Clients, friends, and colleagues:

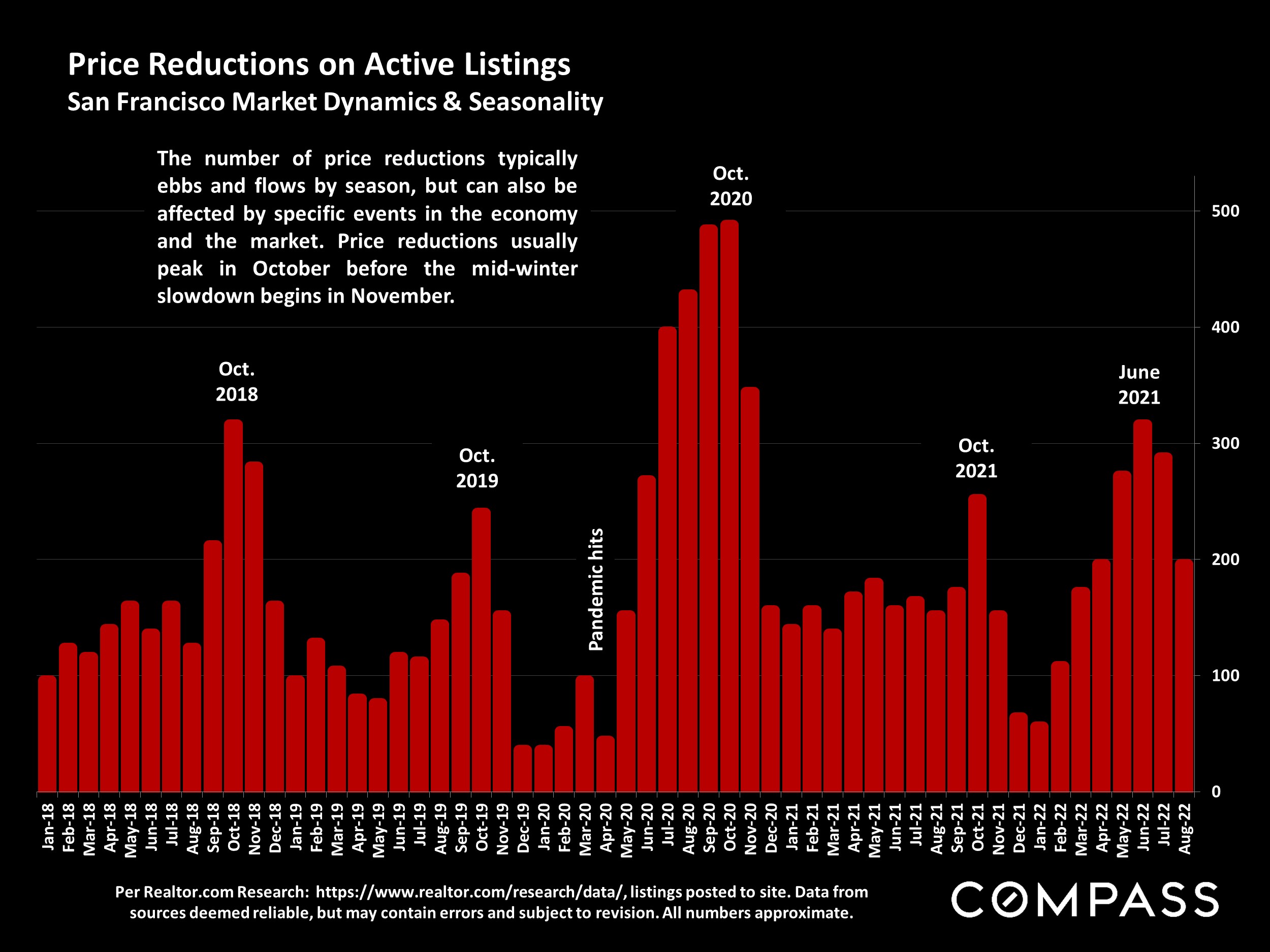

In August, many of us agents were reporting that buyer activity - renewed interest in getting back into the market, visits to open houses, and so on - was picking up due to a number of issues: Price reductions, less competition, the settling of interest rates, and the dramatic recovery in stock markets.

