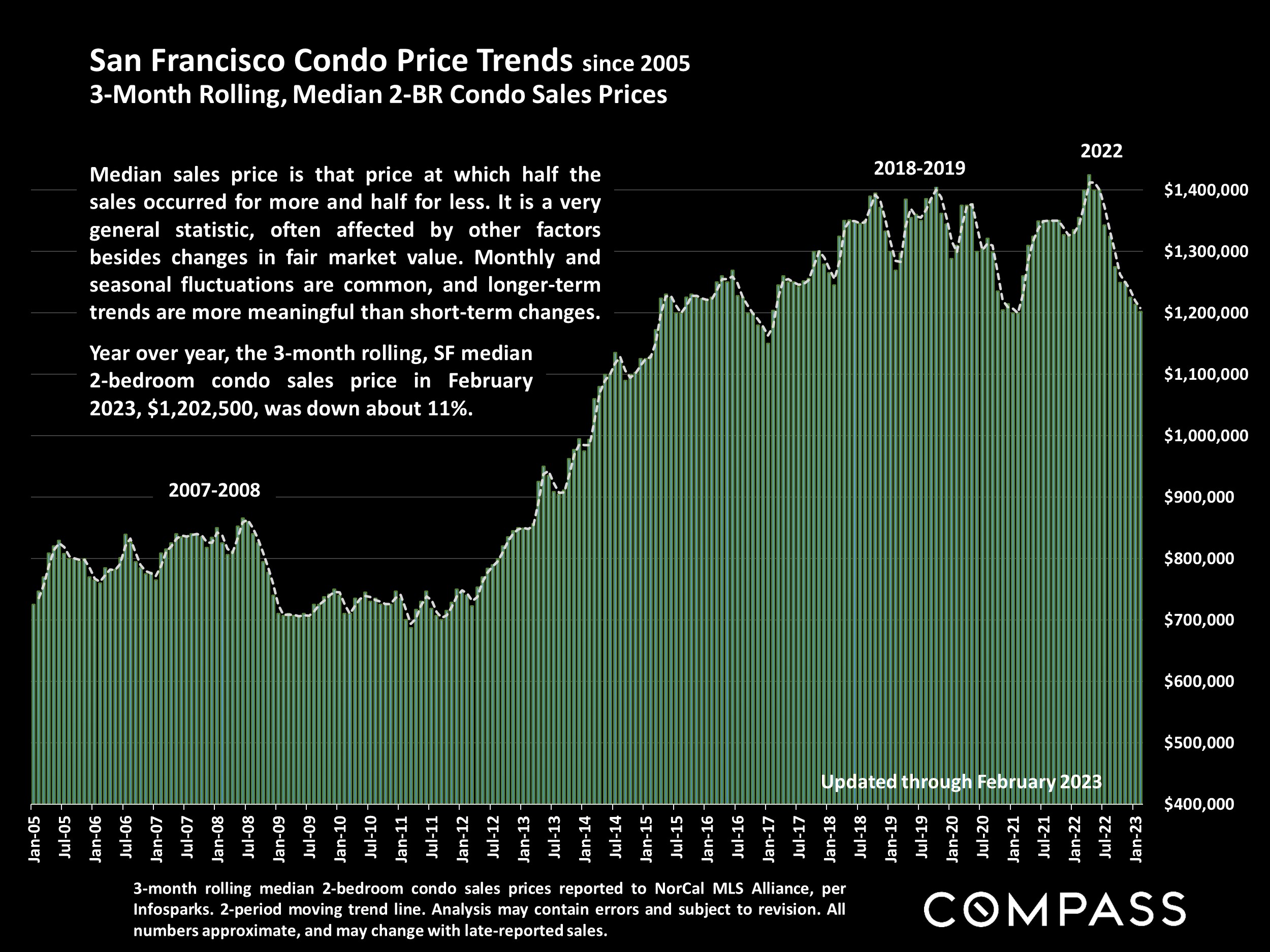

February 2023: $1,041,000 (down 16.7% Y.O.Y.)

February 2022: $1,249,500

February 2021: $1,125,000

February 2020: $1,175,000

February 2019: $1,100,000

Even with the striking improvement in demand over late 2022, most year-over-year indicators remain depressed, but these comparisons are with the severely overheated conditions prevailing at the peak of a 10-year housing market upcycle. March through May is typically the most active listing and sales period of the year, and should soon provide much more data on supply, demand, and price trends. Over the last 3 years, spring markets were deeply affected, in very different and often surprising ways, by the onset of the pandemic (2020), the pandemic boom (2021) and soaring interest rates (2022).

To me, as has been the case for the last 14 months, the biggest wildcard remains interest rates: After dropping considerably in January from a November peak, they climbed again in February and early March, with big impacts on loan application rates. As rates climb, more opportunities exist, and cash holds more value.

If you have any questions about the market, specific property, my top investment choices in the market today, etc, I'm always here to help.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

338 Spear Street, Unit 39E

|

|

3 BD 2 BA 1582 SF $2,625,000

|

|

|

|

|

|

|

|

|

|

15 Lucerne Street, Unit B

|

|

2 BD 3 BA 1875 SF $1,295,000

|

|

|

|

|

|

|

|

|

|

|

1 Burnett Avenue North, Unit 9

|

|

3 BD 3 BA 2157 SF $1,895,000

|

|

|

|

|

|

|

|

|

|

333 Beale Street, Unit 7F

|

|

1 BD 1 BA 920 SF $895,000

|

|

|

|

|

|

|

|

|

|

|

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics - such as "active listings," "days on market," and "months supply of inventory" - differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won't be reflected in the data. "Homes" signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, or their MLS areas, unless otherwise delineated. Multicounty metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, "bonus" rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis.

|

|

Compass is a real estate broker licensed by the State of California operating under multiple entities. License Numbers 01991628, 1527235, 1527365, 1356742, 1443761, 1997075, 1935359, 1961027, 1842987, 1869607, 1866771, 1527205, 1079009, 1272467. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions.

|

|

|

|

|

|

|