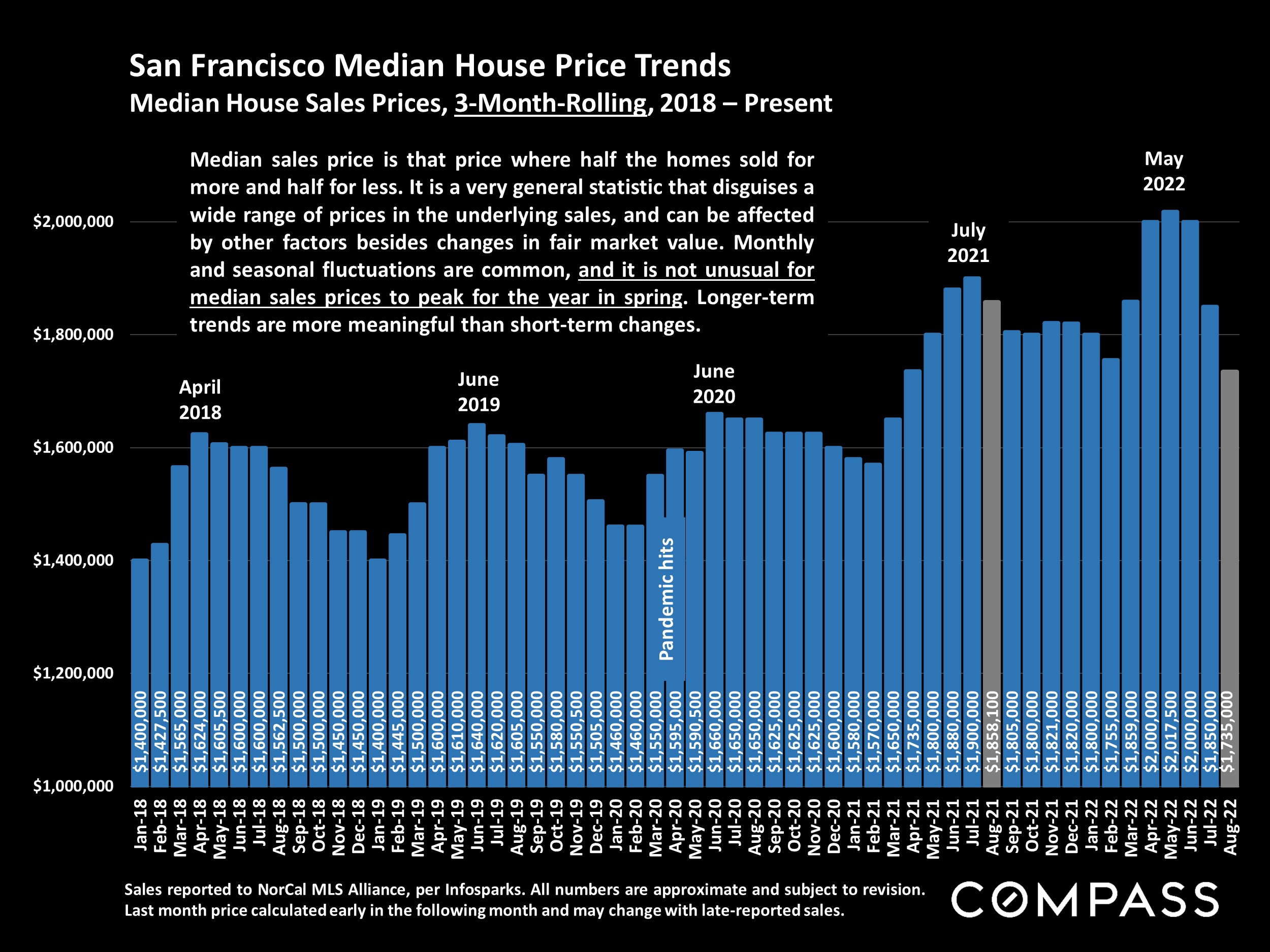

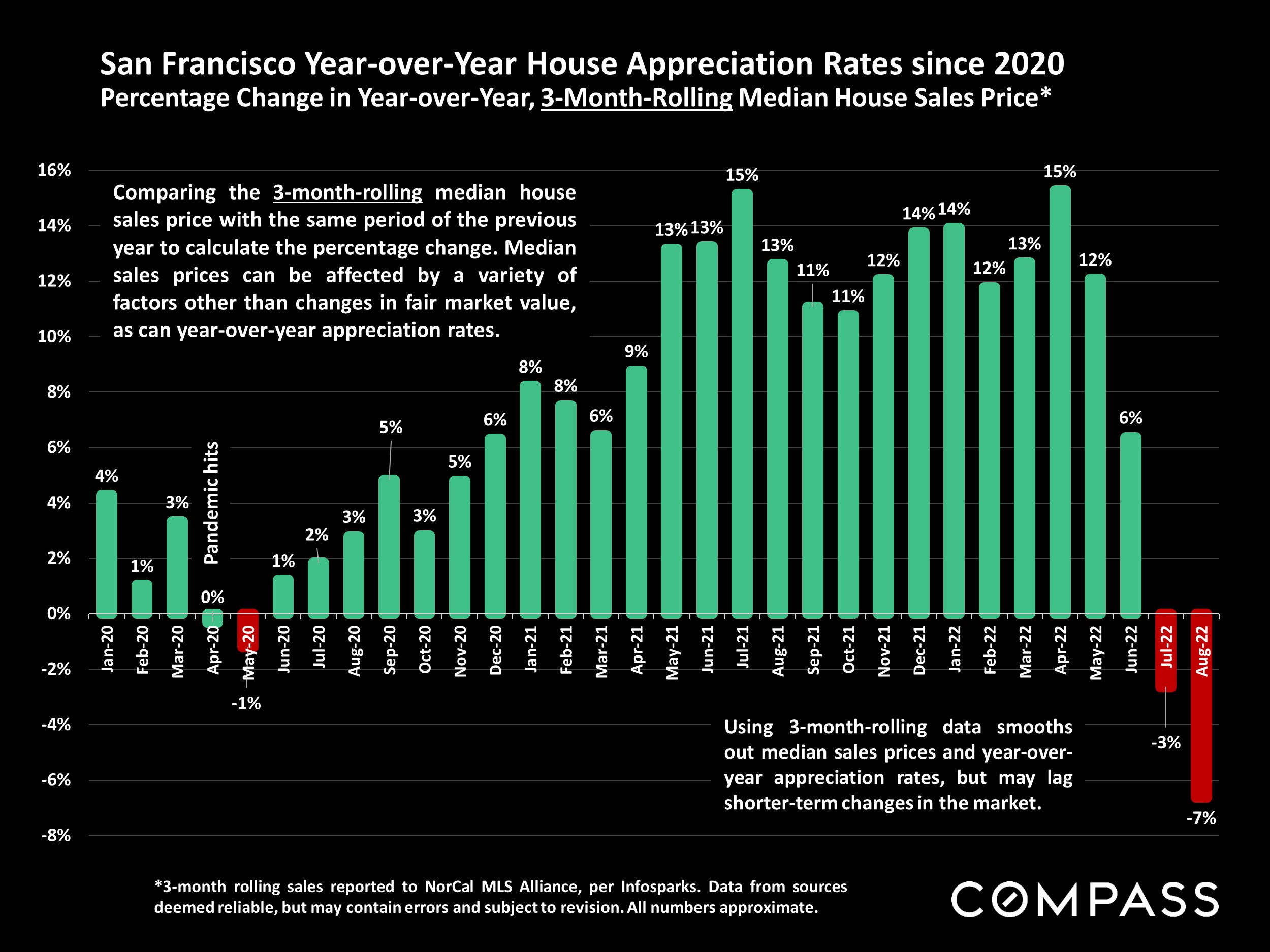

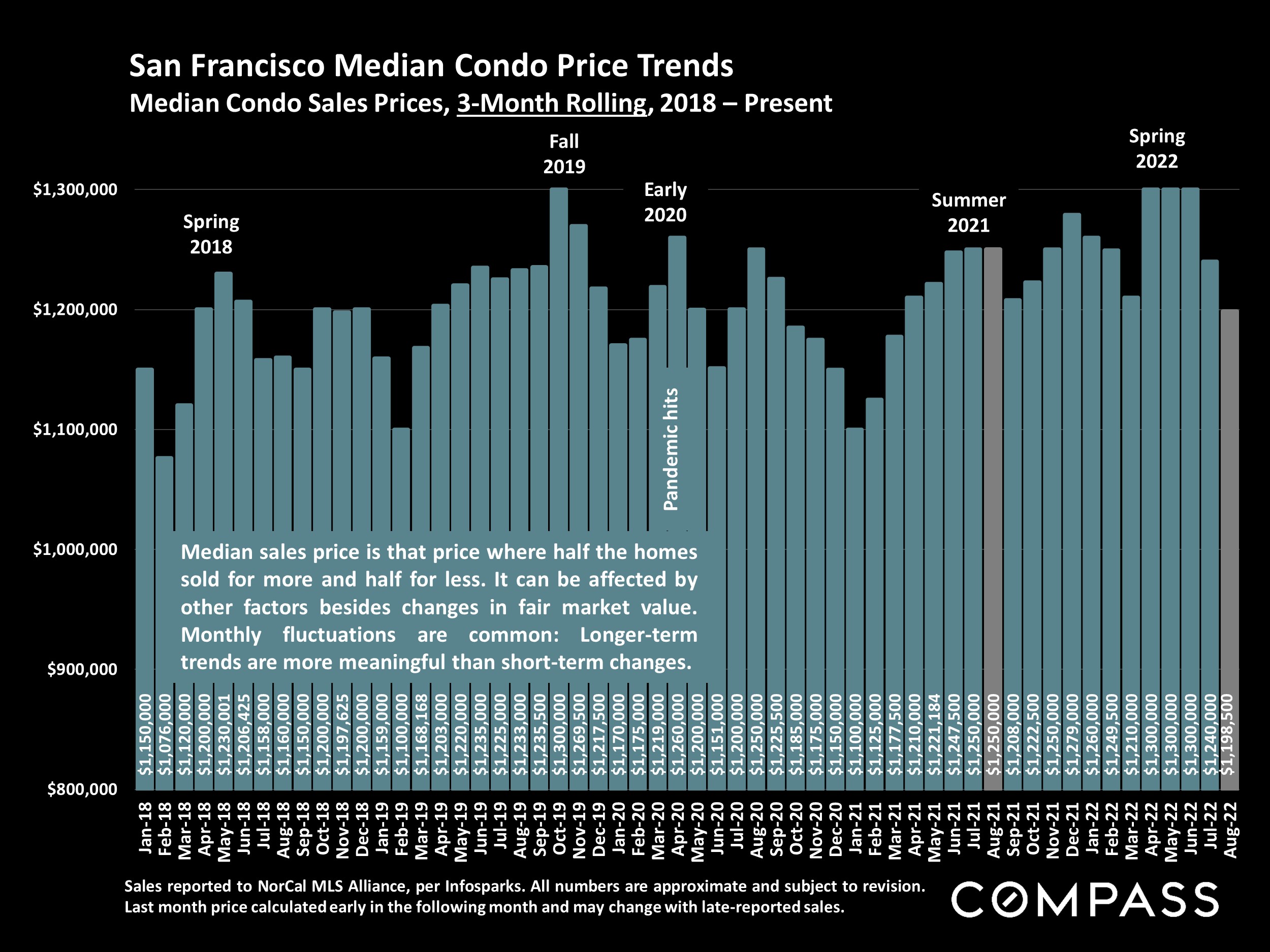

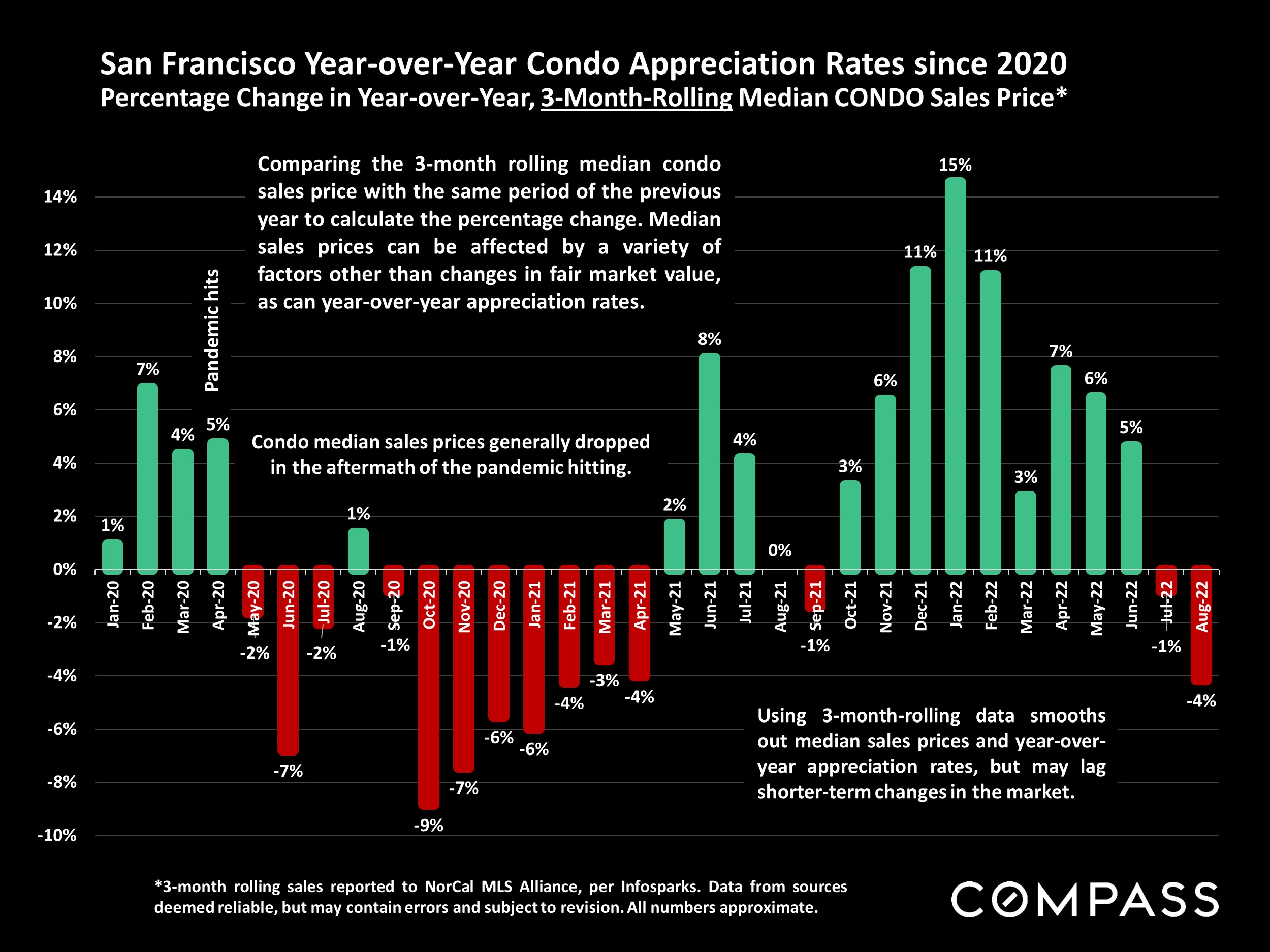

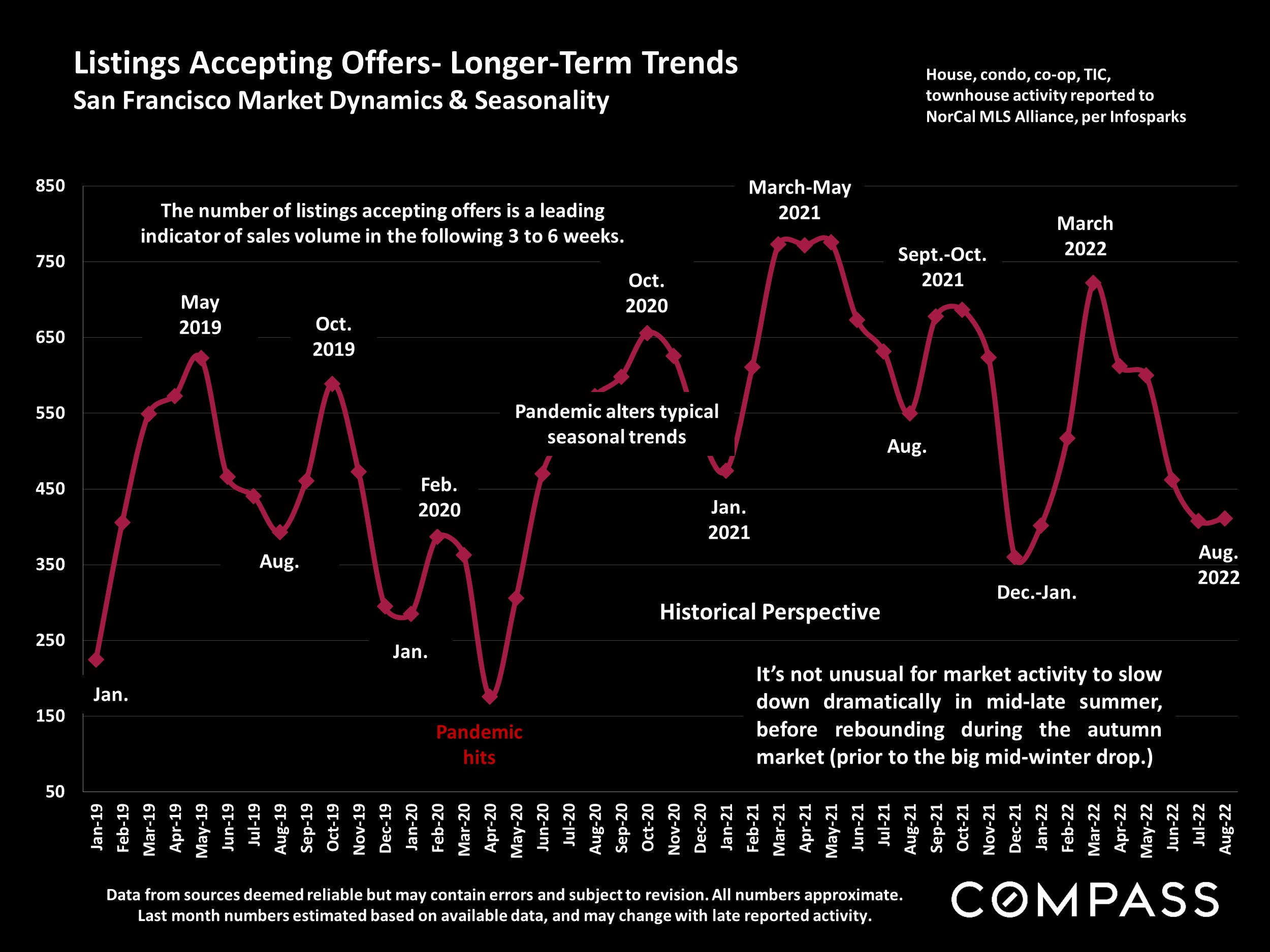

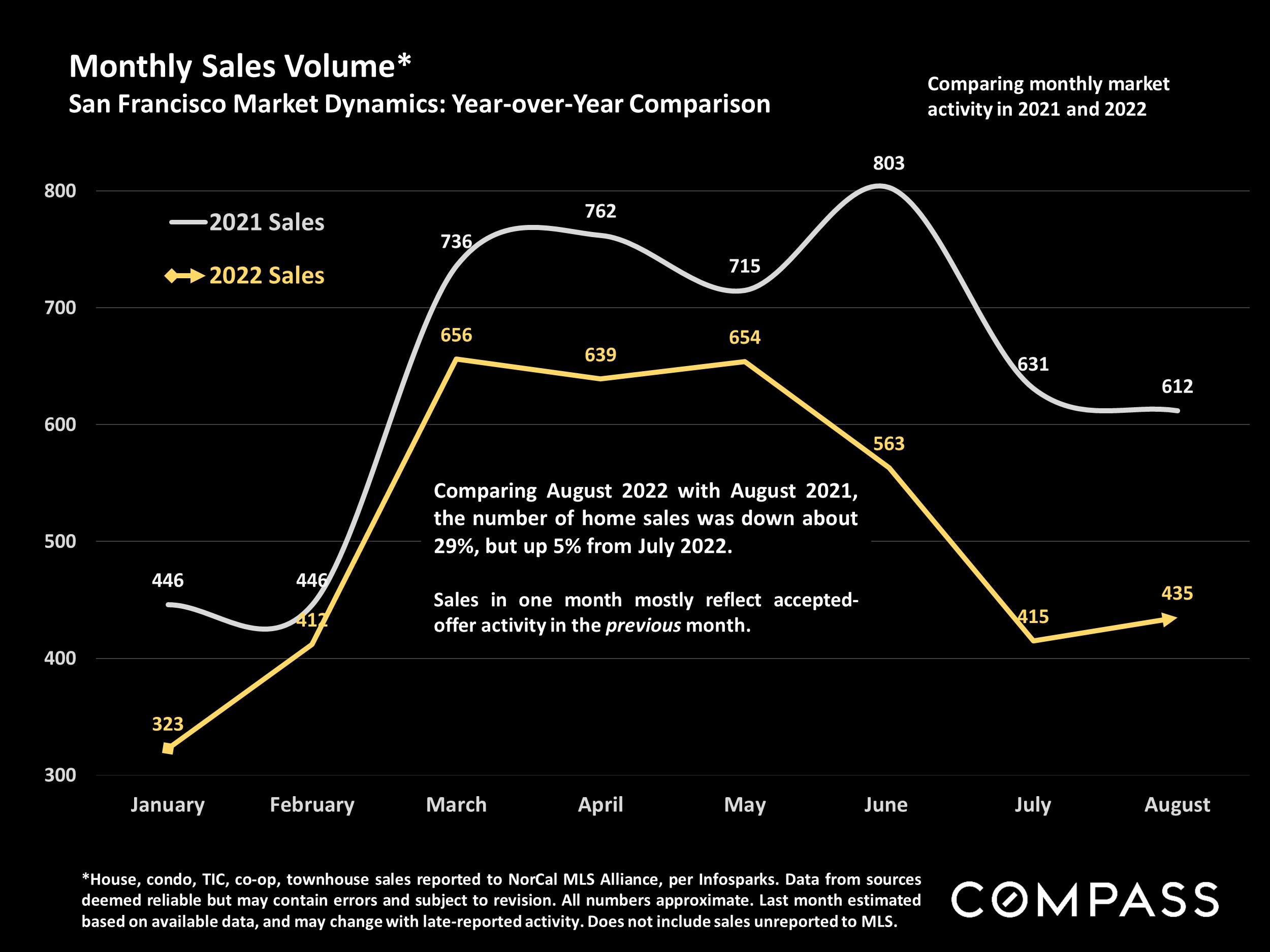

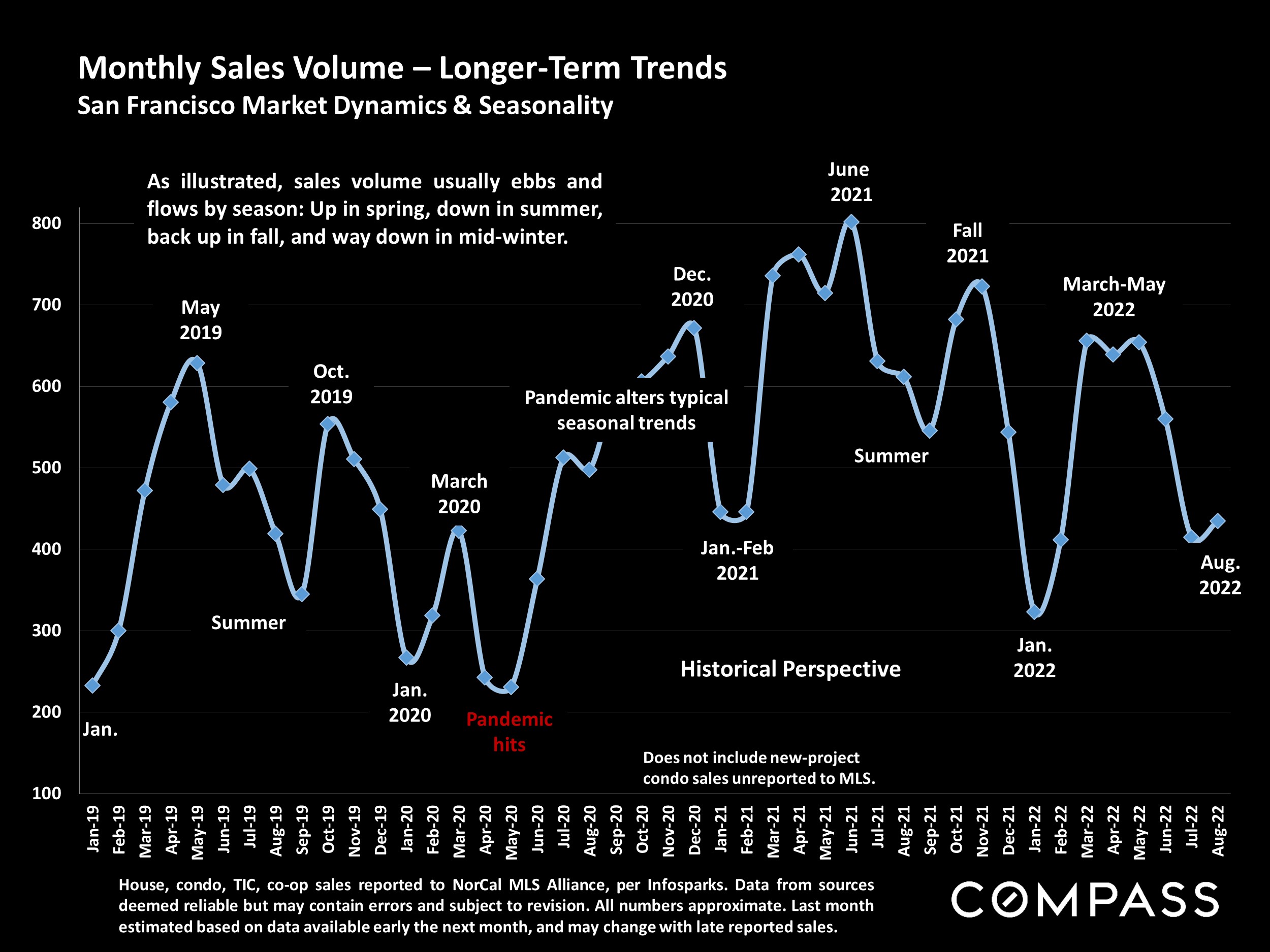

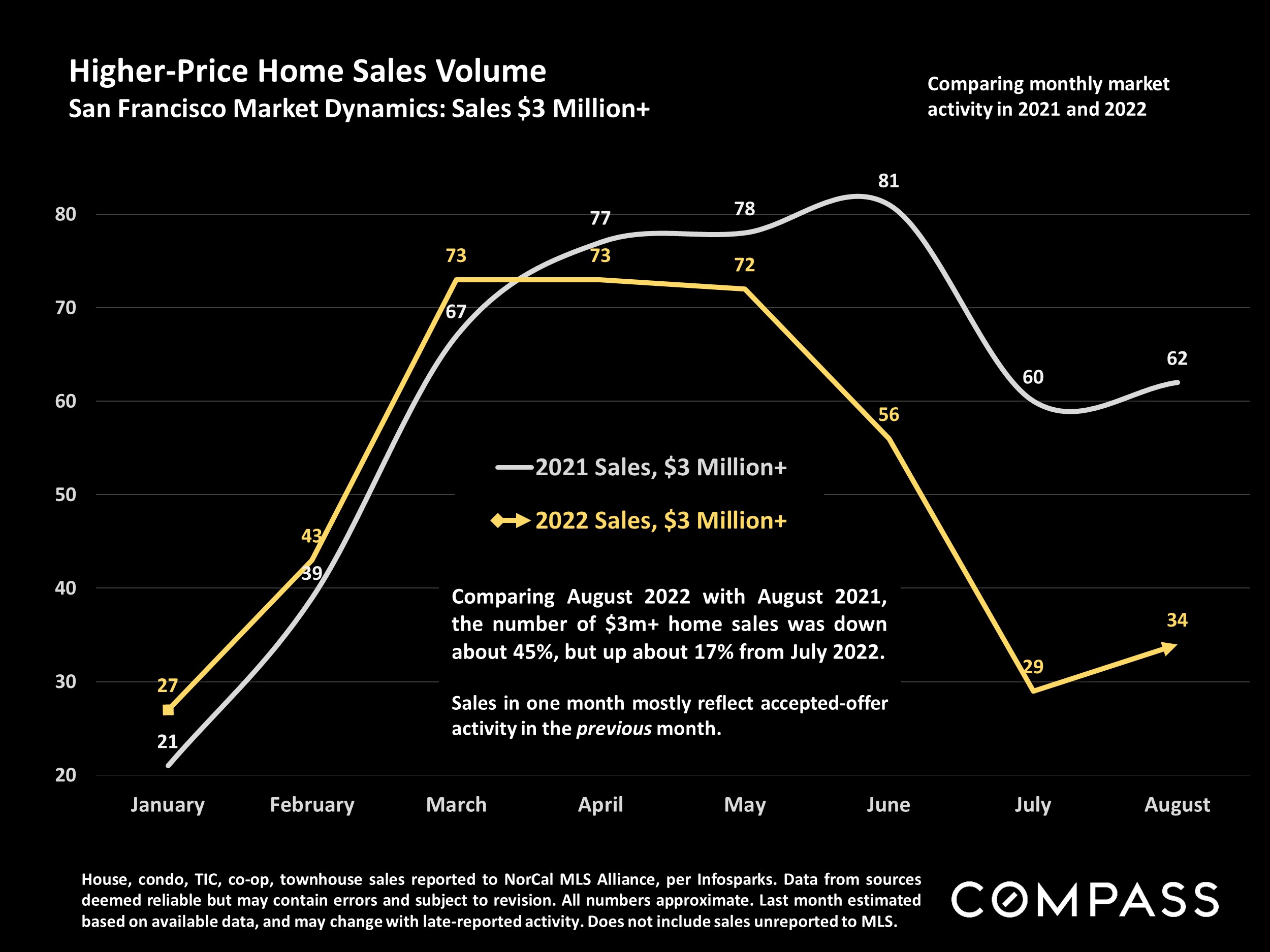

And a small rebound in SF sales did show up in the August data: sales usually tick down in August from July, though volume was still well below last year.

Across the Bay Area,

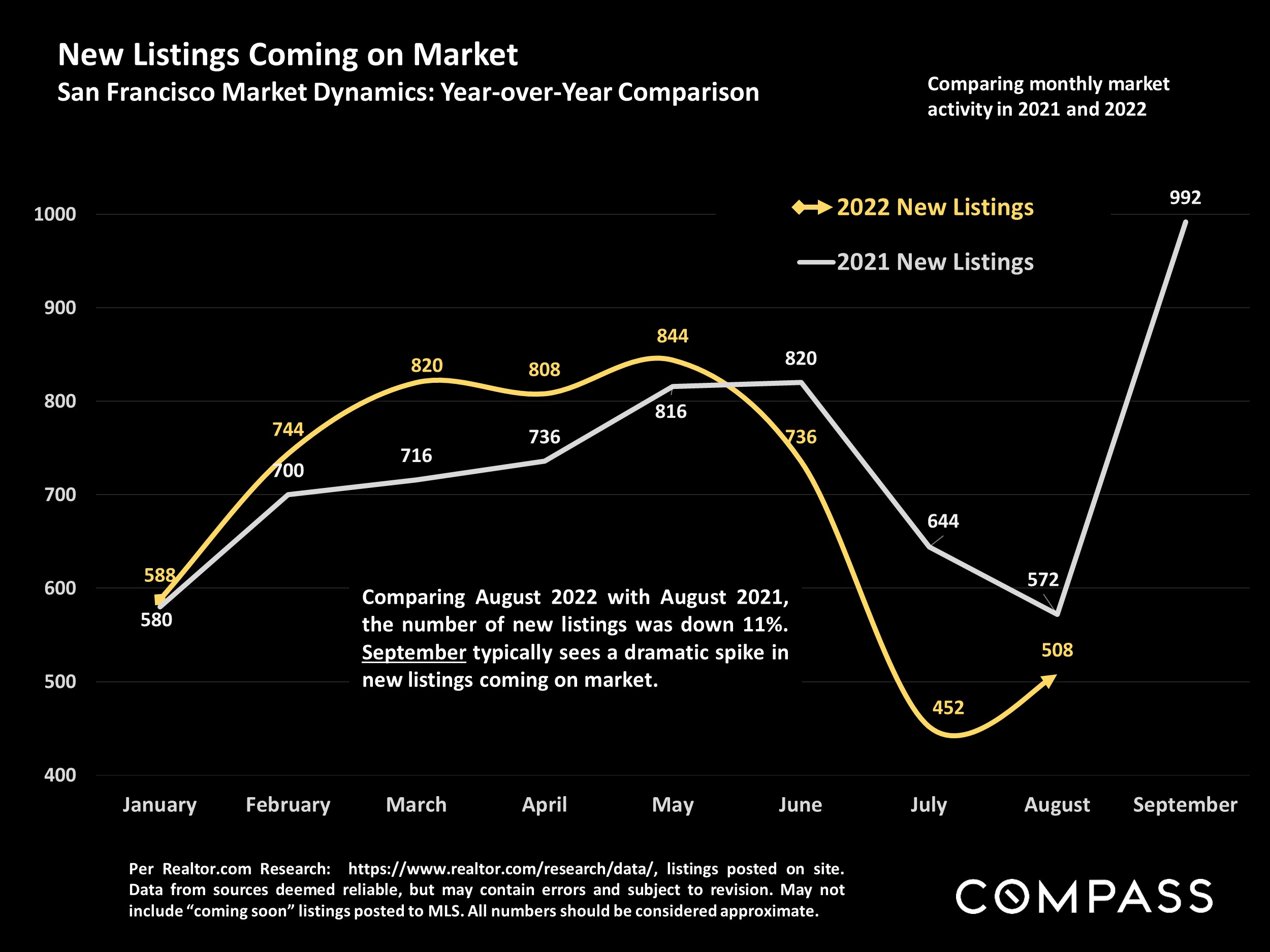

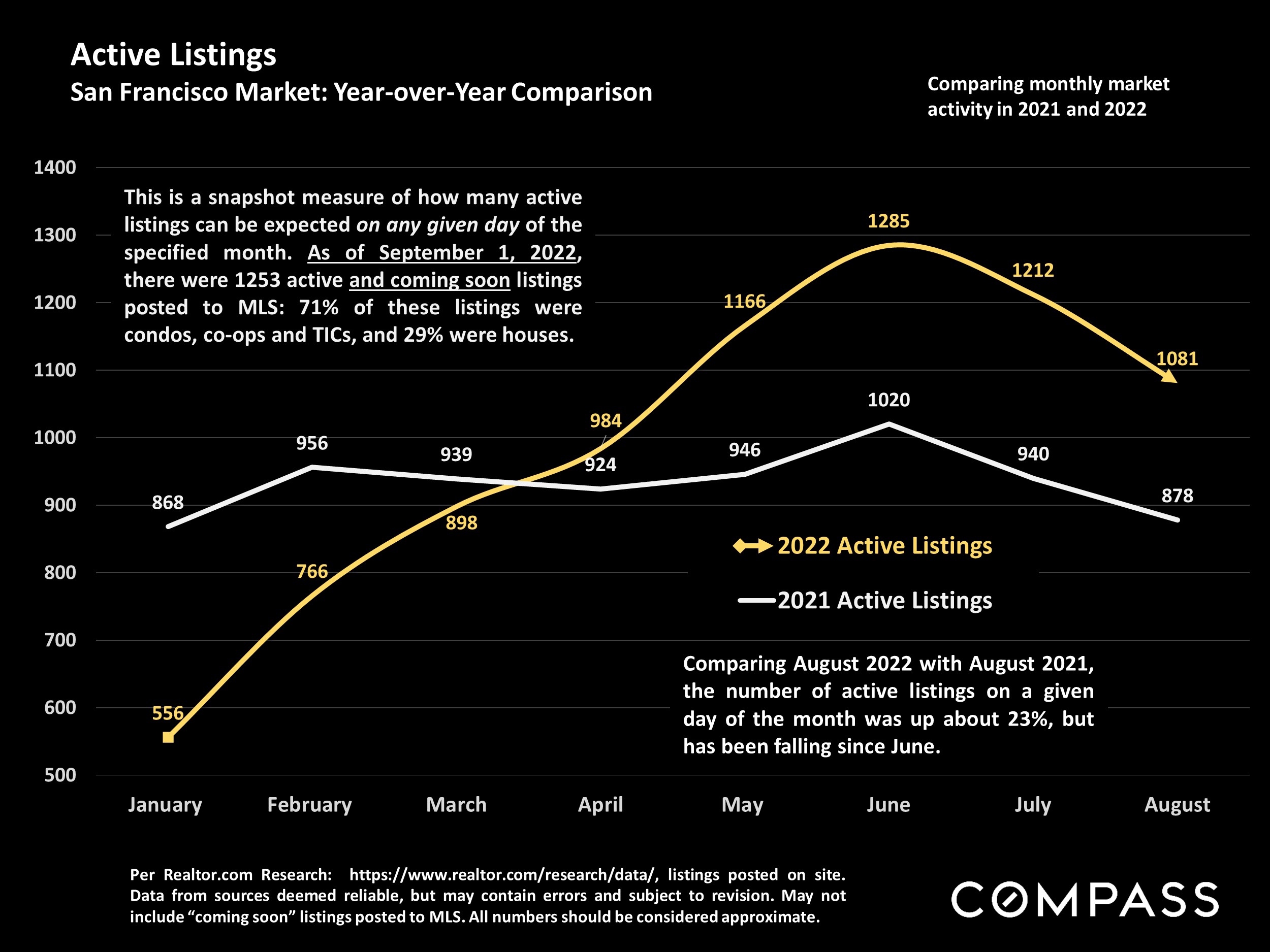

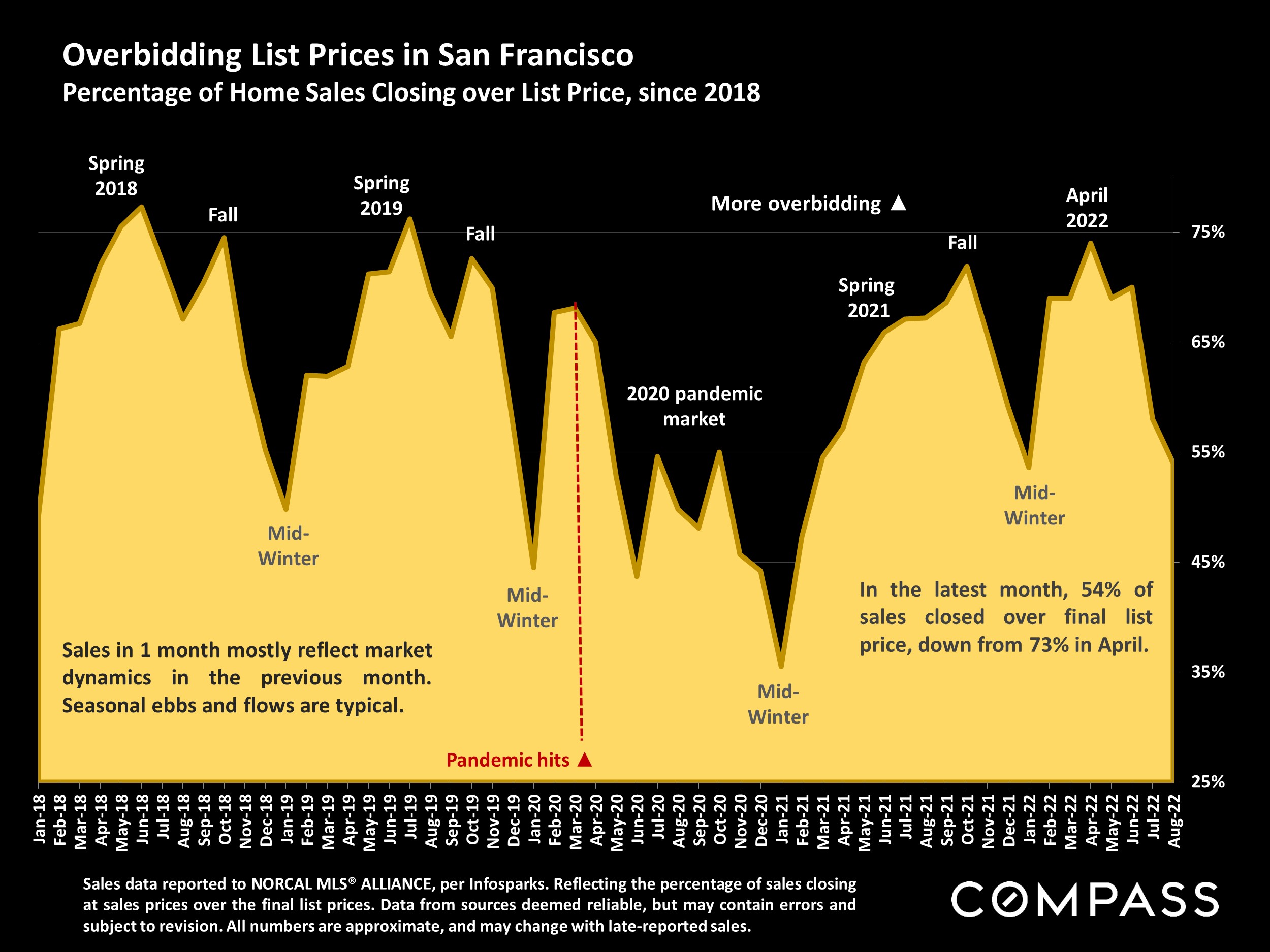

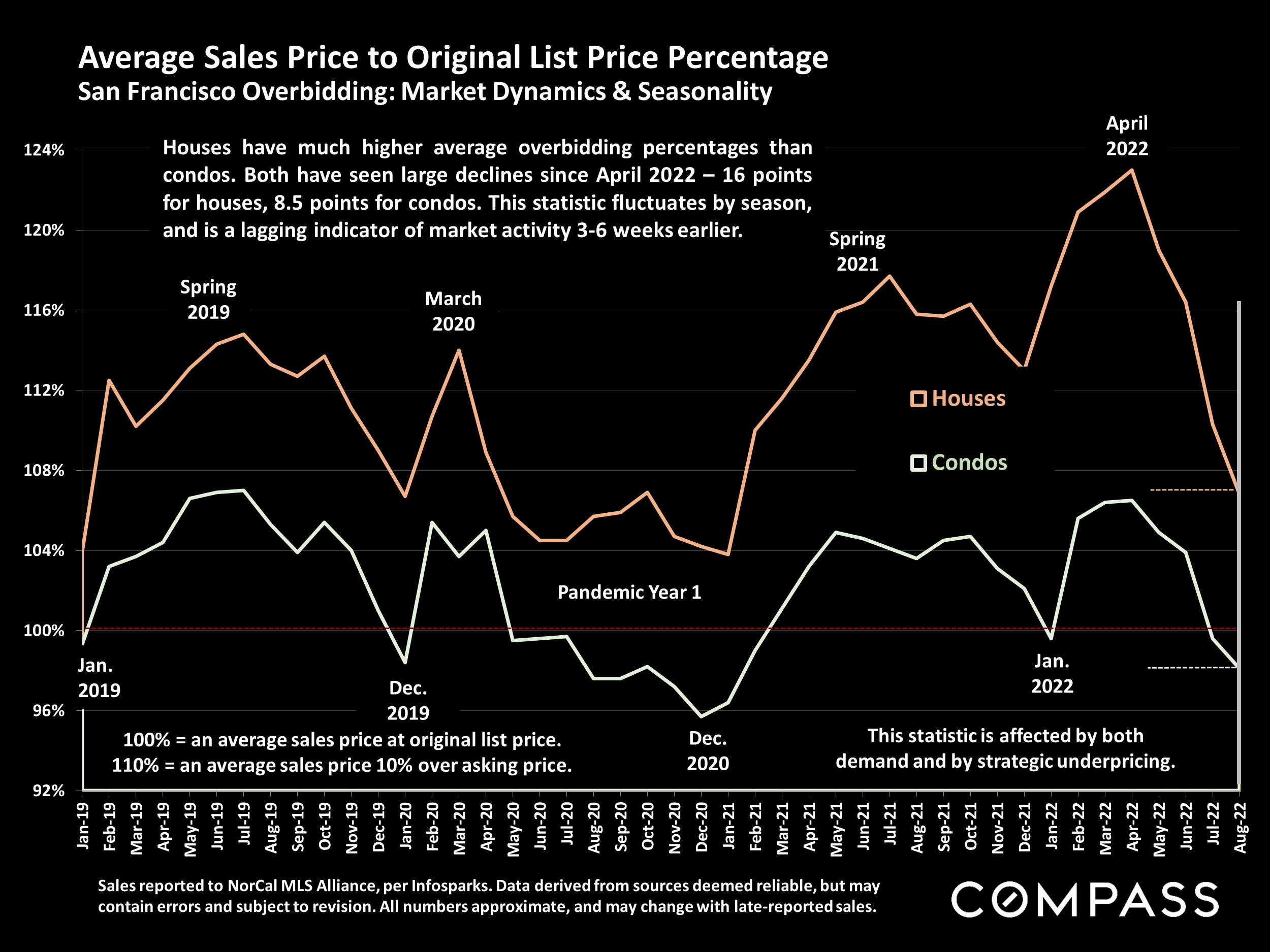

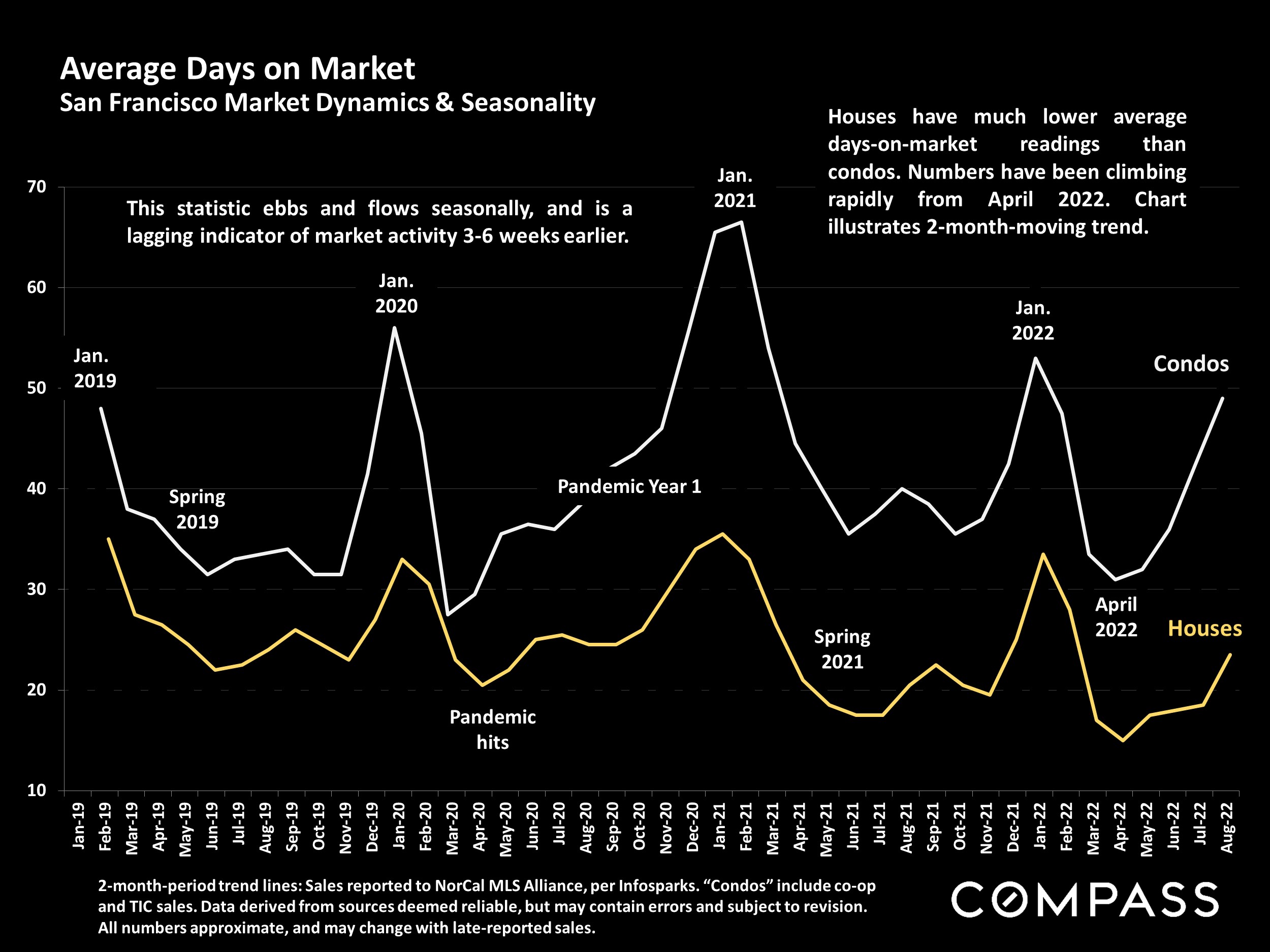

year-over-year, home-price appreciation rates and overbidding statistics have continued to drop, and days-on-market to climb. In August, the number of new listings coming on market was lower year-over-year, and the number of active listings for sale declined, though still significantly higher than previous years.

While September numbers won't be released until next week, we saw a typical jump in new listing activity right after Labor Day. Some single-family homes, and even condos, have seen recent success with under-pricing and setting offer dates, but the vast majority of inventory is using transparent pricing and taking offers-as-they-come. As we know, September is typically the single month with the highest number of new listings, which then fuels autumn sales.

As of now, interest rates have increased again and stock markets have declined once more: they continue to see substantial short-term volatility and it remains difficult to confidently predict their future movements and effects on real estate markets. The next major indicator of buyer & seller psychology and market dynamics will be what occurs during the next 2 months of the autumn selling season, prior to the mid-November to mid-January holiday slowdown (typically the slowest market of the year).

For any specific questions, feel free to reach out to me directly. It's especially important to get professional guidance during volatile times.

Recent sales, contracts, and active listings @ the bottom